You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 2nd Quarter Report Poush 2077 1Document14 pages2nd Quarter Report Poush 2077 1Bushon SyshonNo ratings yet

- AEL Model 30 08 2018-v1Document13 pagesAEL Model 30 08 2018-v1haffaNo ratings yet

- AVB - EXAM QUESTIONS - 2021-2022 (Calculations)Document6 pagesAVB - EXAM QUESTIONS - 2021-2022 (Calculations)Dean ErlanggaNo ratings yet

- 4th Quarter Unaudited Report 2076-2077Document25 pages4th Quarter Unaudited Report 2076-2077Srijana DhunganaNo ratings yet

- Provisional Financials F Y 2020-21Document16 pagesProvisional Financials F Y 2020-21CA Prakash YathamNo ratings yet

- CIPLADocument10 pagesCIPLAMAGOMU DAN DAVIDNo ratings yet

- Adani Ports & Special Economic Zone Ltd. (India) : SourceDocument9 pagesAdani Ports & Special Economic Zone Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Purcari Lucru IndividualDocument7 pagesPurcari Lucru IndividualLenuța PapucNo ratings yet

- Accounting Assignment QuestionDocument14 pagesAccounting Assignment QuestionsureshdassNo ratings yet

- Bajaj Finserv Ltd. (India) : SourceDocument5 pagesBajaj Finserv Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Standardized Financial Statements - SolutionDocument25 pagesStandardized Financial Statements - SolutionanisaNo ratings yet

- Financials 1219051-21.09.20Document6 pagesFinancials 1219051-21.09.20Eduardo FélixNo ratings yet

- Hartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesDocument6 pagesHartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesJUWAIRIA BINTI SADIKNo ratings yet

- Account Cca (AutoRecovered) 1Document13 pagesAccount Cca (AutoRecovered) 1Saloni BaisNo ratings yet

- Financial Statement 2020Document3 pagesFinancial Statement 2020Fuaad DodooNo ratings yet

- United Bank For Africa (Ghana) Limited Summary Financial Statements For The Year Ended 31 December 2020Document2 pagesUnited Bank For Africa (Ghana) Limited Summary Financial Statements For The Year Ended 31 December 2020Fuaad DodooNo ratings yet

- Beneish M ScoreDocument45 pagesBeneish M ScoreAnshu RaiNo ratings yet

- SCALP Handout 040Document2 pagesSCALP Handout 040Cher NaNo ratings yet

- SCALP Handout 040Document2 pagesSCALP Handout 040Eren CuestaNo ratings yet

- Example For Financial Statement AnalysisDocument2 pagesExample For Financial Statement AnalysisMobile Legends0% (1)

- SCALP Handout 040Document2 pagesSCALP Handout 040Cher NaNo ratings yet

- Asian PaintsDocument6 pagesAsian PaintsDivyagarapatiNo ratings yet

- Asian Paints Ltd. (India) : SourceDocument6 pagesAsian Paints Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Global Auto PartsDocument33 pagesGlobal Auto Partssantosh pandeyNo ratings yet

- Cervecería Nacional - FinanzasDocument39 pagesCervecería Nacional - FinanzasLuismy VacacelaNo ratings yet

- Emis Soriana IndicesDocument11 pagesEmis Soriana IndicesRamiro Gallo Diaz GonzalezNo ratings yet

- United Bank Limited and Its Subsidiary CompaniesDocument15 pagesUnited Bank Limited and Its Subsidiary Companieszaighum sultanNo ratings yet

- Standalone Statement of Cash Flows For The Year Ended 31St March, 2020Document6 pagesStandalone Statement of Cash Flows For The Year Ended 31St March, 2020C17ShagunNo ratings yet

- Fatima Jinnah Women University Department of Computer Arts Home Assignment For Class DiscussionDocument6 pagesFatima Jinnah Women University Department of Computer Arts Home Assignment For Class DiscussionHajra ZANo ratings yet

- EV Annual Report 2021 22Document69 pagesEV Annual Report 2021 22deepakturi2002No ratings yet

- M/S Goladi Khola Multipurpose Agriculture Firm: Pokhara-33, KaskiDocument10 pagesM/S Goladi Khola Multipurpose Agriculture Firm: Pokhara-33, KaskiMadhav Prasad KadelNo ratings yet

- Bank AnalysisDocument6 pagesBank AnalysisSachit KCNo ratings yet

- FMDocument8 pagesFMesmailkarimi456No ratings yet

- Company Limited: "We Foster Rich Customer Service"Document7 pagesCompany Limited: "We Foster Rich Customer Service"delrose delgadoNo ratings yet

- CHAPTER 6-FA Questions - BAsicDocument3 pagesCHAPTER 6-FA Questions - BAsicHussna Al-Habsi حُسنى الحبسيNo ratings yet

- Abott LabDocument6 pagesAbott LabRizwan Sikandar 6149-FMS/BBA/F20No ratings yet

- Financial PlanDocument25 pagesFinancial PlanAyesha KanwalNo ratings yet

- Ecobank Ghana Limited: Un-Audited Financial Statements For The Three-Month Period Ended 31 March 2022Document8 pagesEcobank Ghana Limited: Un-Audited Financial Statements For The Three-Month Period Ended 31 March 2022Fuaad DodooNo ratings yet

- Annual Report Meezan Bank (The Premier Islamic Bank) : Ratio Analysis Introduction of The CompanyDocument8 pagesAnnual Report Meezan Bank (The Premier Islamic Bank) : Ratio Analysis Introduction of The CompanyMaida KhanNo ratings yet

- NP SCBNL Fourth Quarter Two Thousand Seventy Six Seventy Seven ResultsDocument23 pagesNP SCBNL Fourth Quarter Two Thousand Seventy Six Seventy Seven ResultsMaahi MaharjanNo ratings yet

- Harus Dikerjakan Sendiri Dan Tidak Boleh DiskusiDocument12 pagesHarus Dikerjakan Sendiri Dan Tidak Boleh DiskusiRutinahNo ratings yet

- 2019FY Anual ResultDocument48 pages2019FY Anual ResultJ. BangjakNo ratings yet

- Income Statement (For The Year Ended 31 December, Taka'000) : Historical PeriodsDocument78 pagesIncome Statement (For The Year Ended 31 December, Taka'000) : Historical PeriodsDot com computer And It servicesNo ratings yet

- Asf ExcleDocument6 pagesAsf ExcleAnam AbrarNo ratings yet

- Annual Financial Statement 2021Document3 pagesAnnual Financial Statement 2021kofiNo ratings yet

- Assignmnt No 5. ASF - ROLL NO 18550920-010-186Document9 pagesAssignmnt No 5. ASF - ROLL NO 18550920-010-186Babli BabliNo ratings yet

- HorizontalDocument4 pagesHorizontal30 Odicta, Justine AnneNo ratings yet

- Statement of Profit and Losss Account For The Year Ended 31 ST March 2019Document9 pagesStatement of Profit and Losss Account For The Year Ended 31 ST March 2019Chirag SinghNo ratings yet

- Fusen Pharmaceutical Company Limited 福 森 藥 業 有 限 公 司Document22 pagesFusen Pharmaceutical Company Limited 福 森 藥 業 有 限 公 司in resNo ratings yet

- Appendix 1 To 5Document13 pagesAppendix 1 To 5Adil SaleemNo ratings yet

- Spring 2023 - ACC501 - 1Document3 pagesSpring 2023 - ACC501 - 1Ghazanfar AliNo ratings yet

- 2022 12 11 08 24Document42 pages2022 12 11 08 24Detective CuriousNo ratings yet

- en PDFDocument49 pagesen PDFJ. BangjakNo ratings yet

- Rabichakra/Ridarc J.V.: Balance SheetDocument8 pagesRabichakra/Ridarc J.V.: Balance SheetNayan MallaNo ratings yet

- Ultratech Cement Ltd. (India) : SourceDocument6 pagesUltratech Cement Ltd. (India) : SourceDivyagarapatiNo ratings yet

- Expressed in Canadian Dollars ($ CAD), Unaudited: Digital Bull Technologies LTDDocument5 pagesExpressed in Canadian Dollars ($ CAD), Unaudited: Digital Bull Technologies LTDDishant KhanejaNo ratings yet

- Balance Sheet: 2016 2017 2018 Assets Non-Current AssetsDocument6 pagesBalance Sheet: 2016 2017 2018 Assets Non-Current AssetsAhsan KamranNo ratings yet

- Year 2009 2008: Johnson & Johnson Balance Sheet (In Millions of USD)Document14 pagesYear 2009 2008: Johnson & Johnson Balance Sheet (In Millions of USD)ujjwal26No ratings yet

- WSP Financial Analysis V1.4Document68 pagesWSP Financial Analysis V1.4maruthimallepalliNo ratings yet

- Nepsealpha Export Price OHL 2023-10-06 2023-10-26Document1 pageNepsealpha Export Price OHL 2023-10-06 2023-10-26Manita KunwarNo ratings yet

- Nepsealpha Export Price NABIL 2020-10-06 2023-10-26Document15 pagesNepsealpha Export Price NABIL 2020-10-06 2023-10-26Manita KunwarNo ratings yet

- Camel Analysis India RankingDocument15 pagesCamel Analysis India RankingManita KunwarNo ratings yet

- Capital BudgetingDocument8 pagesCapital BudgetingManita KunwarNo ratings yet

- Business Development Strategy For Specialty CoffeeDocument11 pagesBusiness Development Strategy For Specialty CoffeeManita KunwarNo ratings yet

- Internationalization Project - Nepalese Sustainable Tea - Coffee in EuropeDocument2 pagesInternationalization Project - Nepalese Sustainable Tea - Coffee in EuropeManita KunwarNo ratings yet

- Final Simulation HRDocument39 pagesFinal Simulation HRManita KunwarNo ratings yet

- Pricing Strategy For ItalyDocument5 pagesPricing Strategy For ItalyManita KunwarNo ratings yet

- Zain KazmiDocument28 pagesZain KazmiZainKazmiNo ratings yet

- Lange 4e Chapter 2 End of Chapter SolutionsDocument9 pagesLange 4e Chapter 2 End of Chapter Solutionsdaddy bobaNo ratings yet

- Conceptual Framework PAS 1 With Answer KeyDocument11 pagesConceptual Framework PAS 1 With Answer KeyRichel Armayan67% (21)

- 2021 Tutorial 9 Nov26 Problem SheetDocument7 pages2021 Tutorial 9 Nov26 Problem SheetdsfghNo ratings yet

- LBO Case Study - Volta Electronics Co. - v3Document14 pagesLBO Case Study - Volta Electronics Co. - v3madamaNo ratings yet

- CreditSights - Adani Group - 23 August 2022Document16 pagesCreditSights - Adani Group - 23 August 2022Krish Patel100% (1)

- Module 2 - Sources of FinanceDocument50 pagesModule 2 - Sources of FinanceBheemeswar ReddyNo ratings yet

- Opening of Business End of Year 2Document10 pagesOpening of Business End of Year 2Mhd RahmanNo ratings yet

- AFM-2019 Course HandoutDocument2 pagesAFM-2019 Course HandoutMeconNo ratings yet

- Merger Demerger Acquisiiton and Transaction AdvisoryDocument48 pagesMerger Demerger Acquisiiton and Transaction AdvisoryErica DsouzaNo ratings yet

- Icici DmartDocument6 pagesIcici DmartGOUTAMNo ratings yet

- F7irl 2010 Dec AnsDocument11 pagesF7irl 2010 Dec AnsNghiêm Thị Mai AnhNo ratings yet

- Bonus ShareDocument3 pagesBonus ShareManjit Mohan ShreevastavaNo ratings yet

- ACCT801 219 Assignment 2 TemplateDocument2 pagesACCT801 219 Assignment 2 TemplateAcademic ServicesNo ratings yet

- Problem I Philippine ViewpointDocument14 pagesProblem I Philippine ViewpointAnonymous PBLfEOJNo ratings yet

- A Study On Financial Performance Using Ratio Analysis at Emami LTDDocument49 pagesA Study On Financial Performance Using Ratio Analysis at Emami LTDglorydharmaraj100% (4)

- FAR Assignment - 2Document7 pagesFAR Assignment - 2Melvin ShajiNo ratings yet

- Pertemuan 9BDocument36 pagesPertemuan 9Bleny aisyahNo ratings yet

- Business Plan - Ent-AssignmentDocument19 pagesBusiness Plan - Ent-AssignmentRichard Simon Kisitu100% (2)

- Corporatisation and Demutualisation of Stock Exchanges: I. What Is Corporatis-Ation and Demutuali - Sation?Document5 pagesCorporatisation and Demutualisation of Stock Exchanges: I. What Is Corporatis-Ation and Demutuali - Sation?Ashish UpadhyayaNo ratings yet

- Review of Financial Statement Preparation, Analysis and InterpretationDocument37 pagesReview of Financial Statement Preparation, Analysis and InterpretationJC AppartelleNo ratings yet

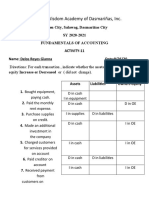

- Legacy of Wisdom Academy of Dasmariñas, IncDocument4 pagesLegacy of Wisdom Academy of Dasmariñas, InczavriaNo ratings yet

- Venture Capital PDFDocument94 pagesVenture Capital PDFRitu MehtaNo ratings yet

- Cost and Management Accounting 2 CHAPTER 1Document44 pagesCost and Management Accounting 2 CHAPTER 1chuchuNo ratings yet

- CH 12Document3 pagesCH 12vivien0% (1)

- Financial Planning and Forecasting ProForma Financial StatementsDocument9 pagesFinancial Planning and Forecasting ProForma Financial StatementsLm MuhammadNo ratings yet

- ACG 2021 Chapter 1 Power Points S15 After Lecture On 1-20-15Document84 pagesACG 2021 Chapter 1 Power Points S15 After Lecture On 1-20-15Benjamin Lott100% (1)

- Security Analysis Project 3Document11 pagesSecurity Analysis Project 3Yashra NaveedNo ratings yet

- S.Chapter 4. The Financial Statements Analyis v2Document44 pagesS.Chapter 4. The Financial Statements Analyis v2Ngọc HuyềnNo ratings yet

- Federal Bank ValuationDocument8 pagesFederal Bank ValuationPragathi T NNo ratings yet

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Risk Management: Concepts and Guidance, Fifth EditionFrom EverandRisk Management: Concepts and Guidance, Fifth EditionRating: 4.5 out of 5 stars4.5/5 (10)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Data Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBIFrom EverandData Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBINo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (35)