You might also like

- Tarafarma Worksheet Januari 2017Document2 pagesTarafarma Worksheet Januari 2017Nazla HanifaNo ratings yet

- CAD Schedule Consolidated Income ReportDocument5 pagesCAD Schedule Consolidated Income Reportm habiburrahman55No ratings yet

- Mid Term Review AnswersDocument12 pagesMid Term Review AnswersManasi ChitnisNo ratings yet

- NlktaDocument9 pagesNlktaYến Hoàng HảiNo ratings yet

- CORRECTION-PEN-FINALDocument21 pagesCORRECTION-PEN-FINALmpa2k22No ratings yet

- Group Aissignment - AnswerDocument15 pagesGroup Aissignment - AnswerDuyên Lê Ngọc TriềuNo ratings yet

- 2022 Academic Writing GuideDocument7 pages2022 Academic Writing GuideNamita GoburdhanNo ratings yet

- Quiz Lab AkmDocument20 pagesQuiz Lab AkmAdib PramanaNo ratings yet

- WorksheetDocument37 pagesWorksheetKim FloresNo ratings yet

- Investments in Financial Instruments CompleteDocument34 pagesInvestments in Financial Instruments CompleteDenise CruzNo ratings yet

- 2019 Unit 3 Outcome 2 Solution BookDocument10 pages2019 Unit 3 Outcome 2 Solution BookLachlan McFarlandNo ratings yet

- Checklist - Roto Pumps Limited FY 18-19Document6 pagesChecklist - Roto Pumps Limited FY 18-19Shubham SinuNo ratings yet

- Lite Inc. (B)Document22 pagesLite Inc. (B)sankalp_iimNo ratings yet

- SCM Stimulation - Preetika ChopraDocument5 pagesSCM Stimulation - Preetika ChopraPreetika ChopraNo ratings yet

- Vertical Income Statement and Balance Sheet for Jyoti LtdDocument6 pagesVertical Income Statement and Balance Sheet for Jyoti LtdAravind ShekharNo ratings yet

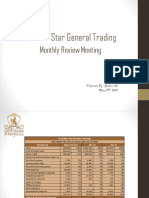

- Al Kamil Star Presentation 09.05.15Document10 pagesAl Kamil Star Presentation 09.05.15wesamNo ratings yet

- Cashflow QuestionDocument2 pagesCashflow QuestionMick MingleNo ratings yet

- Anniversary CompanyDocument3 pagesAnniversary CompanyKris Anne Delos SantosNo ratings yet

- Session 6Document15 pagesSession 6Hamza BennisNo ratings yet

- ACCP 5000 Test 2 Review ClassDocument26 pagesACCP 5000 Test 2 Review ClassDang ThanhNo ratings yet

- Annual Budget Planner SummaryDocument2 pagesAnnual Budget Planner SummaryvijayNo ratings yet

- Dashboard - SAI - PreviewReports - 2011Document73 pagesDashboard - SAI - PreviewReports - 2011Oh Oh OhNo ratings yet

- Class Practice Qs - Inventory Systems SolutionDocument6 pagesClass Practice Qs - Inventory Systems SolutionbaigsadanNo ratings yet

- Accounts Worksheet For TanDocument3 pagesAccounts Worksheet For TanTan ArrowNo ratings yet

- Variable Costing April Revenues 8,400,000Document10 pagesVariable Costing April Revenues 8,400,000Hiền NguyễnNo ratings yet

- Inventory Valuation - Practice QuestionsDocument3 pagesInventory Valuation - Practice QuestionsAhmad NawazNo ratings yet

- Sample Questions and Solutions - Final ExamDocument4 pagesSample Questions and Solutions - Final ExamNadjah JNo ratings yet

- Excel 02Document15 pagesExcel 02Jahid RahmanNo ratings yet

- FIN1161 - Introduction To Finance For Business - Report 1-Case Scenario Briefs - 2023-24Document2 pagesFIN1161 - Introduction To Finance For Business - Report 1-Case Scenario Briefs - 2023-24Kiên NguyễnNo ratings yet

- Accounting SystemDocument36 pagesAccounting SystemMaeNo ratings yet

- ACCT2511 Topic 2 Tutorial Solutions STUDENTDocument8 pagesACCT2511 Topic 2 Tutorial Solutions STUDENTKJSAdNo ratings yet

- Inventory (Questions) : Question No. H-1Document4 pagesInventory (Questions) : Question No. H-1manadish nawazNo ratings yet

- Jupiter Store - Soln - Completing The Accounting CycleDocument10 pagesJupiter Store - Soln - Completing The Accounting CycleMariella Olympia PanuncialesNo ratings yet

- Year 3 Expenses and Cashflow ForecastDocument1 pageYear 3 Expenses and Cashflow ForecastTully HamutenyaNo ratings yet

- Session 7Document20 pagesSession 7Hamza BennisNo ratings yet

- 6gbr 2006 Dec QDocument9 pages6gbr 2006 Dec Qapi-19836745No ratings yet

- Trading and Profit & Loss A/C: Liabilities Amt Assets AmtDocument6 pagesTrading and Profit & Loss A/C: Liabilities Amt Assets Amtshubho karrNo ratings yet

- Practice Session - 14 - MayDocument18 pagesPractice Session - 14 - MayprabhuNo ratings yet

- Afe 3582Document6 pagesAfe 3582sarah josephNo ratings yet

- Problem 3 Chapter1 (Accounting in Action)Document4 pagesProblem 3 Chapter1 (Accounting in Action)Amelia LarasatiNo ratings yet

- Questions Chapter 3 No.11: PEROT CORPORATION - Patay2 Chip ProjectDocument6 pagesQuestions Chapter 3 No.11: PEROT CORPORATION - Patay2 Chip ProjectddNo ratings yet

- AP 5905Q InventoriesDocument3 pagesAP 5905Q Inventoriesaldrin elsisuraNo ratings yet

- QuizDocument41 pagesQuizbar barNo ratings yet

- Case Study AUSCISEDocument2 pagesCase Study AUSCISEsharielles /No ratings yet

- Cost Accounting: The Institute of Chartered Accountants of PakistanDocument4 pagesCost Accounting: The Institute of Chartered Accountants of PakistanShehrozSTNo ratings yet

- Flagstaff ClosingDocument1 pageFlagstaff ClosingSteven SandersonNo ratings yet

- 2003 JuneDocument8 pages2003 JuneSherif AwadNo ratings yet

- Problem 4-4 Dindorf CompanyDocument5 pagesProblem 4-4 Dindorf Companymelati50% (4)

- 1658247187MB-103 [O-278]Document7 pages1658247187MB-103 [O-278]Chaithanya ChaithuNo ratings yet

- Tugas Besar 2 - Arditia Zanuba - 43220120069Document3 pagesTugas Besar 2 - Arditia Zanuba - 43220120069LusianaNo ratings yet

- 16 Inventory ValuationDocument28 pages16 Inventory ValuationSidra MalikNo ratings yet

- Elaine WorkDocument8 pagesElaine WorkElaine CasamaNo ratings yet

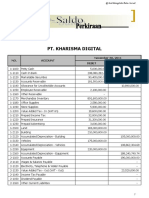

- Kunci Jawaban Pt. Kharisma DigitalDocument91 pagesKunci Jawaban Pt. Kharisma DigitalSanti Mulya100% (3)

- Accounting Case 3Document9 pagesAccounting Case 3RAAFI DAPSKINo ratings yet

- Music Mart FormatDocument4 pagesMusic Mart FormatOggy SharmaNo ratings yet

- Analisis Finansial Usaha Tani (Bayam)Document12 pagesAnalisis Finansial Usaha Tani (Bayam)Usamah RofiNo ratings yet

- Chapter 6 - Preparation of Financial StatementsDocument10 pagesChapter 6 - Preparation of Financial StatementspolymeianNo ratings yet

- Quijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodDocument4 pagesQuijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodzairahNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Chapter 4: Liquidation Based Valuation MC Problems 1 WW IncDocument153 pagesChapter 4: Liquidation Based Valuation MC Problems 1 WW IncKim BihagNo ratings yet

- Application of Fixed Asset DepreciationDocument4 pagesApplication of Fixed Asset DepreciationGiffari Ibnu ToriqNo ratings yet

- Ross Fundamentals of Corporate Finance 13e CH03Document32 pagesRoss Fundamentals of Corporate Finance 13e CH03muhammad AdeelNo ratings yet

- Chapter 8. Reversal Trading StrategiesDocument38 pagesChapter 8. Reversal Trading StrategiesЕкатерина ВладиславовнаNo ratings yet

- Adjudication Order Against 18 Entities in The Matter of Goldstone Technologies Ltd.Document34 pagesAdjudication Order Against 18 Entities in The Matter of Goldstone Technologies Ltd.Shyam SunderNo ratings yet

- Insurance Core PrinciplesDocument32 pagesInsurance Core PrinciplesJorkosNo ratings yet

- SEBI and Indian Securities MarketDocument47 pagesSEBI and Indian Securities MarketsaneshNo ratings yet

- R31 Free Cash Flow Valuation Q Bank PDFDocument8 pagesR31 Free Cash Flow Valuation Q Bank PDFZidane Khan100% (1)

- RHB Report RHB Malaysia Morning Cuppa 23 June 2023 Edited 954530617140640336494e31c8e866 - 1687479574Document7 pagesRHB Report RHB Malaysia Morning Cuppa 23 June 2023 Edited 954530617140640336494e31c8e866 - 1687479574AMMAR THAQIF ABDUL RAHAMANNo ratings yet

- Csec Pob January 2013 p2Document6 pagesCsec Pob January 2013 p2Ikera ClarkeNo ratings yet

- Fundamentos de Marketing - PHILIP KOTLER Y GARY ARMSTRONG - Zsyszleaux.s2 - Page 1 - 498 - Flip PDF Online - PubHTML5Document498 pagesFundamentos de Marketing - PHILIP KOTLER Y GARY ARMSTRONG - Zsyszleaux.s2 - Page 1 - 498 - Flip PDF Online - PubHTML5ALEXIS AARON AGURTO LOPEZNo ratings yet

- Presentation 4 - Basics of Capital Budgeting (Draft)Document27 pagesPresentation 4 - Basics of Capital Budgeting (Draft)sanjuladasanNo ratings yet

- The Triadic "Politics-Economics-EthicsDocument293 pagesThe Triadic "Politics-Economics-EthicsLeonidaNeamtuNo ratings yet

- Analyze financial statements with this SEO-optimized multiple choice quizDocument15 pagesAnalyze financial statements with this SEO-optimized multiple choice quizPrincess Corine BurgosNo ratings yet

- Gold Prices in India GraphDocument3 pagesGold Prices in India GraphArmandoNo ratings yet

- Assignment 1 - Back Bay Battery Simulation - Shreya Gupta (Final)Document10 pagesAssignment 1 - Back Bay Battery Simulation - Shreya Gupta (Final)Shreya Gupta100% (3)

- Chapter 13 CASH FLOWDocument2 pagesChapter 13 CASH FLOWKezia N. ApriliaNo ratings yet

- FM16 Ch26 Tool KitDocument21 pagesFM16 Ch26 Tool KitAdamNo ratings yet

- Morningstar - Report 636d1778e26a17cb57991bce KHCDocument21 pagesMorningstar - Report 636d1778e26a17cb57991bce KHCcmcbuyersgNo ratings yet

- PAYPAL MONEY MARKET FUND PROSPECTUSDocument56 pagesPAYPAL MONEY MARKET FUND PROSPECTUSsamclerryNo ratings yet

- B Ing LM NeroDocument11 pagesB Ing LM NerojezzenNo ratings yet

- FSD7Document2 pagesFSD7Leo the BulldogNo ratings yet

- NUS MBA Investment Analysis ModuleDocument4 pagesNUS MBA Investment Analysis ModuleNikhilNo ratings yet

- Corporate RestructuringDocument55 pagesCorporate Restructuringrashdi1989100% (2)

- Nature of Capital Budgeting & Types of Capital ProjectsDocument11 pagesNature of Capital Budgeting & Types of Capital ProjectsMitesh KumarNo ratings yet

- Co Location ScamDocument3 pagesCo Location ScamcdhjvkfyutdtjyNo ratings yet

- ETF Fact Sheet-Janney Global Water FundDocument2 pagesETF Fact Sheet-Janney Global Water Fundbijon11No ratings yet

- Secom limited debenture accountsDocument2 pagesSecom limited debenture accountsLakshmi PanayappanNo ratings yet

- FINA 1310 Spring 2021 Corporate Finance SessionDocument2 pagesFINA 1310 Spring 2021 Corporate Finance Sessionadmin AdminNo ratings yet

![1658247187MB-103 [O-278]](https://imgv2-2-f.scribdassets.com/img/document/719949228/149x198/9a40317e4b/1712222700?v=1)