You might also like

- Summary of David A. Moss's A Concise Guide to Macroeconomics, Second EditionFrom EverandSummary of David A. Moss's A Concise Guide to Macroeconomics, Second EditionNo ratings yet

- Valix Chapter 20Document22 pagesValix Chapter 20criszel4sobejanaNo ratings yet

- The Open EconomyDocument10 pagesThe Open Economymacurri100% (1)

- Canevas HND 2020 - Vol 1Document293 pagesCanevas HND 2020 - Vol 1rita tamohNo ratings yet

- Risk Appetite PresentationDocument10 pagesRisk Appetite PresentationAntonyNo ratings yet

- Week 6 The is-LM ModelDocument32 pagesWeek 6 The is-LM ModelBiswajit DasNo ratings yet

- Inflation-Conscious Investments: Avoid the most common investment pitfallsFrom EverandInflation-Conscious Investments: Avoid the most common investment pitfallsNo ratings yet

- Sample Life Exam QuestionsDocument10 pagesSample Life Exam Questionsrita tamohNo ratings yet

- 8hczsq TicketsDocument6 pages8hczsq TicketsHafiz Zain SheikhNo ratings yet

- Barangay Final Inventory and Turnover TreasurerDocument1 pageBarangay Final Inventory and Turnover TreasurerDilg Concepcion100% (1)

- Assignment of Money & Capital Market: University of Central Punjab LahoreDocument11 pagesAssignment of Money & Capital Market: University of Central Punjab LahoreALINo ratings yet

- Marco-Economics Assignment: Topic: Is-Lm ModelDocument6 pagesMarco-Economics Assignment: Topic: Is-Lm ModelVishwanath Sagar100% (1)

- Goods and Money Market: Unit 3Document28 pagesGoods and Money Market: Unit 3Mrigesh AgarwalNo ratings yet

- Crowding Out and Fiscal PolicyDocument9 pagesCrowding Out and Fiscal Policykanishks1311No ratings yet

- Macroeconomics Assignment: in Lieu of Missed QuizDocument9 pagesMacroeconomics Assignment: in Lieu of Missed Quizakshay rautNo ratings yet

- Advanced Macro Economics 3rd Day LectureDocument7 pagesAdvanced Macro Economics 3rd Day LectureRoentgen Djon Kaiser IgnacioNo ratings yet

- Quiz # 1, Answers: 14.02 Principles of MacroeconomicsDocument6 pagesQuiz # 1, Answers: 14.02 Principles of MacroeconomicsEmmanuel MbonaNo ratings yet

- Macroeconomics Review Course Lecture NotesDocument17 pagesMacroeconomics Review Course Lecture NotesAhim Raj JoshiNo ratings yet

- Resume The Open Economy NovitasariDocument7 pagesResume The Open Economy NovitasariAfny HnpiNo ratings yet

- Chapter 4 Open Economic SystemDocument65 pagesChapter 4 Open Economic Systemtigabuyeshiber034No ratings yet

- The Small Open Economy ISLM Model: Henry Thompson International EconomicsDocument13 pagesThe Small Open Economy ISLM Model: Henry Thompson International Economicsfakhri_hasanovNo ratings yet

- University of The Philippines School of Economics: Study Guide No. 2Document5 pagesUniversity of The Philippines School of Economics: Study Guide No. 2Djj TrongcoNo ratings yet

- Macro Aliftia YasinDocument9 pagesMacro Aliftia YasinAfny HnpiNo ratings yet

- Saving and InvestmentDocument8 pagesSaving and Investmentyujie zhuNo ratings yet

- Philips CurveDocument7 pagesPhilips CurveMohammad Zeeshan BalochNo ratings yet

- Felicia Irene Week 7Document27 pagesFelicia Irene Week 7felicia ireneNo ratings yet

- ChapterDocument42 pagesChapterIf'idatur rosyidahNo ratings yet

- Ecological Economics-Principles and Applications-8Document50 pagesEcological Economics-Principles and Applications-8Edwin JoyoNo ratings yet

- ECO3 PPT 3Document9 pagesECO3 PPT 3idcidkxxNo ratings yet

- Income Determination Model Including Money and InterestDocument11 pagesIncome Determination Model Including Money and Interestsunnysainani1No ratings yet

- What Determines The Demand ForDocument25 pagesWhat Determines The Demand ForSuruchi SinghNo ratings yet

- Prayoga Dwi Nugraha - Summary CH 11Document10 pagesPrayoga Dwi Nugraha - Summary CH 11Prayoga Dwi NugrahaNo ratings yet

- 02 Alejandro Rodriguez 37-58Document22 pages02 Alejandro Rodriguez 37-58Holger QuispeNo ratings yet

- Quantitative Recession PredictionDocument10 pagesQuantitative Recession PredictionRd PatelNo ratings yet

- Macroeconomics 6th Edition Blanchard Solutions Manual 1Document36 pagesMacroeconomics 6th Edition Blanchard Solutions Manual 1luissandersocraiyznfw100% (27)

- Government SpendingDocument11 pagesGovernment SpendingRow TourNo ratings yet

- Macroeconomics 6th Edition Blanchard Solutions Manual 1Document6 pagesMacroeconomics 6th Edition Blanchard Solutions Manual 1shirley100% (49)

- Macroeconomics 6Th Edition Blanchard Solutions Manual Full Chapter PDFDocument27 pagesMacroeconomics 6Th Edition Blanchard Solutions Manual Full Chapter PDFdonna.morales754100% (12)

- What Macroeconomics Is All About ?: Ratna K. ShresthaDocument36 pagesWhat Macroeconomics Is All About ?: Ratna K. ShresthaShavon ZhangNo ratings yet

- Quiz #3, Answers: 14.02 Principles of MacroeconomicsDocument10 pagesQuiz #3, Answers: 14.02 Principles of MacroeconomicsEmmanuel MbonaNo ratings yet

- Aggregate Demand Importance Components Curve LimitationsDocument11 pagesAggregate Demand Importance Components Curve LimitationsExport ImbdNo ratings yet

- Chapter 3Document100 pagesChapter 3HayamnotNo ratings yet

- Chap13 EssayDocument3 pagesChap13 EssayThuỳ AnNo ratings yet

- Macro EconomicsDocument7 pagesMacro EconomicsShivam GoelNo ratings yet

- Relationship Between GDP, Consumption, Savings and InvestmentDocument16 pagesRelationship Between GDP, Consumption, Savings and InvestmentBharath NaikNo ratings yet

- Questions To Lecture 7 - IS-LM Model and Aggregate DemandDocument6 pagesQuestions To Lecture 7 - IS-LM Model and Aggregate DemandMandar Priya Phatak100% (2)

- MacroeconomicsDocument18 pagesMacroeconomicsAbir RahmanNo ratings yet

- Quiz #3, Answers: 14.02 Principles of MacroeconomicsDocument10 pagesQuiz #3, Answers: 14.02 Principles of MacroeconomicsrohityadavalldNo ratings yet

- Macroeconomics II HandoutDocument106 pagesMacroeconomics II HandoutMrku HyleNo ratings yet

- Chapter - 04 - Deep Dive - DPDocument43 pagesChapter - 04 - Deep Dive - DPDilshansasankayahoo.comNo ratings yet

- Chapter Three Aggregate Demand & Aggregate SupplyDocument44 pagesChapter Three Aggregate Demand & Aggregate SupplyHasbiyallah Weni'imal WakiilNo ratings yet

- Prayoga Dwi Nugraha - Summary CH 10Document9 pagesPrayoga Dwi Nugraha - Summary CH 10Prayoga Dwi NugrahaNo ratings yet

- Unemployment, Stock MarketsDocument4 pagesUnemployment, Stock MarketsfecitusNo ratings yet

- Macro 4Document15 pagesMacro 4Rajesh GargNo ratings yet

- C) IS LM ModelDocument19 pagesC) IS LM ModelJeny ChatterjeeNo ratings yet

- Monetary FiscalDocument4 pagesMonetary FiscalKiranNo ratings yet

- How To Calculate National SavingsDocument6 pagesHow To Calculate National SavingsQazi QaziNo ratings yet

- Macroeconomics IIDocument371 pagesMacroeconomics IIanesahmedtofik932No ratings yet

- (Macroeconomics) Topic 8-3Document12 pages(Macroeconomics) Topic 8-3DavidsarneyNo ratings yet

- Socio-Political Instability and Growth DynamicsDocument14 pagesSocio-Political Instability and Growth DynamicsMwimbaNo ratings yet

- Chapter 4Document26 pagesChapter 4HayamnotNo ratings yet

- Ecodev Midterm Notes 2Document3 pagesEcodev Midterm Notes 2Nichole BombioNo ratings yet

- Macro Note CardsDocument18 pagesMacro Note CardsSankar AdhikariNo ratings yet

- Working of IS-LM Modal ASS4 PDFDocument25 pagesWorking of IS-LM Modal ASS4 PDFSanu BoseNo ratings yet

- IS/LM Model: HistoryDocument6 pagesIS/LM Model: Historyhimanshu_ymca01No ratings yet

- Lukong Blessing Exercise 08 FormationDocument7 pagesLukong Blessing Exercise 08 Formationrita tamohNo ratings yet

- TEMATIO SANDRINE'S DATA - New1Document49 pagesTEMATIO SANDRINE'S DATA - New1rita tamohNo ratings yet

- 31 Yeti Tatsie Elodie EXO 31 COSTDocument7 pages31 Yeti Tatsie Elodie EXO 31 COSTrita tamohNo ratings yet

- 03 Tazoah Francis Exercise 03 CostDocument4 pages03 Tazoah Francis Exercise 03 Costrita tamohNo ratings yet

- Introduction To Law and Fundamental RightsDocument55 pagesIntroduction To Law and Fundamental Rightsrita tamohNo ratings yet

- PBG207 TC+CorrDocument20 pagesPBG207 TC+Corrrita tamohNo ratings yet

- PBG208 TC+CorrDocument25 pagesPBG208 TC+Corrrita tamohNo ratings yet

- OHADA Uniform Act 2000 Harmonization Accounts of Enterprises1Document13 pagesOHADA Uniform Act 2000 Harmonization Accounts of Enterprises1rita tamohNo ratings yet

- Esg Budget Management Final VersionDocument66 pagesEsg Budget Management Final Versionrita tamohNo ratings yet

- Comparative Analysis PH and JPNDocument37 pagesComparative Analysis PH and JPNYla Zennia VistavillaNo ratings yet

- Deed of Absolute SaleDocument2 pagesDeed of Absolute SaleDEXTER ARGONCILLONo ratings yet

- DR R K Sharma 13 FebDocument1 pageDR R K Sharma 13 FebVinay SharmaNo ratings yet

- Holistic Risk AssessmentDocument13 pagesHolistic Risk AssessmentdivakdsNo ratings yet

- Return To TOC: Dowty Propellers Standard Practices ManualDocument32 pagesReturn To TOC: Dowty Propellers Standard Practices ManualNicolás PiratovaNo ratings yet

- Aptis Speakers General Advanced - 2Document77 pagesAptis Speakers General Advanced - 2pamefdezNo ratings yet

- Saregama Carvaan Go Warranty 1.0Document4 pagesSaregama Carvaan Go Warranty 1.0Ashm-ashu SharmaNo ratings yet

- Test Bank For Financial Reporting and Analysis, 8th Edition, Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt Leonard SofferDocument36 pagesTest Bank For Financial Reporting and Analysis, 8th Edition, Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt Leonard Soffervespersrealizeravzo100% (19)

- TCO Strategic Planning Survey ResultsDocument16 pagesTCO Strategic Planning Survey ResultsWassim HuwariNo ratings yet

- DME-Components en 2022 FinalDocument680 pagesDME-Components en 2022 FinalDavid ChavesNo ratings yet

- Wood Therapy Massage ToolDocument14 pagesWood Therapy Massage ToolMuhammad Ayan MalikNo ratings yet

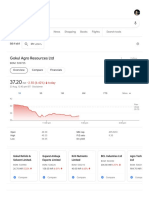

- Gokul Agro Resources LTD: Videos Images Maps News Shopping Books Flights Search ToolsDocument5 pagesGokul Agro Resources LTD: Videos Images Maps News Shopping Books Flights Search ToolsManish SinghNo ratings yet

- FINS5513 Lecture 3A: Capital Allocation and Optimal Risky PortfoliosDocument37 pagesFINS5513 Lecture 3A: Capital Allocation and Optimal Risky Portfolios萬之晨No ratings yet

- The Fashion Rack - FinalDocument17 pagesThe Fashion Rack - FinalAyanna CameroNo ratings yet

- Macroeconomics & The Global EconomyDocument22 pagesMacroeconomics & The Global Economysubash thapaNo ratings yet

- Auto Secure Private Car Package PolicyDocument9 pagesAuto Secure Private Car Package PolicyKaran PrabhakarNo ratings yet

- Supply and Demand PracticeDocument5 pagesSupply and Demand PracticeHeather McCutchenNo ratings yet

- ShitalDocument114 pagesShitalShital PatilNo ratings yet

- Logbook Gac022Document6 pagesLogbook Gac022PaulinaNo ratings yet

- Bill of Quantities Electrical PDFDocument19 pagesBill of Quantities Electrical PDFDENISNo ratings yet

- Tybms Sem5 HRPCM Apr19Document3 pagesTybms Sem5 HRPCM Apr19miracle worldNo ratings yet

- OANDA Currency ConverterDocument2 pagesOANDA Currency Convertertiger2020No ratings yet

- A Research Agenda For Economic Anthropology) Collective Economic ActorsDocument15 pagesA Research Agenda For Economic Anthropology) Collective Economic ActorsANA PAOLA HUESCA LOREDONo ratings yet

- Bindu EXPENSES SHEETDocument1 pageBindu EXPENSES SHEETKrishna ReddyNo ratings yet

- NEMSA Chargeable FeesDocument11 pagesNEMSA Chargeable FeesMubarak AleemNo ratings yet

- Basics On Postings and The Main Database Tables in Asset AccountingDocument17 pagesBasics On Postings and The Main Database Tables in Asset Accountingsf69vNo ratings yet