You might also like

- Current JSS 2 BUSINESS STUDIES 3RD TERMDocument34 pagesCurrent JSS 2 BUSINESS STUDIES 3RD TERMpalmer okiemuteNo ratings yet

- Petty Cash BookDocument4 pagesPetty Cash Bookdayna davisNo ratings yet

- Petty Cashbook NotesDocument6 pagesPetty Cashbook NotesBamidele AdegboyeNo ratings yet

- Cash Book NotesDocument4 pagesCash Book NotesJoRaccoonaNo ratings yet

- Coursebook Answers: Answers To Test Yourself QuestionsDocument3 pagesCoursebook Answers: Answers To Test Yourself QuestionsDonatien Oulaii87% (15)

- Coursebook Chapter 5 Answers PDFDocument3 pagesCoursebook Chapter 5 Answers PDFXx Yung Wei Chin100% (1)

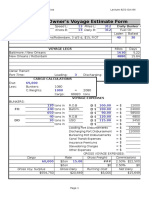

- Owner's Voyage Estimate Form: Daily Bunker ConsumptionDocument2 pagesOwner's Voyage Estimate Form: Daily Bunker ConsumptionJuan Ramón FuentesNo ratings yet

- Petty Cash Book - 21.3XDocument5 pagesPetty Cash Book - 21.3XRichelle HUSBANDSNo ratings yet

- Three Column Cash Book NotesDocument7 pagesThree Column Cash Book NotesTrishana GreenNo ratings yet

- Debtors Oustanding StatementDocument6 pagesDebtors Oustanding StatementDilan Maduranga Fransisku ArachchiNo ratings yet

- Bank ReconDocument6 pagesBank Reconacuna.alexNo ratings yet

- Jawaban Ud WirastriDocument17 pagesJawaban Ud WirastriDevitaNo ratings yet

- Solution Manual For Accounting 25Th Edition Warren Reeve Duchac 1133607608 978113360760 Full Chapter PDFDocument36 pagesSolution Manual For Accounting 25Th Edition Warren Reeve Duchac 1133607608 978113360760 Full Chapter PDFjohn.twilley531100% (16)

- Cash Book: Description V.No - PR Amount (RS) Date Description V.No. PR Amount (RS)Document4 pagesCash Book: Description V.No - PR Amount (RS) Date Description V.No. PR Amount (RS)Rudrasish BeheraNo ratings yet

- Solution Manual For Accounting 25th Edition Warren Reeve Duchac 1133607608 9781133607601Document36 pagesSolution Manual For Accounting 25th Edition Warren Reeve Duchac 1133607608 9781133607601nicolemiddleton19081987ewg100% (22)

- Buku Besar Ud BuanaDocument23 pagesBuku Besar Ud BuanaNabilla ParamitaNo ratings yet

- Cashbook 140813004915 Phpapp02Document14 pagesCashbook 140813004915 Phpapp02Nishi YadavNo ratings yet

- Session 17 Journals 2 - ReturnsDocument7 pagesSession 17 Journals 2 - Returnsol.iv.e.a.gui.l.ar412No ratings yet

- Session 17 Journals 1 - Sales & PurchasesDocument10 pagesSession 17 Journals 1 - Sales & Purchasesol.iv.e.a.gui.l.ar412No ratings yet

- Chapter 5-Petty Cash Book 2023Document8 pagesChapter 5-Petty Cash Book 2023Joshua RuizNo ratings yet

- CCP102Document18 pagesCCP102api-3849444No ratings yet

- Double-Entry Bookkeeping: A Double-Entry Account Account Name Debit Side (DR) Credit Side (CR)Document5 pagesDouble-Entry Bookkeeping: A Double-Entry Account Account Name Debit Side (DR) Credit Side (CR)Veronica BaileyNo ratings yet

- Accounting 2Document4 pagesAccounting 2aromalsolteroNo ratings yet

- F5 Bafs 2 QueDocument13 pagesF5 Bafs 2 Queouo So方No ratings yet

- Aud 34PB2ND-1 PDFDocument1 pageAud 34PB2ND-1 PDFLove Sunshine BancaleNo ratings yet

- Praktek Ukk Akuntansi TP 2017-2018 IntanDocument27 pagesPraktek Ukk Akuntansi TP 2017-2018 Intanyuliani utamiNo ratings yet

- Chapter 4 - Mathematics of Merchandising 4.2 Cash Discounts & Terms of Payment (Invoices)Document3 pagesChapter 4 - Mathematics of Merchandising 4.2 Cash Discounts & Terms of Payment (Invoices)chantoniusNo ratings yet

- ACCO TestDocument6 pagesACCO TestvrindadevigtmNo ratings yet

- Preparing A Bank Reconciliation - Financial AccountingDocument14 pagesPreparing A Bank Reconciliation - Financial AccountingsninaricaNo ratings yet

- Solutions Manual For Century 21 Accounting, Advanced, 11e Claudia Bienias Gilbertson, Mark Lehman, Daniel Passalacq - CroppedDocument8 pagesSolutions Manual For Century 21 Accounting, Advanced, 11e Claudia Bienias Gilbertson, Mark Lehman, Daniel Passalacq - Croppedtutortype5No ratings yet

- 4 Preparing A Bank ReconciliationDocument9 pages4 Preparing A Bank ReconciliationSamuel DebebeNo ratings yet

- Atlas - Monika Umardi - 4122413220590Document10 pagesAtlas - Monika Umardi - 4122413220590WidiantiNo ratings yet

- Sources and Recording of Data 1Document5 pagesSources and Recording of Data 1MachelMDotAlexanderNo ratings yet

- Jawaban PADocument24 pagesJawaban PAvivi lewarNo ratings yet

- POA GR 10 Weeks 1-5 - Term 3Document29 pagesPOA GR 10 Weeks 1-5 - Term 3ZeeLazMursalinNo ratings yet

- Purchases JournalDocument18 pagesPurchases JournalHidalgo, John Christian MunarNo ratings yet

- 03 Books of Original Entry and Ledgers (I)Document16 pages03 Books of Original Entry and Ledgers (I)YU TaktakNo ratings yet

- In Class Exercise - 3 - Purchases and Cash Disbursements CycleDocument9 pagesIn Class Exercise - 3 - Purchases and Cash Disbursements CycleMatthew BraswellNo ratings yet

- Jurnal KhususDocument6 pagesJurnal KhususFanix Yostina DaelyNo ratings yet

- Usa Ma 21Document9 pagesUsa Ma 21Usama17No ratings yet

- Book KeepingDocument10 pagesBook KeepingOnyiNo ratings yet

- Cash Book NotesDocument2 pagesCash Book NotesRonaldo GhanyNo ratings yet

- AccountsDocument8 pagesAccountsWilliNo ratings yet

- CSEC Principles of Accounts SEC. 3-Balancing The BooksDocument18 pagesCSEC Principles of Accounts SEC. 3-Balancing The BooksEphraim PryceNo ratings yet

- FABM - L-10Document16 pagesFABM - L-10Seve HanesNo ratings yet

- Peta AWP FormDocument179 pagesPeta AWP FormBilly BlazerNo ratings yet

- Olwen Febry Irawan - Kuis Uts Apli Audit 2Document30 pagesOlwen Febry Irawan - Kuis Uts Apli Audit 2Olwen IrawanNo ratings yet

- 05 Posting To LedgerDocument2 pages05 Posting To LedgerTrisha Mae BrazaNo ratings yet

- Ch8 Cabook PDFDocument7 pagesCh8 Cabook PDFThiruvenkata ManiNo ratings yet

- Accounting Records-JournalDocument14 pagesAccounting Records-JournalBoi NonoNo ratings yet

- BSA2001-Principles of Accounting TOTAL: 100 Points Midterm Oct/2021 Name: Nguyen Quynh Trang Student ID: 1604171Document5 pagesBSA2001-Principles of Accounting TOTAL: 100 Points Midterm Oct/2021 Name: Nguyen Quynh Trang Student ID: 1604171Quỳnh Trang NguyễnNo ratings yet

- Revision QuestionsDocument5 pagesRevision QuestionsVishwa NirmalaNo ratings yet

- SCHNEIDERS (00006) Periodic Billing Statement Closing Date 02.17.2015 - RedactedDocument1 pageSCHNEIDERS (00006) Periodic Billing Statement Closing Date 02.17.2015 - Redactedlarry-612445No ratings yet

- Document 1312021 53807 AM ZrAxTn7pDocument8 pagesDocument 1312021 53807 AM ZrAxTn7pGisselle RodriguezNo ratings yet

- FnboDocument4 pagesFnboMaximusNo ratings yet

- Stop: 3118/04 1620 Dodge ST Omaha, NE 68197: Spiro G Sakellis 2563 123RD ST FLUSHING, NY 11354-1040Document4 pagesStop: 3118/04 1620 Dodge ST Omaha, NE 68197: Spiro G Sakellis 2563 123RD ST FLUSHING, NY 11354-1040Viktoria DenisenkoNo ratings yet

- Flat CostingDocument6 pagesFlat Costingridoy2146No ratings yet

- Unit 2 - Accounting TemplatesDocument13 pagesUnit 2 - Accounting TemplatesHsu WaiNo ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Session 14 Balance SheetDocument6 pagesSession 14 Balance Sheetol.iv.e.a.gui.l.ar412No ratings yet

- Session 15 Vertical and Horizontal FormatDocument4 pagesSession 15 Vertical and Horizontal Formatol.iv.e.a.gui.l.ar412No ratings yet

- Session 17 Journals 1 Exercise 2 RowlandDocument2 pagesSession 17 Journals 1 Exercise 2 Rowlandol.iv.e.a.gui.l.ar412No ratings yet

- Session 22 Capital and Revenue ExpenditureDocument3 pagesSession 22 Capital and Revenue Expenditureol.iv.e.a.gui.l.ar412No ratings yet

- Session 11 Closing Off Ledger AccountsDocument3 pagesSession 11 Closing Off Ledger Accountsol.iv.e.a.gui.l.ar412No ratings yet

- Session 12 Capital Account and Further Considerations For The Final AccountsDocument4 pagesSession 12 Capital Account and Further Considerations For The Final Accountsol.iv.e.a.gui.l.ar412No ratings yet

- Cash Chapter 5Document9 pagesCash Chapter 5yoantanNo ratings yet

- FSCS02 Granting Liquidation and Accounting For Cash AdvancesDocument12 pagesFSCS02 Granting Liquidation and Accounting For Cash AdvancesPauline Caceres AbayaNo ratings yet

- Summary Notes On Petty CashDocument4 pagesSummary Notes On Petty CashGio SantosNo ratings yet

- CH 07Document81 pagesCH 07Ismadth2918388No ratings yet

- Audit of CashDocument10 pagesAudit of CashJoannah maeNo ratings yet

- Accounting Manual PDFDocument226 pagesAccounting Manual PDFAnonymous 4W32x1SlL67% (3)

- Bgy. Disbursements Revised 5-8-07Document82 pagesBgy. Disbursements Revised 5-8-07AnnamaAnnamaNo ratings yet

- Narrative ReportDocument8 pagesNarrative ReportJohn Maynard Resquid SalazarNo ratings yet

- 2cycles DCPR FormatDocument5 pages2cycles DCPR FormatLibertad-Butuan MultibikesNo ratings yet

- CH 3 Practice Questions - N2 CDocument6 pagesCH 3 Practice Questions - N2 CSoputivong NhemNo ratings yet

- Cash and Internal Control: Ani Wilujeng Suryani, PHDDocument47 pagesCash and Internal Control: Ani Wilujeng Suryani, PHDRoby RohmadNo ratings yet

- DocxDocument16 pagesDocxLeah Mae NolascoNo ratings yet

- Let Check AACC124 PDFDocument13 pagesLet Check AACC124 PDFFatima Medriza DuranNo ratings yet

- 1 SOP Petty Cash ManagementDocument27 pages1 SOP Petty Cash ManagementMuhammad Julianto FardanNo ratings yet

- Appendix 48 - PCVDocument13 pagesAppendix 48 - PCVHelen Paragas Solivar AranetaNo ratings yet

- Sweta's L&TDocument52 pagesSweta's L&TRicha Sinha0% (1)

- Tugas Sia 2Document5 pagesTugas Sia 2vincent alvinNo ratings yet

- 2019 Vol 1 CH 1 AnswersDocument17 pages2019 Vol 1 CH 1 AnswersTatangNo ratings yet

- Non-Procurement Checklist v1.2Document53 pagesNon-Procurement Checklist v1.2FLORES CHARLESNo ratings yet

- Solution Manual Auditing by Espenilla MacariolaDocument158 pagesSolution Manual Auditing by Espenilla MacariolaPatrick Louie FormosoNo ratings yet

- Module 3 Cash and Cash EquivalentsDocument32 pagesModule 3 Cash and Cash Equivalentschuchu tv100% (1)

- Audit of Cash - Roque 2018Document87 pagesAudit of Cash - Roque 2018patrise sioson78% (9)

- Cash and Cash Equivalents Sample ProblemsDocument7 pagesCash and Cash Equivalents Sample ProblemsCamille Donaire LimNo ratings yet

- 7 Simple Steps To Improve Control Over Petty CashDocument9 pages7 Simple Steps To Improve Control Over Petty CashAudit DepartmentNo ratings yet

- VouchersDocument9 pagesVouchersRaviSankar100% (2)

- Audit 2-Prelim-Quiz 1 (1663899998)Document3 pagesAudit 2-Prelim-Quiz 1 (1663899998)Ella Mae Clavano NuicaNo ratings yet

- Rey Ocampo Online! FAR: Cash and Cash EquivalentsDocument3 pagesRey Ocampo Online! FAR: Cash and Cash EquivalentsMacy SantosNo ratings yet

- CH 2 Audit IIDocument9 pagesCH 2 Audit IIsamuel debebeNo ratings yet

- Accounting For CashDocument3 pagesAccounting For CashMichael BwireNo ratings yet

- Accounting For CashDocument9 pagesAccounting For CashNatty STAN100% (1)