You might also like

- Monthly Sales and Cost AnalysisDocument3 pagesMonthly Sales and Cost AnalysisGautam D50% (2)

- Statement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Document4 pagesStatement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Jayash KaushalNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Case 5Document12 pagesCase 5JIAXUAN WANGNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document6 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Mystic SportsDocument34 pagesMystic SportshelloNo ratings yet

- Sbi Car LoanDocument10 pagesSbi Car LoanShweta Yashwant Chalke100% (2)

- Variable Costing Case Part A SolutionDocument3 pagesVariable Costing Case Part A SolutionG, BNo ratings yet

- Costco2-Quiz End-TermDocument4 pagesCostco2-Quiz End-TermmhikeedelantarNo ratings yet

- Midterms I Answer KeyDocument5 pagesMidterms I Answer Keyaldric taclanNo ratings yet

- Q - Add or Drop A SegmentDocument1 pageQ - Add or Drop A SegmentIrahq Yarte TorrejosNo ratings yet

- Correct Amount of Inventory 677,500Document8 pagesCorrect Amount of Inventory 677,500Maria Kathreena Andrea AdevaNo ratings yet

- CH 3 Problem SolutionsDocument9 pagesCH 3 Problem SolutionsFrancisco PradoNo ratings yet

- Accounts Receivable, Accounts Payable, Sales and Purchases ProblemsDocument30 pagesAccounts Receivable, Accounts Payable, Sales and Purchases ProblemsJem ValmonteNo ratings yet

- Intercompany Sale of Merchandise - AdditionalDocument4 pagesIntercompany Sale of Merchandise - AdditionalJaimell LimNo ratings yet

- Cristobal Store Problem 8-4 Accounts Adjusted Trial BalanceDocument3 pagesCristobal Store Problem 8-4 Accounts Adjusted Trial BalanceFakerPlaymakerNo ratings yet

- Departmental accounts solutionsDocument10 pagesDepartmental accounts solutionsMINTU SARAFNo ratings yet

- ClassProblemsChapter5 SolutionDocument6 pagesClassProblemsChapter5 SolutionA373728272No ratings yet

- CAD Schedule Consolidated Income ReportDocument5 pagesCAD Schedule Consolidated Income Reportm habiburrahman55No ratings yet

- Adriel Company toy car costing and profit analysisDocument4 pagesAdriel Company toy car costing and profit analysisLerma MarianoNo ratings yet

- Bahas Latihan TM11-1 2Document7 pagesBahas Latihan TM11-1 2Shely NaNo ratings yet

- Assignment On LCNRV and GP MethodDocument6 pagesAssignment On LCNRV and GP MethodAdam CuencaNo ratings yet

- CVP, AVC, BudgetingDocument8 pagesCVP, AVC, BudgetingLeoreyn Faye MedinaNo ratings yet

- Intercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Document31 pagesIntercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Abegail LibreaNo ratings yet

- Weighted Average Costing and Quantity SchedulesDocument5 pagesWeighted Average Costing and Quantity SchedulesEric Kevin LecarosNo ratings yet

- Advanced Accounting 3Document1 pageAdvanced Accounting 3Tax TrainingNo ratings yet

- Cost of Goods Available For SaleDocument4 pagesCost of Goods Available For SaleColeen RamosNo ratings yet

- Fabm OutputsDocument3 pagesFabm OutputsElaine Joyce GarciaNo ratings yet

- D10 Spring2010Document7 pagesD10 Spring2010meelas123No ratings yet

- DAIBB MA Math Solutions 290315Document11 pagesDAIBB MA Math Solutions 290315joyNo ratings yet

- Bahas Latihan TM11-1Document7 pagesBahas Latihan TM11-1Julia Pratiwi ParhusipNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- MZM Grocery Store Financial StatementsDocument9 pagesMZM Grocery Store Financial StatementsRica Ann RoxasNo ratings yet

- FAR 1 Chapter - 10Document12 pagesFAR 1 Chapter - 10Klaus DoNo ratings yet

- FAR 1 Chapter - 10Document12 pagesFAR 1 Chapter - 10Klaus DoNo ratings yet

- Discontinued Operations, Segment and Interim Reporting, Biological AssetsDocument5 pagesDiscontinued Operations, Segment and Interim Reporting, Biological AssetsElaine Joyce GarciaNo ratings yet

- Practical Auditing by Empleo 2022 Chapter 4 Receivables Related RevenuesDocument55 pagesPractical Auditing by Empleo 2022 Chapter 4 Receivables Related RevenuesDarence IndayaNo ratings yet

- Inventory, Purchases, Sales and Expenses ReportDocument10 pagesInventory, Purchases, Sales and Expenses ReportnovyNo ratings yet

- Kunci Quiz 3 Bond BaruDocument1 pageKunci Quiz 3 Bond BaruKoko D'DemonsongNo ratings yet

- Model Paper AnswersDocument12 pagesModel Paper AnswersShenali NupehewaNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- Audit Problem Inventories AnswerDocument6 pagesAudit Problem Inventories AnswerJames PaulNo ratings yet

- AC - IntAcctg1 Quiz 2 Solution GuideDocument6 pagesAC - IntAcctg1 Quiz 2 Solution Guidejohn hellNo ratings yet

- Tutorial4 - Sol - New UpdateDocument13 pagesTutorial4 - Sol - New UpdateHa NguyenNo ratings yet

- Hoba Icare Answer KeysDocument15 pagesHoba Icare Answer KeysMark Gelo WinchesterNo ratings yet

- Absorption vs Marginal Costing: Worked ExamplesDocument5 pagesAbsorption vs Marginal Costing: Worked ExamplesSUHRIT BISWASNo ratings yet

- Making Capital Investment DecisionsDocument48 pagesMaking Capital Investment DecisionsJerico ClarosNo ratings yet

- Tut Mene AccDocument7 pagesTut Mene Accnatasya angelNo ratings yet

- Matching problems and liquidation computationsDocument8 pagesMatching problems and liquidation computationsSherryl DumagpiNo ratings yet

- Pembahasan Kuiz Indirect HoldingsDocument3 pagesPembahasan Kuiz Indirect HoldingsAdara KiranaNo ratings yet

- Jawaban Soal Quiz No 2 Dan 3Document4 pagesJawaban Soal Quiz No 2 Dan 3Anthony indrahalimNo ratings yet

- Modul 7Document9 pagesModul 7Sebastian T.MNo ratings yet

- Accounting 3 4 Module 3aDocument2 pagesAccounting 3 4 Module 3aMnriMinaNo ratings yet

- ME CIA3 BepDocument4 pagesME CIA3 BepSanjana A 1910217No ratings yet

- CHUA - Exercise 3 - BudgetingDocument1 pageCHUA - Exercise 3 - BudgetingClaudeen Jade Antoinette ChuaNo ratings yet

- Z Company Income Statement ComparisonDocument11 pagesZ Company Income Statement ComparisonMohamed RefaayNo ratings yet

- Chapter 7 Up StreamDocument14 pagesChapter 7 Up StreamAditya Agung SatrioNo ratings yet

- RM Music Worksheet For The Ended Period July, 31 2016Document25 pagesRM Music Worksheet For The Ended Period July, 31 2016AmandaNo ratings yet

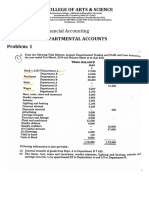

- PSG Financial Accounting Departmental ProblemsDocument7 pagesPSG Financial Accounting Departmental Problemsanand dpiNo ratings yet

- CF Assignment 1 Group 9Document51 pagesCF Assignment 1 Group 9rishabh tyagiNo ratings yet

- 10-column-worksheet-form (1)Document1 page10-column-worksheet-form (1)catherinemariposa001No ratings yet

- Lesson 2 - VAT May 05, 2022Document8 pagesLesson 2 - VAT May 05, 2022Kloie SanoriaNo ratings yet

- Problem 2 Process Costing UlitDocument4 pagesProblem 2 Process Costing UlitKloie SanoriaNo ratings yet

- MAS Integration Exercise 1 Cost BehaviorDocument4 pagesMAS Integration Exercise 1 Cost BehaviorNycole joi CondeNo ratings yet

- VAT HomeworkDocument3 pagesVAT HomeworkKloie SanoriaNo ratings yet

- Problem 1 Process CostingDocument1 pageProblem 1 Process CostingKloie SanoriaNo ratings yet

- Audit of Plant, Property, and EquipmentDocument36 pagesAudit of Plant, Property, and EquipmentKloie SanoriaNo ratings yet

- (ACC124) Investment QuizDocument6 pages(ACC124) Investment QuizKloie SanoriaNo ratings yet

- X'Chapter I SECTION 1: Form of Negotiable InstrumentsDocument13 pagesX'Chapter I SECTION 1: Form of Negotiable InstrumentsKloie SanoriaNo ratings yet

- GROUPED - Mean Median ModeDocument85 pagesGROUPED - Mean Median ModeKloie SanoriaNo ratings yet

- Operational Auditing Role ExpansionDocument5 pagesOperational Auditing Role ExpansionKloie SanoriaNo ratings yet

- BSA Students Maintaining CoVid-19 Preventive MeasuresDocument68 pagesBSA Students Maintaining CoVid-19 Preventive MeasuresKloie SanoriaNo ratings yet

- Auditppedocxdocx PDF FreeDocument121 pagesAuditppedocxdocx PDF FreeNicolas ErnestoNo ratings yet

- Terms Used in STATISTICS 32720Document20 pagesTerms Used in STATISTICS 32720Kloie SanoriaNo ratings yet

- Measures of Variability in DataDocument15 pagesMeasures of Variability in DataKloie SanoriaNo ratings yet

- Measures of Central Tendency SAwSDocument17 pagesMeasures of Central Tendency SAwSLeby FastidioNo ratings yet

- Measures of Central Tendency SAwSDocument17 pagesMeasures of Central Tendency SAwSLeby FastidioNo ratings yet

- Bitcoin Investment Options - Indian Family OfficesDocument5 pagesBitcoin Investment Options - Indian Family OfficesPranav UdaniNo ratings yet

- Comparing Projects with Unequal Lives Using Replacement Chain Method and Equivalent Annual AnnuityDocument3 pagesComparing Projects with Unequal Lives Using Replacement Chain Method and Equivalent Annual AnnuitydzazeenNo ratings yet

- Nedbank Case StudyDocument14 pagesNedbank Case Studyambuj joshiNo ratings yet

- Unit Test 5: Answer All Thirty Questions. There Is One Mark Per Question. 1 Who Receives What? Match A-E To 1-5Document6 pagesUnit Test 5: Answer All Thirty Questions. There Is One Mark Per Question. 1 Who Receives What? Match A-E To 1-5gronigan100% (1)

- Sa Puregold, Always Panalo!: N R D C I NDocument7 pagesSa Puregold, Always Panalo!: N R D C I NTumamudtamud, JenaNo ratings yet

- FIN301 Final QuestionDocument5 pagesFIN301 Final QuestionJunaidNo ratings yet

- IC 33 Question PaperDocument12 pagesIC 33 Question PaperSushil MehraNo ratings yet

- Reinsurance Industry Results 15Document14 pagesReinsurance Industry Results 15Philip SandaNo ratings yet

- Unit 6Document9 pagesUnit 6sheetal gudseNo ratings yet

- Saving and Investment Factors Literature Review: Chapter-IiDocument44 pagesSaving and Investment Factors Literature Review: Chapter-IiVienna Corrine Q. AbucejoNo ratings yet

- Xeerka Shirkada Land ServiceDocument20 pagesXeerka Shirkada Land ServiceHassan Ali50% (2)

- Case Study of CresentDocument3 pagesCase Study of Cresentgagan15095895No ratings yet

- Home Loan Lap Disbursement ChecklistDocument1 pageHome Loan Lap Disbursement ChecklistJaved QasimNo ratings yet

- Flash Memory Inc Student Spreadsheet SupplementDocument5 pagesFlash Memory Inc Student Spreadsheet Supplementjamn1979No ratings yet

- Balanced Scorecard: Company: BETLAP WANIA Date: March 27, 2018Document2 pagesBalanced Scorecard: Company: BETLAP WANIA Date: March 27, 2018Jesper Marie TuraoNo ratings yet

- Business Startup Costs and FundingDocument9 pagesBusiness Startup Costs and Fundingنور روسلنNo ratings yet

- Problem SetDocument105 pagesProblem SetYodaking Matt100% (1)

- Demat Services Project ReportDocument35 pagesDemat Services Project Reportjyoti raghuvanshi100% (2)

- The Virgin Group: An Innovative Corporate StructureDocument25 pagesThe Virgin Group: An Innovative Corporate Structurerohanag25% (4)

- NSDL Payment Bank by YunikShopDocument4 pagesNSDL Payment Bank by YunikShoprahul dev varunNo ratings yet

- CA Casualty Educational ObjectivesDocument40 pagesCA Casualty Educational ObjectiveshasupkNo ratings yet

- Akl Resume CH.5Document3 pagesAkl Resume CH.5cindy vica azizahNo ratings yet

- Deed of PartnershipDocument4 pagesDeed of Partnershipsince1978nsNo ratings yet

- Case 19-6 Classification of Cryptocurrency Holdings: All Rights ReservedDocument2 pagesCase 19-6 Classification of Cryptocurrency Holdings: All Rights ReservedbalonyNo ratings yet

- COA-SaranganiPov2019 Audit ReportDocument186 pagesCOA-SaranganiPov2019 Audit ReportRascille LaranasNo ratings yet

- Balance Sheet Accounts Income Statement Accounts: APPENDIX A: Company Chart of AccountsDocument27 pagesBalance Sheet Accounts Income Statement Accounts: APPENDIX A: Company Chart of Accountsrisc1No ratings yet

- NORKA SPECIAL SCHEME FOR RETURNING EMIGRANTSDocument1 pageNORKA SPECIAL SCHEME FOR RETURNING EMIGRANTSGreatway ServicesNo ratings yet

- Trial Balance Ud Mudah HasilDocument1 pageTrial Balance Ud Mudah HasilSani SausanNo ratings yet

- Ssgrbcc Official: Banking, Finance and Static G.K NotesDocument83 pagesSsgrbcc Official: Banking, Finance and Static G.K NotesSiva PrasadNo ratings yet