You might also like

- ProvisionalInterestCertificate 856658 201902052347Document1 pageProvisionalInterestCertificate 856658 201902052347prateek mishra0% (1)

- ProvisionalInterestCertificate IL10026977 202205111824Document1 pageProvisionalInterestCertificate IL10026977 202205111824Diksha PrasadNo ratings yet

- Interest Certificate: Dharmendra Kumar SamtaniDocument1 pageInterest Certificate: Dharmendra Kumar SamtanideepNo ratings yet

- 4330467076170342677Document1 page4330467076170342677vamsi patnalaNo ratings yet

- MR Parmar Krishnarajsinh 554/1, Satyam Society, Sector-22, Gandhinagar, GANDHINAGAR-382021Document1 pageMR Parmar Krishnarajsinh 554/1, Satyam Society, Sector-22, Gandhinagar, GANDHINAGAR-382021parmarkrishnarajsinh100% (1)

- HHLHYD00208643 ProvisionalDocument1 pageHHLHYD00208643 ProvisionalPranab PaulNo ratings yet

- HHLHYE00424239 Provisional (2019-2020)Document1 pageHHLHYE00424239 Provisional (2019-2020)sanjeevNo ratings yet

- Zxyzvyyyyy 1223Document1 pageZxyzvyyyyy 1223VIGNESHNo ratings yet

- Provisional Letter CommDocument1 pageProvisional Letter CommShekharNo ratings yet

- PHR051401998301-Final IT CertificateDocument2 pagesPHR051401998301-Final IT Certificateamjad.shaik0128No ratings yet

- Interest Certificate - Manoj ThakurDocument1 pageInterest Certificate - Manoj ThakurDiksha PrasadNo ratings yet

- Home loan deduction detailsDocument1 pageHome loan deduction detailsDonally PatelNo ratings yet

- HDFC Home Loan Deduction StatementDocument1 pageHDFC Home Loan Deduction StatementArunNo ratings yet

- Lac It Cert 832987 PDFDocument1 pageLac It Cert 832987 PDFManoj Kumar0% (1)

- Interest Certificate - 36185174 - 1054440Document1 pageInterest Certificate - 36185174 - 1054440ganeshbanger73No ratings yet

- IT Certificate 622197149Document1 pageIT Certificate 622197149karimshiekNo ratings yet

- Provisional Certificate 2018-2019Document1 pageProvisional Certificate 2018-2019RohanNo ratings yet

- Loan Details SampleDocument1 pageLoan Details Samplekarthik dNo ratings yet

- Web It CertDocument1 pageWeb It Certprashasya duttNo ratings yet

- To Whomsoever It May Concern Provisional Interest CertificateDocument1 pageTo Whomsoever It May Concern Provisional Interest CertificateSHOBHRAJ MEENA0% (1)

- Web It CertDocument1 pageWeb It CertGuna SeelanNo ratings yet

- Provisional Interest Certificate - 56465233 - 221527539Document1 pageProvisional Interest Certificate - 56465233 - 221527539dinesh makwanaNo ratings yet

- Residential home loan EMI and tax deduction detailsDocument1 pageResidential home loan EMI and tax deduction detailsXen Operation DPHNo ratings yet

- Home LoanDocument2 pagesHome LoanRoshan LewisNo ratings yet

- Insurance Statement - Narender RawatDocument1 pageInsurance Statement - Narender RawatNarender Singh RawatNo ratings yet

- Provisional Fy 20-21Document1 pageProvisional Fy 20-21Kedar YadavNo ratings yet

- Interest Certificate: To Whomsoever It May ConcernDocument1 pageInterest Certificate: To Whomsoever It May ConcernfakeNo ratings yet

- ITcertificateDocument1 pageITcertificateV N CharyNo ratings yet

- Variable Rate Home Loan Interest DeductionDocument1 pageVariable Rate Home Loan Interest DeductionSelvakumaran GNo ratings yet

- Home Loan AllDocument3 pagesHome Loan Allsumanpal78No ratings yet

- 9473667098713233264Document1 page9473667098713233264Parth NayakNo ratings yet

- Education Loan PDFDocument1 pageEducation Loan PDFmac martinNo ratings yet

- Hhlkal00211208 17-18Document1 pageHhlkal00211208 17-18RohanNo ratings yet

- 80c-House Princ Phrxxxxxx8636Document1 page80c-House Princ Phrxxxxxx8636Sama UmateNo ratings yet

- MR Shaik Mansoor Hussain H NO 87 1101 P 363 A, Ganesh Nagar, 4Th Class Colony, KURNOOL, KURNOOL-518002Document1 pageMR Shaik Mansoor Hussain H NO 87 1101 P 363 A, Ganesh Nagar, 4Th Class Colony, KURNOOL, KURNOOL-518002Shaik MansoorhussainNo ratings yet

- Housing Loan (0363675100002233) Provisional Certificate-2017-18 PDFDocument1 pageHousing Loan (0363675100002233) Provisional Certificate-2017-18 PDFsikha singh63% (8)

- 369982633-Housing-Loan-0363675100002233-Provisional-Certificate-2017-18-pdfDocument1 page369982633-Housing-Loan-0363675100002233-Provisional-Certificate-2017-18-pdfNeha JainNo ratings yet

- AXIS BANK HOME LOAN INTEREST CERTIFICATE For FY 2019-20Document1 pageAXIS BANK HOME LOAN INTEREST CERTIFICATE For FY 2019-20Harish Ghorpade67% (6)

- MR Yogesh #4, Shiva Enclave, Zirakpur, Vill Bhabat, S.A.S NAGAR-140603Document1 pageMR Yogesh #4, Shiva Enclave, Zirakpur, Vill Bhabat, S.A.S NAGAR-140603yogeshNo ratings yet

- Web It CertDocument1 pageWeb It CertRana BiswasNo ratings yet

- DocumentDocument2 pagesDocumentkitchencloud2022No ratings yet

- ELR008205284502-Final IT CertificateDocument1 pageELR008205284502-Final IT CertificateMarzook Suhail100% (1)

- Provisional Certificate For The Financial Year 2016-2017: To Whomsoever It May ConcernDocument1 pageProvisional Certificate For The Financial Year 2016-2017: To Whomsoever It May Concernvarsha sekharNo ratings yet

- Input Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtDocument9 pagesInput Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtdeepakasopaNo ratings yet

- View CertificateDocument1 pageView CertificateGopal PenjarlaNo ratings yet

- REPLYDocument94 pagesREPLYabhiGT40100% (1)

- Car LoanDocument1 pageCar Loansatya.undapalliNo ratings yet

- Premium Paid Certificate Sandip PatilDocument2 pagesPremium Paid Certificate Sandip Patilbebo03450% (2)

- Housing Loan (0363675100002233) Final Certificate - 2016-17 PDFDocument1 pageHousing Loan (0363675100002233) Final Certificate - 2016-17 PDFsikha singh50% (2)

- JudgementbyjdateDocument27 pagesJudgementbyjdateBasanta Kumar SahooNo ratings yet

- 7993761947155757203Document1 page7993761947155757203Sourav MohapatraNo ratings yet

- Home Loan - Certificate - 2022-23Document1 pageHome Loan - Certificate - 2022-23cont2chandu100% (1)

- Education Loan Interest CertDocument1 pageEducation Loan Interest Certshekismail mvjNo ratings yet

- Car Loan Nagendra StatementDocument1 pageCar Loan Nagendra Statementnavengg521No ratings yet

- DocumentDocument1 pageDocumentkalyan0% (1)

- Provisional Certificate H404HHL0871998Document1 pageProvisional Certificate H404HHL0871998Prakash BattalaNo ratings yet

- Reply Letter - Lawyer NoticeDocument3 pagesReply Letter - Lawyer Noticemeghan googlyNo ratings yet

- HL IT - Certificate - 621058739 FY 23-24 SampleDocument1 pageHL IT - Certificate - 621058739 FY 23-24 SampleGouravpurvi100% (1)

- CHALLANDocument1 pageCHALLANtdsbolluNo ratings yet

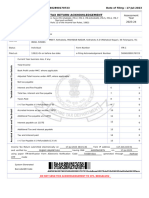

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:500402890170723 Date of Filing: 17-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:500402890170723 Date of Filing: 17-Jul-2023tdsbolluNo ratings yet

- JR E-2 Girls NWT-04 10.07.23Document3 pagesJR E-2 Girls NWT-04 10.07.23tdsbolluNo ratings yet

- Proceedings of The Mandal Educational Officer, MP KothakotaDocument1 pageProceedings of The Mandal Educational Officer, MP KothakotatdsbolluNo ratings yet

- El's Proccedings of The Gazetted Head MasterDocument1 pageEl's Proccedings of The Gazetted Head MastertdsbolluNo ratings yet

- 27a Hydz03256b 24Q Q3 2023Document1 page27a Hydz03256b 24Q Q3 2023tdsbolluNo ratings yet

- Proceedings of The Mandal Educational Officer, MP KothakotaDocument1 pageProceedings of The Mandal Educational Officer, MP KothakotatdsbolluNo ratings yet

- 27a - Hydg04633g - 24Q - Q3 - 202324 GJC PBRDocument1 page27a - Hydg04633g - 24Q - Q3 - 202324 GJC PBRtdsbolluNo ratings yet