You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- New Road & Transport Planning of Entire India: Under the Theme How to Revive India?From EverandNew Road & Transport Planning of Entire India: Under the Theme How to Revive India?No ratings yet

- Banks in IndiaDocument7 pagesBanks in IndiahappytiwariNo ratings yet

- Regional Rural Banks in IndiaDocument6 pagesRegional Rural Banks in IndiaSadhana MishraNo ratings yet

- Structure of Commercial Banking in India: Submmited By:-Samridhi Goad Roll Number - 4217Document56 pagesStructure of Commercial Banking in India: Submmited By:-Samridhi Goad Roll Number - 4217Jyoti GoadNo ratings yet

- Structure of Commercial Banking in IndiaDocument56 pagesStructure of Commercial Banking in IndiaSamridhi Goad86% (7)

- Abhilasha DubeyDocument8 pagesAbhilasha Dubeyanon_292119648No ratings yet

- India Banking OverviewDocument14 pagesIndia Banking OverviewNitin NagpureNo ratings yet

- 23.aug Ijmte - CWDocument6 pages23.aug Ijmte - CWPrince KatyalNo ratings yet

- Types of BankingDocument8 pagesTypes of Banking090 Riddhi MonparaNo ratings yet

- Banking System in IndiaDocument33 pagesBanking System in Indiadevinder07No ratings yet

- MANAGEMENT OF RURAL FINANCIAL SERVICESDocument25 pagesMANAGEMENT OF RURAL FINANCIAL SERVICESkinjpraj50% (2)

- A Project Report ON Rural Banking in India: Submitted To: M/S. Khushbu ShahDocument25 pagesA Project Report ON Rural Banking in India: Submitted To: M/S. Khushbu ShahvishaliNo ratings yet

- Management of Financial Services A ProjeDocument25 pagesManagement of Financial Services A ProjeSagar A. BarotNo ratings yet

- Regional Rural BankDocument26 pagesRegional Rural BankVijayeta Nerurkar100% (1)

- Public Sector BanksDocument8 pagesPublic Sector BanksPradeep KannanNo ratings yet

- Chairpersons: Karam Chand ThaparDocument3 pagesChairpersons: Karam Chand ThaparRachit KushwahaNo ratings yet

- Patel Rakesh H.: Banking in IndiaDocument76 pagesPatel Rakesh H.: Banking in IndiaKamlesh MevadaNo ratings yet

- Public sector banks, co-operative banks, private banks and financial institutions in IndiaDocument8 pagesPublic sector banks, co-operative banks, private banks and financial institutions in IndiaSrisusindhran KalaichelvanNo ratings yet

- Banking Management: Presented by C. KavyaDocument27 pagesBanking Management: Presented by C. KavyaKaviya KaviNo ratings yet

- IBPS RRB CWE III Quick Reference Guide 2014Document58 pagesIBPS RRB CWE III Quick Reference Guide 2014ilakkikarthiNo ratings yet

- Types of Co-operative and Public Sector Banks in IndiaDocument4 pagesTypes of Co-operative and Public Sector Banks in IndiaIMPEL Learning SolutionsNo ratings yet

- Banks in IndiaDocument15 pagesBanks in IndiaGaurav SharmaNo ratings yet

- Investment Banking 9th SemDocument14 pagesInvestment Banking 9th SemShikshaNo ratings yet

- About IBPS: Description DetailsDocument3 pagesAbout IBPS: Description DetailssandeepNo ratings yet

- Regional RuralDocument3 pagesRegional RuralheartlyhiteshNo ratings yet

- Regional RuralDocument3 pagesRegional RuralheartlyhiteshNo ratings yet

- Financial Awareness & Banking AwarenessDocument24 pagesFinancial Awareness & Banking Awarenessfgrowth646No ratings yet

- Rural BankingDocument22 pagesRural BankingGungun KumariNo ratings yet

- Small Finance BankDocument9 pagesSmall Finance BankRohit SinghNo ratings yet

- Types of Banks in IndiaDocument2 pagesTypes of Banks in IndiaANKIT SINGHNo ratings yet

- Presentation Report On Loans and AdvancesDocument20 pagesPresentation Report On Loans and AdvancesHawk AujlaNo ratings yet

- Structure of Commercial Banking in IndiaDocument43 pagesStructure of Commercial Banking in IndiaViral PathakNo ratings yet

- Growth and Development of Regional Rural Banks: Case Study of Two Major RrbsDocument16 pagesGrowth and Development of Regional Rural Banks: Case Study of Two Major RrbsProf S P GargNo ratings yet

- Scheduled Commercial BanksDocument9 pagesScheduled Commercial BanksMinakshi JalanNo ratings yet

- Customer Satisfaction OF Icici Bank: A Summer Training Report ONDocument88 pagesCustomer Satisfaction OF Icici Bank: A Summer Training Report ONGeetanshu SinghNo ratings yet

- Bank Name Chairmen Head Quarter Establishe D By: State Bank and AssociatesDocument4 pagesBank Name Chairmen Head Quarter Establishe D By: State Bank and AssociatesAvadhanam NagarajuNo ratings yet

- Live Banks in NACH 25022014Document24 pagesLive Banks in NACH 25022014Avneesh KumarNo ratings yet

- Wa0001Document94 pagesWa0001Akash Ðaya SinhaNo ratings yet

- Indian Banking Mission and VisionDocument10 pagesIndian Banking Mission and VisionkarthickkrishnanmbaNo ratings yet

- Insurance & Banking ProjectDocument15 pagesInsurance & Banking Projectfundoo16No ratings yet

- Banking Management: Presented by C. KavyaDocument28 pagesBanking Management: Presented by C. KavyaKaviya KaviNo ratings yet

- History of Obc BankDocument4 pagesHistory of Obc BankRachit KushwahaNo ratings yet

- Regional Rural BankDocument4 pagesRegional Rural BanksrikanthuasNo ratings yet

- State Bank of IndiaDocument20 pagesState Bank of IndiaLatika BhallaNo ratings yet

- State Bank of IndiaDocument20 pagesState Bank of IndiaLatika BhallaNo ratings yet

- Unit - 1Document93 pagesUnit - 1Suji MbaNo ratings yet

- Indian Banking StructureDocument24 pagesIndian Banking StructureRENUKA CHAUHANNo ratings yet

- Hyderabad, Telangana India State Bank of India HyderabadDocument4 pagesHyderabad, Telangana India State Bank of India HyderabadERAKACHEDU HARI PRASADNo ratings yet

- RRB 180228071053Document10 pagesRRB 180228071053Kool KingNo ratings yet

- Banking Structure in IndiaDocument5 pagesBanking Structure in IndiaCharu Saxena16No ratings yet

- By Sandeep Keshri Alumini IPEXDocument33 pagesBy Sandeep Keshri Alumini IPEXgladalokNo ratings yet

- Mega Merger of SBI with Five SubsidiariesDocument4 pagesMega Merger of SBI with Five Subsidiarieskartik naikNo ratings yet

- About Privet Banking Sector in IndiaDocument11 pagesAbout Privet Banking Sector in IndiaRakesh MalusareNo ratings yet

- Indian Banking System StructureDocument44 pagesIndian Banking System StructureUrooj Alam FarooquiNo ratings yet

- Rural Banking in India: An Overview of Key Institutions and Their RolesDocument16 pagesRural Banking in India: An Overview of Key Institutions and Their Rolespravin_kotecha7383100% (1)

- BANKING AND FINANCE IN INDIA Post-IndepeDocument22 pagesBANKING AND FINANCE IN INDIA Post-IndepePravin ThoratNo ratings yet

- Banking DetailsDocument9 pagesBanking DetailsModi HaniNo ratings yet

- Micro Credit: SHG Movement - A MissionDocument4 pagesMicro Credit: SHG Movement - A Missiongogetter_moiNo ratings yet

- Bankers, Hug Your Customers: A Guide to Every Banker to Delight Customers, Employees, and ColleaguesFrom EverandBankers, Hug Your Customers: A Guide to Every Banker to Delight Customers, Employees, and ColleaguesNo ratings yet

- Binlist PDFDocument26 pagesBinlist PDFStingah Velli0% (1)

- J.P Morgan ChaseDocument22 pagesJ.P Morgan ChaseshagunyashiNo ratings yet

- Adhaar Aadhaar Adhar Aadhar Update Centre CenterDocument2 pagesAdhaar Aadhaar Adhar Aadhar Update Centre CenterMatt RileyNo ratings yet

- GrupoDocument3 pagesGrupo28kpjrrx4nNo ratings yet

- HistoryDocument3 pagesHistoryPia Angela ElemosNo ratings yet

- List of Top Financial Institutions in PuneDocument15 pagesList of Top Financial Institutions in PuneKalpana JohnNo ratings yet

- FAIZDocument83 pagesFAIZMohammad RizwanNo ratings yet

- British Private Equity Is Losing Out To American Firms Such As KKR's Henry Kravis and Blackstone's Stephen SchwarzmanDocument9 pagesBritish Private Equity Is Losing Out To American Firms Such As KKR's Henry Kravis and Blackstone's Stephen SchwarzmanAlex HoltNo ratings yet

- HARSHUDocument22 pagesHARSHUvini2710No ratings yet

- ETF Quarterly 4Q09Document4 pagesETF Quarterly 4Q09Vladimir KreindelNo ratings yet

- History: State Bank of India (SBI) Is A MultinationalDocument7 pagesHistory: State Bank of India (SBI) Is A MultinationalsrikanthuasNo ratings yet

- BR Table For BNM Website 14062019Document3 pagesBR Table For BNM Website 14062019Sundararaju NarayanasamyNo ratings yet

- Histori TransaksiDocument3 pagesHistori TransaksiAde Wardhana ChicharitoNo ratings yet

- Corporate Bond Listed On The Exchange - Public IssueDocument174 pagesCorporate Bond Listed On The Exchange - Public IssuePrachi MaheshwariNo ratings yet

- Bloomberg Markets Magazine The Worlds 100 Richest Hedge Funds February 2011Document8 pagesBloomberg Markets Magazine The Worlds 100 Richest Hedge Funds February 2011VALUEWALK LLCNo ratings yet

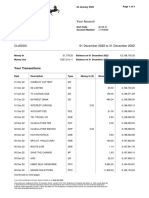

- Acct Statement XX9972 01082022Document35 pagesAcct Statement XX9972 01082022Ashik AshiNo ratings yet

- Advantages and disadvantages of mutual fundsDocument4 pagesAdvantages and disadvantages of mutual fundsbhaveshNo ratings yet

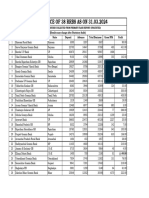

- ATCH to Cir. No. 89 - PERFORMANCE OF 39 RRBS AS ON 31.03.2024Document2 pagesATCH to Cir. No. 89 - PERFORMANCE OF 39 RRBS AS ON 31.03.2024pateldixit.dx3No ratings yet

- Statement 2022 12Document4 pagesStatement 2022 12wconceptouNo ratings yet

- Top Sri Lankan and Indian Banks ListDocument660 pagesTop Sri Lankan and Indian Banks ListShailendra YadavNo ratings yet

- Acct Statement - XX4811 - 11032024Document21 pagesAcct Statement - XX4811 - 11032024amolgorkhe612No ratings yet

- Indian Bank Contacts List with Designations and Contact DetailsDocument3 pagesIndian Bank Contacts List with Designations and Contact DetailsAmit Dwivedi100% (1)

- Manage savings with ease through online bankingDocument20 pagesManage savings with ease through online bankingSunny ProNo ratings yet

- Banks Enabled For Customer Payment Through RTGSDocument4,727 pagesBanks Enabled For Customer Payment Through RTGSSunny RajaNo ratings yet

- HLB Mohd IzzwandeeDocument13 pagesHLB Mohd IzzwandeeMohd IzzwandeeNo ratings yet

- Samsonite International S A SEHK 1910 新秀麗國際有限公司 Public Company ProfileDocument3 pagesSamsonite International S A SEHK 1910 新秀麗國際有限公司 Public Company ProfileSilviu TrebuianNo ratings yet

- Statement 1568002244543Document10 pagesStatement 1568002244543krishna aNo ratings yet

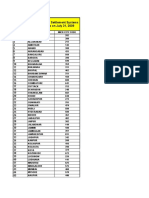

- Codes Banking MICR Codes RBI 15102010 67440Document1,455 pagesCodes Banking MICR Codes RBI 15102010 67440abhayarchivNo ratings yet

- Actuarial Companies in South AfricaDocument4 pagesActuarial Companies in South AfricaJonahJuniorNo ratings yet

- 1 4906830763644683526Document8 pages1 4906830763644683526sandra.hurta2vNo ratings yet