You might also like

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- REINSURANCEDocument3 pagesREINSURANCEKelly CardejonNo ratings yet

- Unit 3 InsuranceDocument29 pagesUnit 3 InsuranceNikita ShekhawatNo ratings yet

- Final Year Project For MCom in Manufacturing PencilDocument73 pagesFinal Year Project For MCom in Manufacturing PencilPadmaja MenonNo ratings yet

- Insurance OperationsDocument5 pagesInsurance OperationssimplyrochNo ratings yet

- Af 323 Topic No OneDocument8 pagesAf 323 Topic No Oneannampunga25No ratings yet

- 120 Financial Planning Handbook PDPDocument10 pages120 Financial Planning Handbook PDPMoh. Farid Adi PamujiNo ratings yet

- Accidental InsuranceDocument33 pagesAccidental InsuranceHarinarayan PrajapatiNo ratings yet

- FAIS AssignmentDocument17 pagesFAIS AssignmentSalman SaeedNo ratings yet

- Project Report ON: University of MumbaiDocument55 pagesProject Report ON: University of MumbaiNayak SandeshNo ratings yet

- Sariga.s - Insurance PresentationDocument13 pagesSariga.s - Insurance PresentationSasi KumarNo ratings yet

- Assign 1Document11 pagesAssign 1Rakshi BegumNo ratings yet

- Lecture 8 InsuranceDocument8 pagesLecture 8 InsuranceAnna BrasoveanNo ratings yet

- A Project Report ON: "Customer Satisfaction Survey OnDocument66 pagesA Project Report ON: "Customer Satisfaction Survey Onsshane kumarNo ratings yet

- Insurance Company AnalysisDocument13 pagesInsurance Company AnalysisAyon ImtiazNo ratings yet

- Go Policy (Insurance Broker) : Student's Name: Student's Id: Date: Word Count: 2000Document12 pagesGo Policy (Insurance Broker) : Student's Name: Student's Id: Date: Word Count: 2000Mayur SoNo ratings yet

- What Is An Insurer?: Topic 3. Types of Insurers and Marketing SystemsDocument14 pagesWhat Is An Insurer?: Topic 3. Types of Insurers and Marketing SystemsLNo ratings yet

- Capstone Report - Ensure - Io - Final DraftDocument13 pagesCapstone Report - Ensure - Io - Final DraftRamapriyaNo ratings yet

- Reflection Paper#1Document2 pagesReflection Paper#1nerieroseNo ratings yet

- Claim Management in Life InsuranceDocument55 pagesClaim Management in Life InsuranceSunil RawatNo ratings yet

- Ibis Unit 03Document28 pagesIbis Unit 03bhagyashripande321No ratings yet

- ProjectDocument52 pagesProjectPranali WahaneNo ratings yet

- Indian Insurance SectorDocument32 pagesIndian Insurance Sectorbanirumi100% (2)

- Max New York Life, Axis Bank Sign Bancassurance RelationshipDocument22 pagesMax New York Life, Axis Bank Sign Bancassurance RelationshipAnurag PateriaNo ratings yet

- Business Process DesignDocument2 pagesBusiness Process DesignLea Jane CadanoNo ratings yet

- ProjectDocument36 pagesProjectGayathri SelvarajNo ratings yet

- Concept of ClaimsDocument23 pagesConcept of ClaimsbapparoyNo ratings yet

- InsuranceDocument8 pagesInsuranceSriram VenkatakrishnanNo ratings yet

- Share ICICI PrudentialsDocument63 pagesShare ICICI PrudentialsMadhushreeNo ratings yet

- CHAPTER 1 IntroductionDocument6 pagesCHAPTER 1 IntroductionPrerana AroraNo ratings yet

- Bancassurance in Standard Chartered BankDocument65 pagesBancassurance in Standard Chartered BankShweta Yashwant ChalkeNo ratings yet

- Progressive Final PaperDocument16 pagesProgressive Final PaperJordyn WebreNo ratings yet

- CRM in InsuranceDocument55 pagesCRM in InsuranceNitin SinghNo ratings yet

- Full and FinallDocument23 pagesFull and FinallRaihan RakibNo ratings yet

- Reinsurance Basic GuideDocument80 pagesReinsurance Basic GuideAyaaz Fazulbhoy100% (3)

- InsuranceDocument7 pagesInsurancesarvesh.bhartiNo ratings yet

- BasicsDocument2 pagesBasicsAtul SinghNo ratings yet

- Executive SummaryDocument25 pagesExecutive SummaryRitika MahenNo ratings yet

- InsuranceDocument7 pagesInsuranceSamadNo ratings yet

- Recruitment of Advisors in IciciDocument77 pagesRecruitment of Advisors in Icicipadamheena123No ratings yet

- Present Scenario in The Insurance SectorDocument6 pagesPresent Scenario in The Insurance Sectorghagsona100% (1)

- Dbfi303 - Principles and Practices of InsuranceDocument10 pagesDbfi303 - Principles and Practices of Insurancevikash rajNo ratings yet

- Chapter II - UnderwritingDocument24 pagesChapter II - UnderwritingswatishouryaNo ratings yet

- Journal of Accountancy March 2013Document8 pagesJournal of Accountancy March 2013hhpdenverNo ratings yet

- Re InsuranceDocument5 pagesRe Insurancenetishrai88No ratings yet

- Whole Life InsuranceDocument16 pagesWhole Life Insuranceemilda_samuel211No ratings yet

- Customer Satisfaction Insurance Products of ICICI PrudentialDocument71 pagesCustomer Satisfaction Insurance Products of ICICI Prudentialkarthik_shabby15No ratings yet

- CH 6 Insurance Company Operations PDFDocument22 pagesCH 6 Insurance Company Operations PDFMonika RehmanNo ratings yet

- What Is The Meaning of The Term Reinsurance?Document3 pagesWhat Is The Meaning of The Term Reinsurance?Shipra Singh0% (1)

- Final ScriptDocument42 pagesFinal ScriptAkhilesh desaiNo ratings yet

- My ProjectDocument94 pagesMy ProjectSunil RawatNo ratings yet

- Consumer BehaviourDocument10 pagesConsumer BehaviourAishwarya GharmalkarNo ratings yet

- Consumer Awareness Regarding PNB MetlifeDocument51 pagesConsumer Awareness Regarding PNB MetlifeKirti Jindal100% (1)

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- Executive Summary: M.S.R.C.A.S.C BangaloreDocument72 pagesExecutive Summary: M.S.R.C.A.S.C BangaloreSubramanya Dg100% (2)

- Structured Settlements: A Guide For Prospective SellersFrom EverandStructured Settlements: A Guide For Prospective SellersNo ratings yet

- Principles of Insurance Law with Case StudiesFrom EverandPrinciples of Insurance Law with Case StudiesRating: 5 out of 5 stars5/5 (1)

- taxxDocument4 pagestaxxKelly CardejonNo ratings yet

- TRANSACTIONCYCLESDocument26 pagesTRANSACTIONCYCLESKelly CardejonNo ratings yet

- Output in EconDocument12 pagesOutput in EconKelly CardejonNo ratings yet

- CHAPTER 10Document5 pagesCHAPTER 10Kelly CardejonNo ratings yet

- TRANSACTIONCYCLESDocument26 pagesTRANSACTIONCYCLESKelly CardejonNo ratings yet

- Get Ready To Breakdown The BarrierDocument1 pageGet Ready To Breakdown The BarrierKelly CardejonNo ratings yet

- Output in EconDocument12 pagesOutput in EconKelly CardejonNo ratings yet

- UntitledDocument1 pageUntitledKelly CardejonNo ratings yet

- Chapter 1Document2 pagesChapter 1Kelly CardejonNo ratings yet

- Chaptr 7-12 Gov AccDocument7 pagesChaptr 7-12 Gov AccKelly CardejonNo ratings yet

- DateDocument1 pageDateKelly CardejonNo ratings yet

- KishaDocument1 pageKishaKelly CardejonNo ratings yet

- Specialized Industry ReviewerDocument5 pagesSpecialized Industry ReviewerKelly CardejonNo ratings yet

- Econ Dev ScriptDocument5 pagesEcon Dev ScriptKelly CardejonNo ratings yet

- TRANSACTIONCYCLESDocument26 pagesTRANSACTIONCYCLESKelly CardejonNo ratings yet

- Chapter 1Document20 pagesChapter 1Kelly CardejonNo ratings yet

- TEST BANK - LAW 1-DiazDocument14 pagesTEST BANK - LAW 1-DiazChristian Blanza Lleva100% (3)

- Ecosystems Are Communities of LiDocument1 pageEcosystems Are Communities of LiKelly CardejonNo ratings yet

- Week 5 Law On Other Business Transactions 1Document11 pagesWeek 5 Law On Other Business Transactions 1seventh accountNo ratings yet

- Reflection in StsDocument2 pagesReflection in StsKelly CardejonNo ratings yet

- Definition of TermsDocument9 pagesDefinition of TermsKelly CardejonNo ratings yet

- Chapter 4Document30 pagesChapter 4Kelly CardejonNo ratings yet

- Definition of TermsDocument9 pagesDefinition of TermsKelly CardejonNo ratings yet

- Reflection in StsDocument2 pagesReflection in StsKelly CardejonNo ratings yet

- Reviewer in STSDocument3 pagesReviewer in STSKelly CardejonNo ratings yet

- Are Resources Controlled by An Entity As A Result of Past EventsDocument3 pagesAre Resources Controlled by An Entity As A Result of Past EventsKelly CardejonNo ratings yet

- Refers To The Percentage Change in A NationDocument1 pageRefers To The Percentage Change in A NationKelly CardejonNo ratings yet

- RFBT QuestionDocument7 pagesRFBT QuestionKelly CardejonNo ratings yet

- EXER07Document1 pageEXER07Kelly CardejonNo ratings yet

- EXER08Document1 pageEXER08Kelly CardejonNo ratings yet

- Private Vacancy List For 6 State Level Mega Job FairDocument91 pagesPrivate Vacancy List For 6 State Level Mega Job FairAkshit Raj Babbar SherNo ratings yet

- FandI CT5 200509 ExampaperDocument8 pagesFandI CT5 200509 ExampaperEuston ChinharaNo ratings yet

- A Study of Mutual Fund Management at LIC, JabalpurDocument38 pagesA Study of Mutual Fund Management at LIC, JabalpurArsh TiwariNo ratings yet

- Privatisation in Insurance SectorDocument20 pagesPrivatisation in Insurance Sectormokalo100% (5)

- Traditional IC Mock ExamDocument37 pagesTraditional IC Mock ExamNald FigueroaNo ratings yet

- Aviva Case StudyDocument15 pagesAviva Case Studymtayya266No ratings yet

- Insurance Company ThesisDocument7 pagesInsurance Company Thesisdwt5trfn100% (2)

- BBA Insurance Management 2022Document4 pagesBBA Insurance Management 2022Ꮢ.Gᴀɴᴇsн ٭ʏт᭄No ratings yet

- Consumer Perception Towards LIC in Rewa CityDocument64 pagesConsumer Perception Towards LIC in Rewa CityAbhay JainNo ratings yet

- IRDA Latest Claim Settlement Ratio 2019 List Best Death Claim Settlement Ratio Life Insurance Companies PicDocument4 pagesIRDA Latest Claim Settlement Ratio 2019 List Best Death Claim Settlement Ratio Life Insurance Companies PicsantuNo ratings yet

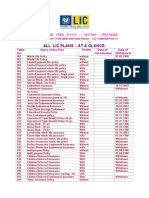

- All LIC PlansDocument4 pagesAll LIC Planslicvivek100% (1)

- Meghna Life Insurance Company: Insurance & Risk ManagementDocument28 pagesMeghna Life Insurance Company: Insurance & Risk Managementshahin317No ratings yet

- Suitability H Lead 231109061116067Document1 pageSuitability H Lead 231109061116067Surya 0710No ratings yet

- Example of Investment Analysis (School Project)Document43 pagesExample of Investment Analysis (School Project)Eminem89% (9)

- Training Deck - ABSLI Group Protection Solutions - SBDocument46 pagesTraining Deck - ABSLI Group Protection Solutions - SBavniakamdarNo ratings yet

- Lagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Document23 pagesLagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Lagnajit Ayaskant SahooNo ratings yet

- Pbi Module 4Document18 pagesPbi Module 4SUBHECHHA MOHAPATRANo ratings yet

- HDFC Life InsuranceDocument12 pagesHDFC Life Insurancesaswat mohantyNo ratings yet

- Renewal Premium Receipt: Har Pal Aapke Sath!!Document1 pageRenewal Premium Receipt: Har Pal Aapke Sath!!krishna krishNo ratings yet

- History of InsuranceDocument10 pagesHistory of InsuranceNikithaNo ratings yet

- Assignment - Financial Institutions and MarketsDocument6 pagesAssignment - Financial Institutions and MarketsShivam GoelNo ratings yet

- Irrevocable Life Insurance TrustDocument5 pagesIrrevocable Life Insurance TrustCeeNo ratings yet

- Insurance TrendsDocument19 pagesInsurance TrendsMaithili GuptaNo ratings yet

- Unit Byb - Fall BP, Mond PanelDocument96 pagesUnit Byb - Fall BP, Mond PanelRaymond OndesimoNo ratings yet

- Recruitment and Selection Process of Insurance CompaniesDocument85 pagesRecruitment and Selection Process of Insurance CompaniesAkhtar NawazNo ratings yet

- FIBA304 Introduction To Indian Financial SystemDocument14 pagesFIBA304 Introduction To Indian Financial SystemAk KalakotiNo ratings yet

- Term Life InsuranceDocument3 pagesTerm Life InsuranceAbhishek TendulkarNo ratings yet

- Sun Smarter Life ClassicDocument7 pagesSun Smarter Life Classicpaul jan sarachoNo ratings yet

- Sbaa 1401Document126 pagesSbaa 1401gayuammu1135No ratings yet

- Benefit IllustrationDocument5 pagesBenefit IllustrationAvnish MisraNo ratings yet