You might also like

- Time SeriesDocument63 pagesTime SeriesMegan SpitzerNo ratings yet

- ForecastingDocument56 pagesForecastingSumeet GaikwadNo ratings yet

- Instructions:: This Is An Online, Closed Book ExaminationDocument18 pagesInstructions:: This Is An Online, Closed Book ExaminationChandan SahNo ratings yet

- Caso 3 Homework7SolutionsDocument8 pagesCaso 3 Homework7SolutionsdeyviNo ratings yet

- Speciality Packaging Case StudyDocument20 pagesSpeciality Packaging Case StudyNitin ShankarNo ratings yet

- Jiahui He Bnad Lab8Document3 pagesJiahui He Bnad Lab8api-530849574No ratings yet

- BS SRR-3Document20 pagesBS SRR-3anveshvarma365No ratings yet

- Steel Frame FurnitureDocument17 pagesSteel Frame FurnitureDev AnandNo ratings yet

- Speciality Packaging Case Study PDFDocument20 pagesSpeciality Packaging Case Study PDFরাকিবইসলামNo ratings yet

- A Review of Basic Statistical Concepts: Answers To Odd Numbered Problems 1Document32 pagesA Review of Basic Statistical Concepts: Answers To Odd Numbered Problems 1Abbas RazaNo ratings yet

- Business Research: Corporate Governance in Financial Institutions of BangladeshDocument31 pagesBusiness Research: Corporate Governance in Financial Institutions of BangladeshShahriar HaqueNo ratings yet

- Ass No 4Document10 pagesAss No 4Muhammad Bilal MakhdoomNo ratings yet

- 02.3 DekomposisiDocument51 pages02.3 DekomposisiMuhamad Iqbal ArsaNo ratings yet

- QuizDocument1 pageQuizcathy.cathy9092No ratings yet

- Hanke9 Odd-Num Sol 03Document10 pagesHanke9 Odd-Num Sol 03NiladriDas100% (1)

- Class Exercise Before MIDDocument2 pagesClass Exercise Before MIDKhalil AhmedNo ratings yet

- XLSL bài 1-2 thị hiếuDocument4 pagesXLSL bài 1-2 thị hiếuPhương NguyễnNo ratings yet

- Module 4 (Data Management) - Math 101Document8 pagesModule 4 (Data Management) - Math 101Flory CabaseNo ratings yet

- Corporate AssingmentDocument10 pagesCorporate AssingmentHeitham OmarNo ratings yet

- Jro JDocument14 pagesJro JSandhyaNo ratings yet

- Lecture Note: Analysis of Financial Time SeriesDocument12 pagesLecture Note: Analysis of Financial Time Seriestestuser132546No ratings yet

- Yadunandan Sharma 500826933 MTH480 Due Date: April 15, 2021Document16 pagesYadunandan Sharma 500826933 MTH480 Due Date: April 15, 2021danNo ratings yet

- Simple Exponential Smoothing Model, Holt's Method and Holt-Winters MethodDocument10 pagesSimple Exponential Smoothing Model, Holt's Method and Holt-Winters MethoddesolatwormNo ratings yet

- isom3031 功課5 第4,5,6題 (update)Document13 pagesisom3031 功課5 第4,5,6題 (update)mak wangNo ratings yet

- Tutorial 9Document4 pagesTutorial 9HENG QUAN PANNo ratings yet

- Assignm 3Document3 pagesAssignm 3Luis Bellido C.No ratings yet

- Decomposition MethodsDocument42 pagesDecomposition MethodsAiman NawawiNo ratings yet

- Sales Forecast: October 9, 2020Document9 pagesSales Forecast: October 9, 2020salnasuNo ratings yet

- Tutorial 8Document4 pagesTutorial 8HENG QUAN PANNo ratings yet

- ForecastingDocument12 pagesForecastingMohoua SRNo ratings yet

- Apllied Econometrics-Cia 1 Nikitha M 1837044 3 Maeco Outputs and InterpretationDocument5 pagesApllied Econometrics-Cia 1 Nikitha M 1837044 3 Maeco Outputs and InterpretationnikiNo ratings yet

- STA302 Mid 2010FDocument9 pagesSTA302 Mid 2010FexamkillerNo ratings yet

- EC203 Tutorial 12 Time Series 16Document4 pagesEC203 Tutorial 12 Time Series 16R and R wweNo ratings yet

- BUS 5030 Milestone 2 WorksheetDocument12 pagesBUS 5030 Milestone 2 WorksheetDarlington OkonkwoNo ratings yet

- BUS - 5030 - Milestone - 2 - Worksheet (2) (1) (Repaired)Document12 pagesBUS - 5030 - Milestone - 2 - Worksheet (2) (1) (Repaired)Akasoro Abayomi A. OlabanjiNo ratings yet

- Mayli Econometria Exa FinalDocument13 pagesMayli Econometria Exa Finalzenia mayli coras de la cruzNo ratings yet

- RossettoDocument9 pagesRossettoDavide SilvestriNo ratings yet

- Book1 XlsxuuuDocument9 pagesBook1 XlsxuuuKenn SenadosNo ratings yet

- CH E Problem 3Document3 pagesCH E Problem 3Brayan AguilarNo ratings yet

- Solution To Campbell Lo Mackinlay PDFDocument71 pagesSolution To Campbell Lo Mackinlay PDFstaimouk0% (1)

- Seminar Final Word FileDocument8 pagesSeminar Final Word FileGhulam MustafaNo ratings yet

- Fa AssignmentDocument7 pagesFa AssignmentAnshuman GhoshNo ratings yet

- Inflasi ARIMA ModelDocument7 pagesInflasi ARIMA ModelAnto TomodachiRent SusiloNo ratings yet

- Carrying Cost: Inventory CostsDocument31 pagesCarrying Cost: Inventory CostsVivek Kumar GuptaNo ratings yet

- TheisMatchFt ComDocument21 pagesTheisMatchFt ComBarbu IonelNo ratings yet

- Hydrology Section8 - PeakFlowEstimationDocument19 pagesHydrology Section8 - PeakFlowEstimationKeith YangNo ratings yet

- BCGZrbIgSUOhma2yIGlDWw BF C2 W4a Seasonal Dummy VariablesDocument19 pagesBCGZrbIgSUOhma2yIGlDWw BF C2 W4a Seasonal Dummy VariablesManuel Alejandro Sanabria AmayaNo ratings yet

- Eviews 2Document15 pagesEviews 2Minza JahangirNo ratings yet

- Tutorial 3 SolutionDocument8 pagesTutorial 3 Solutionthanusha selvamanyNo ratings yet

- Welcome To "Rte-Book1Ddeltanorm - XLS" Calculator For 1D Subaerial Fluvial Fan-Delta With Channel of Constant WidthDocument23 pagesWelcome To "Rte-Book1Ddeltanorm - XLS" Calculator For 1D Subaerial Fluvial Fan-Delta With Channel of Constant WidthsteveNo ratings yet

- Data AnalysisDocument7 pagesData AnalysisMetin KayaNo ratings yet

- MGS3100 Chapter 13 Forecasting: Slides 13b: Time-Series Models Measuring Forecast ErrorDocument36 pagesMGS3100 Chapter 13 Forecasting: Slides 13b: Time-Series Models Measuring Forecast ErrorVinod Kumar Patel100% (2)

- Econometrics Hina NazDocument17 pagesEconometrics Hina NazHina Naz (F-Name :Khadim Hussain)No ratings yet

- Sistema Estructural Aporticada Tratandolo Como Irregular: Analisis Sismorrsistente Estatico & DinamicoDocument9 pagesSistema Estructural Aporticada Tratandolo Como Irregular: Analisis Sismorrsistente Estatico & DinamicoRicardo BermudezNo ratings yet

- Câu 7 8Document2 pagesCâu 7 8050610220285No ratings yet

- Assignment 5Document43 pagesAssignment 5Priyanka SindhwaniNo ratings yet

- Decision ScienceDocument3 pagesDecision ScienceRiyaNo ratings yet

- Tutorial Chapter 5Document2 pagesTutorial Chapter 5tashaNo ratings yet

- Macro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsFrom EverandMacro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsNo ratings yet

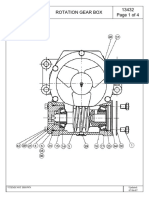

- Caja de Engranes para Pluma DunbarRotationGearBoxDocument4 pagesCaja de Engranes para Pluma DunbarRotationGearBoxMartin CalderonNo ratings yet

- Huawei FusionServer RH8100 V3 Data SheetDocument4 pagesHuawei FusionServer RH8100 V3 Data Sheetpramod BhattNo ratings yet

- PN423522 (1) Checkfire SC-NDocument50 pagesPN423522 (1) Checkfire SC-NJhojanCeleita50% (2)

- Assignment 4 Forward KinematicsDocument2 pagesAssignment 4 Forward KinematicsVaibhav KulkarniNo ratings yet

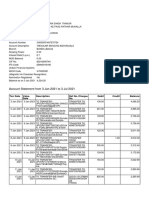

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- IGCSE COMMERCE Chapter 10.1Document5 pagesIGCSE COMMERCE Chapter 10.1Tahmid Raihan100% (1)

- 247248-The Histiry and Culture of The Indian People, The Vedic Age Vol I - DjvuDocument620 pages247248-The Histiry and Culture of The Indian People, The Vedic Age Vol I - DjvuDeja ImagenationNo ratings yet

- General Information NC Detector: SignatureDocument2 pagesGeneral Information NC Detector: SignatureEvelin FriasNo ratings yet

- ISO Accredited Training and Certification: VCAT I - Vibration AnalysisDocument3 pagesISO Accredited Training and Certification: VCAT I - Vibration AnalysisPraveenNo ratings yet

- Math 9 Q1 Summative Test 1Document4 pagesMath 9 Q1 Summative Test 1John Paul GaoatNo ratings yet

- Guide To Computer Forensics and Investigations 5th Edition Bill Test BankDocument11 pagesGuide To Computer Forensics and Investigations 5th Edition Bill Test Bankshelleyrandolphikeaxjqwcr100% (30)

- Experiences of Students On Online LearningDocument24 pagesExperiences of Students On Online LearningcharmaineNo ratings yet

- Juhi S. Khandekar: Email ID: Contact (M) : +91-7710007972Document1 pageJuhi S. Khandekar: Email ID: Contact (M) : +91-7710007972Reddi SyamsundarNo ratings yet

- Factors Affecting System Complexity: CouplingDocument4 pagesFactors Affecting System Complexity: CouplingJaskirat KaurNo ratings yet

- The Power of Social MediaDocument3 pagesThe Power of Social MediaTIGER CHEETANo ratings yet

- 2013-03 CBTA OverviewDocument19 pages2013-03 CBTA OverviewRahul Thandani100% (1)

- Indian Institute of Technology: Delhi Summary Sheet Consumable StoresDocument2 pagesIndian Institute of Technology: Delhi Summary Sheet Consumable StoresSumit SinghNo ratings yet

- Tech M Service LetterDocument1 pageTech M Service LetterRahul upadhyayNo ratings yet

- Reflection PaperDocument2 pagesReflection PaperKatrina DeveraNo ratings yet

- Service Manual: Wireless AmplifierDocument60 pagesService Manual: Wireless AmplifiergermieNo ratings yet

- Attachment - 1Document2 pagesAttachment - 1Abhilash KurianNo ratings yet

- VerilatorDocument224 pagesVerilatorGolnaz KorkianNo ratings yet

- Analytics-Based Investigation & Automated Response With AWS + Splunk Security SolutionsDocument37 pagesAnalytics-Based Investigation & Automated Response With AWS + Splunk Security SolutionsWesly SibagariangNo ratings yet

- Schengen Visa Application 2021-11-26Document5 pagesSchengen Visa Application 2021-11-26Edivaldo NehoneNo ratings yet

- Hydrodynamic Calculation Needle Valve Closing Flow Against The Direction of Movement of The PistonDocument23 pagesHydrodynamic Calculation Needle Valve Closing Flow Against The Direction of Movement of The Pistonmet-calcNo ratings yet

- DC BASIC GAS at Ravi Ranjan KumarDocument1 pageDC BASIC GAS at Ravi Ranjan KumarRAVI RANJAN KUMARNo ratings yet

- Emeter MDM White PaperDocument9 pagesEmeter MDM White PapernittecatNo ratings yet

- As 3850-2003 Tilt-Up Concrete ConstructionDocument8 pagesAs 3850-2003 Tilt-Up Concrete ConstructionSAI Global - APACNo ratings yet

- Netelastic VBNG Manager Installation GuideDocument11 pagesNetelastic VBNG Manager Installation GuideKhaing myal HtikeNo ratings yet

- Research Assistant - Smart Manufacturing Factory Designer 230795 at University of StrathclydeDocument1 pageResearch Assistant - Smart Manufacturing Factory Designer 230795 at University of StrathclydeOzden IsbilirNo ratings yet