You might also like

- QUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With SolutionsDocument9 pagesQUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With Solutionsfinn mertens100% (1)

- 123 PDFDocument3 pages123 PDFauliaNo ratings yet

- HBL Schedule of Bank ChargesDocument25 pagesHBL Schedule of Bank ChargesJohn Wick60% (5)

- Accounting For MfisDocument53 pagesAccounting For MfisChris Turnley100% (1)

- Bayer, George - Stock and Commodity Traders Hand-Book of Trend DeterminationDocument49 pagesBayer, George - Stock and Commodity Traders Hand-Book of Trend Determinationriri200410955288% (17)

- Monday To Thursday Exit 3 PMDocument2 pagesMonday To Thursday Exit 3 PMधीरज चव्हाणNo ratings yet

- Financial Accounting Project Covers Key ConceptsDocument6 pagesFinancial Accounting Project Covers Key ConceptsNosipho MsimangoNo ratings yet

- 2017report GambiaDocument378 pages2017report GambiaAlain PalaciosNo ratings yet

- Bank loan write-off policiesDocument4 pagesBank loan write-off policiescliffNo ratings yet

- Chapter 1 Current LiabilitiesDocument48 pagesChapter 1 Current LiabilitiesNeighvest100% (1)

- Egypt Debtor PolicyDocument13 pagesEgypt Debtor PolicyKhaled SherifNo ratings yet

- Duties of a Drawing & Disbursing OfficerDocument42 pagesDuties of a Drawing & Disbursing OfficerKotashiva KrishnaNo ratings yet

- Topic Five: Refund and Retention of Revenue: Ibrahim Abby YusufDocument18 pagesTopic Five: Refund and Retention of Revenue: Ibrahim Abby YusufProf. SchleidenNo ratings yet

- FM LaDocument115 pagesFM LaSamNo ratings yet

- ELCCG - Fin04 Provision For and Write Off of Bad Debts Policy V3Document10 pagesELCCG - Fin04 Provision For and Write Off of Bad Debts Policy V3DavidNo ratings yet

- NPA MGMTDocument60 pagesNPA MGMTRajib Ranjan SamalNo ratings yet

- Unit A 1Document12 pagesUnit A 1Karl Lincoln TemporosaNo ratings yet

- Intention To Acquire Goods in The FutureDocument21 pagesIntention To Acquire Goods in The Futurecynthia reyesNo ratings yet

- Group 1 Budget ProcessDocument26 pagesGroup 1 Budget ProcessCassie ParkNo ratings yet

- Accounting Standards: 2.1 AS 4: Contingencies and Events Occurring After The Balance Sheet DateDocument0 pagesAccounting Standards: 2.1 AS 4: Contingencies and Events Occurring After The Balance Sheet DateThéotime HabinezaNo ratings yet

- LiabilitiesDocument4 pagesLiabilitiesarkishaNo ratings yet

- Liabilities: Chidelyn Aguado, Marian Andrage, Wincer Alonzaga, Chincel AniDocument57 pagesLiabilities: Chidelyn Aguado, Marian Andrage, Wincer Alonzaga, Chincel AniChincel AniNo ratings yet

- Acc 106Document66 pagesAcc 106ananimus ananimusNo ratings yet

- Audit of LiabilitiesDocument12 pagesAudit of LiabilitiesAcier KozukiNo ratings yet

- General Financial Rules 2017Document62 pagesGeneral Financial Rules 2017ADITYA GAHLAUT0% (1)

- Accounting For Specialized Institution Set 2 Scheme of ValuationDocument19 pagesAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Role of Different Parties in Public Financial ManagementDocument8 pagesRole of Different Parties in Public Financial ManagementharishayinisureshNo ratings yet

- Accounts Receivable System For TPITDocument6 pagesAccounts Receivable System For TPITFokso FutekoNo ratings yet

- Audit Programme For Audit of BanksDocument8 pagesAudit Programme For Audit of BanksGaurav AgrawalNo ratings yet

- AFAR 2304 Government AccountingDocument17 pagesAFAR 2304 Government AccountingDzulija TalipanNo ratings yet

- Closing Guidelines 2023-24 (1)Document68 pagesClosing Guidelines 2023-24 (1)Nikhil Kharat NiCkNo ratings yet

- Understanding The SelfDocument9 pagesUnderstanding The SelfNatalie SerranoNo ratings yet

- Chapter 1 Statement of Financial PositionDocument9 pagesChapter 1 Statement of Financial PositionblancocarizagioNo ratings yet

- Financial Statements QuizDocument6 pagesFinancial Statements QuizDonna TumalaNo ratings yet

- Module 1-LIABILITIES and PREMIUM LIABILITYDocument10 pagesModule 1-LIABILITIES and PREMIUM LIABILITYKathleen SalesNo ratings yet

- Review Notes #2 PDFDocument9 pagesReview Notes #2 PDFJha Ya100% (3)

- 2023 COALA1 Week 5 Transfer Procedures & Correspondent AccountsDocument44 pages2023 COALA1 Week 5 Transfer Procedures & Correspondent Accountsnandinhlapo96No ratings yet

- Module 1Document31 pagesModule 1Jiane SanicoNo ratings yet

- Question 1Document8 pagesQuestion 1Anna ZielinskaNo ratings yet

- Present ObligationDocument6 pagesPresent ObligationArgem Jay PorioNo ratings yet

- Bank Audit RelatedDocument6 pagesBank Audit RelatedNikhil Kharat NiCkNo ratings yet

- Accounting for Budgetary AccountsDocument63 pagesAccounting for Budgetary Accountselisha mae cardeñoNo ratings yet

- C1 LiabilitiesDocument20 pagesC1 LiabilitiesJomar MarananNo ratings yet

- Current LiabilitiesDocument87 pagesCurrent LiabilitiestheheckwithitNo ratings yet

- State Bank Learning Centre e-gyan Vol 1 Key HighlightsDocument13 pagesState Bank Learning Centre e-gyan Vol 1 Key Highlightsmevrick_guyNo ratings yet

- 1502448534501G O 43,22 4 2000withsignDocument14 pages1502448534501G O 43,22 4 2000withsignNITHIN SAI CHINTHALANo ratings yet

- Integrated Accounting: Financial Accounting & Reporting (P1) Integrated Accounting - Far (P1) Module 4: LiabilitiesDocument10 pagesIntegrated Accounting: Financial Accounting & Reporting (P1) Integrated Accounting - Far (P1) Module 4: LiabilitiesKamyll VidadNo ratings yet

- Role of DDO-PresentationDocument24 pagesRole of DDO-PresentationBalu Mahendra SusarlaNo ratings yet

- Briefly Discuss The Insolvency Process.: 1. Corporate Debtors: Two-Stage ProcessDocument2 pagesBriefly Discuss The Insolvency Process.: 1. Corporate Debtors: Two-Stage Processvyakhya khatriNo ratings yet

- Proper Execution of Waiver of Statute of LimitationsDocument2 pagesProper Execution of Waiver of Statute of LimitationsKobi SaibenNo ratings yet

- Copy 7 ACP 313 QuickNotes On Government AccountingDocument10 pagesCopy 7 ACP 313 QuickNotes On Government AccountingRodken VallenteNo ratings yet

- Audit Liabilities NotesDocument15 pagesAudit Liabilities NotesJoanne Pauline Ochea100% (2)

- MB0041-Finance & Management Accounting Mba 1 Semester Assignment Set - 1Document12 pagesMB0041-Finance & Management Accounting Mba 1 Semester Assignment Set - 1Abhinav TelidevaraNo ratings yet

- Accounting For Local Government Unit I. Basic Fatures and PoliciesDocument10 pagesAccounting For Local Government Unit I. Basic Fatures and PoliciesChin-Chin Alvarez SabinianoNo ratings yet

- Disbursements MommyDocument61 pagesDisbursements MommyLyn CarlosNo ratings yet

- Tax RemediesDocument6 pagesTax RemediesJollibee Bida BidaNo ratings yet

- Intermediate Accounting 1A 2019 by Millan Chapter 1-Summary (Accounting Process)Document5 pagesIntermediate Accounting 1A 2019 by Millan Chapter 1-Summary (Accounting Process)Shaina DellomesNo ratings yet

- Current Liabilities, Provisions and Contingencies UPDATEDDocument82 pagesCurrent Liabilities, Provisions and Contingencies UPDATEDPaolo Perandos100% (2)

- COA Presentation - RRSADocument155 pagesCOA Presentation - RRSAKristina Dacayo-Garcia100% (1)

- Accounting For Special Transactions:: Corporate LiquidationDocument28 pagesAccounting For Special Transactions:: Corporate LiquidationKim EllaNo ratings yet

- Here are the amounts that should be reported as cash and cash equivalents for each company:1. PILI NUT Company - P1,869,8002. MUSIC CO. - P2,432,000 3. OTTO CO. - P13,347,500Document11 pagesHere are the amounts that should be reported as cash and cash equivalents for each company:1. PILI NUT Company - P1,869,8002. MUSIC CO. - P2,432,000 3. OTTO CO. - P13,347,500Justine FloresNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- PracticalTipps Broschuere NAP DINA5 Engl WEB 210409Document26 pagesPracticalTipps Broschuere NAP DINA5 Engl WEB 210409Gere TassewNo ratings yet

- Application FormDocument12 pagesApplication FormGere TassewNo ratings yet

- Guideline For Write-Off of Non-Performing Assets 14.11.2018 - FinalDocument7 pagesGuideline For Write-Off of Non-Performing Assets 14.11.2018 - FinalGere TassewNo ratings yet

- 21 01 04 DefinitionsDocument1 page21 01 04 DefinitionsGere TassewNo ratings yet

- Un Habitat Finance Policies and Procedures 2013Document198 pagesUn Habitat Finance Policies and Procedures 2013Mesfin MahtemeselaseNo ratings yet

- Social Enterprise in Germany - Understanding Concetps and ContextDocument32 pagesSocial Enterprise in Germany - Understanding Concetps and ContextGere TassewNo ratings yet

- AABE's Roadmap for IPSAS ImplementationDocument66 pagesAABE's Roadmap for IPSAS ImplementationGere Tassew100% (1)

- 3 Checklists For 80 - Productive MeetingsDocument25 pages3 Checklists For 80 - Productive MeetingsGere TassewNo ratings yet

- IFRS 16 - Leases and The Impact On Credit InstitutionsDocument15 pagesIFRS 16 - Leases and The Impact On Credit InstitutionsGere TassewNo ratings yet

- Fair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaDocument60 pagesFair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaGere Tassew100% (1)

- TOR LED Mid-Term EvaluationDocument7 pagesTOR LED Mid-Term EvaluationGere TassewNo ratings yet

- Lecture 3: Memory Buffers and SchedulingDocument21 pagesLecture 3: Memory Buffers and SchedulingGere TassewNo ratings yet

- Asklepios gb18 en Online PDFDocument108 pagesAsklepios gb18 en Online PDFGere TassewNo ratings yet

- Sample IPSAS Implementation Road Map Based On TheDocument4 pagesSample IPSAS Implementation Road Map Based On TheGere TassewNo ratings yet

- Fair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaDocument60 pagesFair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaGere Tassew100% (1)

- Basics of Valuation ConceptsDocument16 pagesBasics of Valuation ConceptsGere TassewNo ratings yet

- Basics of Valuation ConceptsDocument16 pagesBasics of Valuation ConceptsGere TassewNo ratings yet

- F1eb PDFDocument68 pagesF1eb PDFGere TassewNo ratings yet

- Open Safari Case StudyDocument37 pagesOpen Safari Case Studybangucok123No ratings yet

- Ethiopia D2S2a Extract From The Open Safari Case Study PDFDocument1 pageEthiopia D2S2a Extract From The Open Safari Case Study PDFGere TassewNo ratings yet

- 10 Finance Policies and Procedures Manual - TEMPLATE PDFDocument60 pages10 Finance Policies and Procedures Manual - TEMPLATE PDFGere TassewNo ratings yet

- Ethiopia D1S4b Soc Gen Case StudyDocument4 pagesEthiopia D1S4b Soc Gen Case StudyGere TassewNo ratings yet

- Leasing 090806121819 Phpapp01 PDFDocument35 pagesLeasing 090806121819 Phpapp01 PDFGere TassewNo ratings yet

- IFRS Core Tools PDFDocument33 pagesIFRS Core Tools PDFGere TassewNo ratings yet

- FATF report highlights vital role of authorities in combating financial flows from illegal wildlife tradeDocument6 pagesFATF report highlights vital role of authorities in combating financial flows from illegal wildlife tradeGere TassewNo ratings yet

- Accounting Standard-16: Borrowing CostsDocument19 pagesAccounting Standard-16: Borrowing CostsGere TassewNo ratings yet

- Ifrs 8: Operating SegmentsDocument12 pagesIfrs 8: Operating SegmentsGere TassewNo ratings yet

- IFRS 6 E&E Assets Impairment DisclosuresDocument18 pagesIFRS 6 E&E Assets Impairment DisclosuresGere TassewNo ratings yet

- Model ETF Portfolios: iShares Returns and AllocationsDocument3 pagesModel ETF Portfolios: iShares Returns and AllocationsmusicbrahNo ratings yet

- Capital Structure of Jindal Steel and PowerDocument2 pagesCapital Structure of Jindal Steel and PowerAshok VenkatNo ratings yet

- Iifl - M-Reit - Kyc - 20200915Document37 pagesIifl - M-Reit - Kyc - 20200915Saatvik ShettyNo ratings yet

- E5-19 Journal EntriesDocument15 pagesE5-19 Journal EntriesDzaky FarhansyahNo ratings yet

- Statement of Financial Position ActivityDocument3 pagesStatement of Financial Position ActivityHannah Mae JaguinesNo ratings yet

- Ranchi University M.com SyllabusDocument42 pagesRanchi University M.com SyllabusFarhan AkhtarNo ratings yet

- Introduction to financial managementDocument37 pagesIntroduction to financial managementBritney BowersNo ratings yet

- Audit of Property, Plant and Equipment and Intangible AssetsDocument8 pagesAudit of Property, Plant and Equipment and Intangible AssetsEsse ValdezNo ratings yet

- Partnership FormationDocument45 pagesPartnership FormationJwhll MaeNo ratings yet

- MBA Group Learning Diary and Financial Statements AnalysisDocument24 pagesMBA Group Learning Diary and Financial Statements AnalysisRaluca UrseNo ratings yet

- A211 MC4 MFRS108 Mfrs110-StudentDocument6 pagesA211 MC4 MFRS108 Mfrs110-StudentGui Xue ChingNo ratings yet

- 4.1 Mat112 DepreciationDocument1 page4.1 Mat112 Depreciation2023300633No ratings yet

- FINANCE FUNCTIONS AND MANAGEMENTDocument13 pagesFINANCE FUNCTIONS AND MANAGEMENTCharming AshishNo ratings yet

- Financial ManagementDocument8 pagesFinancial Managementoptimistic070% (1)

- Firoz MBA 4 Sem Final PRJCTDocument21 pagesFiroz MBA 4 Sem Final PRJCTFiroz Shaikh100% (1)

- MFF Convention Emphatic Accounts Live Funds Trading PayoutsDocument4 pagesMFF Convention Emphatic Accounts Live Funds Trading Payoutsmacosd4450No ratings yet

- Financial Management Time Value ProblemsDocument39 pagesFinancial Management Time Value Problemsprashanth1911820% (2)

- Abay Bank Call Written Exam For The Post of Customer Service OfficerDocument36 pagesAbay Bank Call Written Exam For The Post of Customer Service OfficerGetacher Niguse100% (1)

- 11.11.07 wp438Document41 pages11.11.07 wp438Thanhtam NhiNo ratings yet

- Finance Interview Dictionary GuideDocument44 pagesFinance Interview Dictionary GuideRahul GandhiNo ratings yet

- Lauren Manufacturing Company Cost Report AnalysisDocument4 pagesLauren Manufacturing Company Cost Report Analysisjose abalayanNo ratings yet

- Adnan Ahsan Assignment 1 Bond ValuationDocument8 pagesAdnan Ahsan Assignment 1 Bond Valuationmuhammad hasanNo ratings yet

- Applied Value Investing Session 1Document138 pagesApplied Value Investing Session 1adityaNo ratings yet

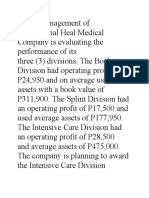

- International Heal Medical evaluates divisions' performanceDocument6 pagesInternational Heal Medical evaluates divisions' performanceGillai Marie IbardolazaNo ratings yet

- Research Project on Performance of Income Mutual FundsDocument51 pagesResearch Project on Performance of Income Mutual FundsYoutube PremiumNo ratings yet

- CH 5Document10 pagesCH 5Miftahudin MiftahudinNo ratings yet

- Report Dairy Milk Management SystemDocument44 pagesReport Dairy Milk Management SystemSathishNo ratings yet