You might also like

- Essential Soft Skills for Lawyers: What They Are and How to Develop ThemFrom EverandEssential Soft Skills for Lawyers: What They Are and How to Develop ThemNo ratings yet

- TZERO White PaperDocument27 pagesTZERO White PaperFran Frankel92% (13)

- Business Interruption: Coverage, Claims, and Recovery, 2nd EditionFrom EverandBusiness Interruption: Coverage, Claims, and Recovery, 2nd EditionNo ratings yet

- FARFIS Intermolecular Forces Multiple Choice QuestionsDocument3 pagesFARFIS Intermolecular Forces Multiple Choice QuestionsRezky SaputraNo ratings yet

- CH 10Document84 pagesCH 10Michael Fine100% (2)

- Ep Group 2 Syllabus Dec 05032023Document81 pagesEp Group 2 Syllabus Dec 05032023deepanshudonaladsingh11arosaryNo ratings yet

- Clearing and SettlementDocument12 pagesClearing and Settlementneelabh_singh_1No ratings yet

- Business SecuritiesDocument19 pagesBusiness SecuritiesStephens Tioluwanimi Oluwadamilare100% (5)

- Financial Markets & Instruments - Assignment 1Document3 pagesFinancial Markets & Instruments - Assignment 1Aditi RawatNo ratings yet

- 144 ADocument9 pages144 AAmrin NazNo ratings yet

- Economicall West Frn0018268748 Cpni Compliance Cert 2013Document1 pageEconomicall West Frn0018268748 Cpni Compliance Cert 2013Federal Communications Commission (FCC)No ratings yet

- PHD Thesis Stock ExchangeDocument4 pagesPHD Thesis Stock ExchangeWebsiteThatWillWriteAPaperForYouSingapore100% (2)

- Clearing & Settlement PDFDocument24 pagesClearing & Settlement PDFGourav GoyelNo ratings yet

- Darryl Crowe Sony Playstation Network Csol-520 December 14Th, 2020 Professor Thomas PlunkettDocument11 pagesDarryl Crowe Sony Playstation Network Csol-520 December 14Th, 2020 Professor Thomas Plunkettapi-594428506No ratings yet

- Study Material-MergedDocument127 pagesStudy Material-Mergedstudysks2324No ratings yet

- Securities On The BlockchainDocument26 pagesSecurities On The BlockchainDai Dong Dao PhapNo ratings yet

- Docket ID OCC-2011-0008 Docket No. R-1415 RIN 7100 AD74 RIN 3064-AD79Document6 pagesDocket ID OCC-2011-0008 Docket No. R-1415 RIN 7100 AD74 RIN 3064-AD79MarketsWikiNo ratings yet

- STO Research ReportDocument17 pagesSTO Research ReportDavit KhachikyanNo ratings yet

- Markit Data Guide: Part Number: 077 - 106 Date: July 24, 2007Document18 pagesMarkit Data Guide: Part Number: 077 - 106 Date: July 24, 2007rohanmanxNo ratings yet

- V05 C08 EstimatDocument9 pagesV05 C08 EstimatPalanisamyNo ratings yet

- SEC Testimony On Virtual CurrenciesDocument71 pagesSEC Testimony On Virtual CurrenciesCharles Hoskinson100% (5)

- ALLDocument16 pagesALLKim Ngân PhanNo ratings yet

- Programming QuestionDocument5 pagesProgramming QuestionLuxmi Kumar MdhesiyaNo ratings yet

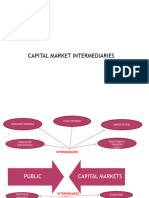

- Capital Market IntermediariesDocument31 pagesCapital Market IntermediariesNivesh DixitNo ratings yet

- 209 - F - IndiabullsDocument75 pages209 - F - IndiabullsPeacock Live ProjectsNo ratings yet

- Dld-Traditional & Vul Insurance Concepts - Final - (Edits 011022)Document233 pagesDld-Traditional & Vul Insurance Concepts - Final - (Edits 011022)Renz LanuzaNo ratings yet

- Investment BankerDocument2 pagesInvestment BankerAnna Lyssa BatasNo ratings yet

- Econo Legal Opinion On A Series A Investment in A Startup 1591528511Document31 pagesEcono Legal Opinion On A Series A Investment in A Startup 1591528511ShekinahNo ratings yet

- Basics of Stock Market For BeginnersDocument58 pagesBasics of Stock Market For BeginnersYatharth DassNo ratings yet

- Stock Market - Simran EditDocument4 pagesStock Market - Simran EditManinder KaurNo ratings yet

- Securities Law FrameworkDocument28 pagesSecurities Law FrameworkKelvin FuNo ratings yet

- CSA Canada ICO-OfferingsDocument6 pagesCSA Canada ICO-OfferingsCrowdfundInsiderNo ratings yet

- CDSC FAQ EnglishDocument44 pagesCDSC FAQ EnglishSanjeev Bikram KarkiNo ratings yet

- Capital MarketDocument43 pagesCapital MarketmurkyNo ratings yet

- Easiest OperatingInstructions BODocument24 pagesEasiest OperatingInstructions BOidkwhiiNo ratings yet

- Potential LitigationDocument7 pagesPotential Litigationnbroom123No ratings yet

- Ey The Valuation of Crypto AssetsDocument24 pagesEy The Valuation of Crypto AssetsDeming ZhuNo ratings yet

- Trade Initiation Stage Trade Execution Stage Trade Capture Stage Trade EnrichmentDocument5 pagesTrade Initiation Stage Trade Execution Stage Trade Capture Stage Trade EnrichmentNitish JhaNo ratings yet

- Securities-Law WordDocument36 pagesSecurities-Law WordencinajarianjayNo ratings yet

- Chapter 2Document6 pagesChapter 2Sricharan MNo ratings yet

- HSC SP Q.5. Answer in Brief PDFDocument4 pagesHSC SP Q.5. Answer in Brief PDFTanya SinghNo ratings yet

- Financial Market Managment1Document14 pagesFinancial Market Managment1SsNo ratings yet

- FAQ's Commodity: 1. How Can I Activate Commodity Segment For My Trading Account Held With SSL?Document9 pagesFAQ's Commodity: 1. How Can I Activate Commodity Segment For My Trading Account Held With SSL?AJAYNo ratings yet

- Negotiated Deaing SystemDocument10 pagesNegotiated Deaing Systemtsamitsah837No ratings yet

- 098 Fmbo-2-Ketaki NikamDocument10 pages098 Fmbo-2-Ketaki NikamKetakiNo ratings yet

- Abridged Letter of Offer Equity 01102021Document12 pagesAbridged Letter of Offer Equity 01102021Nitesh BairagiNo ratings yet

- Trust-Overview Handouts PDFDocument14 pagesTrust-Overview Handouts PDFShobhit UmraoNo ratings yet

- Depository System - Company LawDocument5 pagesDepository System - Company LawPAULOMI DASNo ratings yet

- Perfect Competition Case Study On Stock ExchangeDocument29 pagesPerfect Competition Case Study On Stock Exchangegagan3211100% (1)

- Religare EQUITY FINAL DetailsDocument75 pagesReligare EQUITY FINAL DetailsVarun KumarNo ratings yet

- OGL 481 Pro-Seminar I: PCA-Human Resource Frame WorksheetDocument4 pagesOGL 481 Pro-Seminar I: PCA-Human Resource Frame Worksheetapi-603022252No ratings yet

- Web-Appendix - Transition Risk Stress Test Versie 2018-10-08 Voor Web - tcm46-379400 PDFDocument28 pagesWeb-Appendix - Transition Risk Stress Test Versie 2018-10-08 Voor Web - tcm46-379400 PDFmilkNo ratings yet

- Securities Reg OutlineDocument114 pagesSecurities Reg Outlined8n1007No ratings yet

- Code of Conduct For Exchanges ChiEngDocument9 pagesCode of Conduct For Exchanges ChiEngDanny LinNo ratings yet

- Chapter 1Document34 pagesChapter 1sahumonikaNo ratings yet

- Reporting Violations and Whistleblower Manual MEXDocument9 pagesReporting Violations and Whistleblower Manual MEXMuhammad Shoaib AkramNo ratings yet

- It Now Trades On 18 ExchangesDocument7 pagesIt Now Trades On 18 ExchangesDouglas SlainNo ratings yet

- Procedure Dor Demat Acc Opening BY THE HUSTLERSDocument8 pagesProcedure Dor Demat Acc Opening BY THE HUSTLERSSankhadeep DebdasNo ratings yet

- CHAPTER NO 4 Ventura LTDDocument6 pagesCHAPTER NO 4 Ventura LTDamir420007No ratings yet

- Exercise-1 SMRDocument4 pagesExercise-1 SMRTime-Lapse CamNo ratings yet

- MECANISMOS de Metais de TransicaoDocument36 pagesMECANISMOS de Metais de TransicaoJoão BarbosaNo ratings yet

- Rhodopsin Dyes For Polyamide by RDNDocument96 pagesRhodopsin Dyes For Polyamide by RDNSaidul KarimNo ratings yet

- 50 Stronghold Insurance Co. v. Tokyu ConstructionDocument1 page50 Stronghold Insurance Co. v. Tokyu ConstructionGSSNo ratings yet

- Functional Group NamesDocument21 pagesFunctional Group NamesAdine RaissaNo ratings yet

- HARRISBURGBONDSHarrisburg Insiders Trash The Forgotten TaxpayerDocument4 pagesHARRISBURGBONDSHarrisburg Insiders Trash The Forgotten TaxpayerBob GuzzardiNo ratings yet

- Families of Carbon Compounds: Functional Groups, Intermolecular Forces, & Infrared (IR) SpectrosDocument79 pagesFamilies of Carbon Compounds: Functional Groups, Intermolecular Forces, & Infrared (IR) SpectrosRuryKharismaMuzaqieNo ratings yet

- Acrylic UrethaneDocument12 pagesAcrylic UrethaneBala Singam100% (1)

- Money Market in India: Presented By: Manish Jain Mridul Chawla Kunal GoelDocument22 pagesMoney Market in India: Presented By: Manish Jain Mridul Chawla Kunal Goelkunal goelNo ratings yet

- Formal ChargeDocument15 pagesFormal ChargeTahir HussainNo ratings yet

- Chapter 10Document158 pagesChapter 10Hafizszul FeyzulNo ratings yet

- Notice: Railroad Services Abandonment: Pittsburg & Shawmut Railroad, LLCDocument2 pagesNotice: Railroad Services Abandonment: Pittsburg & Shawmut Railroad, LLCJustia.comNo ratings yet

- StandardAndPoors Corporate Ratings Criteria PDFDocument114 pagesStandardAndPoors Corporate Ratings Criteria PDFAnonymous fjgmbzTNo ratings yet

- Chemistry Quiz Chapter 5 Form 4 @Document4 pagesChemistry Quiz Chapter 5 Form 4 @Mohd NorihwanNo ratings yet

- Markets and Commodity Figures: Total Market Turnover StatisticsDocument6 pagesMarkets and Commodity Figures: Total Market Turnover StatisticsTiso Blackstar GroupNo ratings yet

- HYDocument2 pagesHYkarasa1No ratings yet

- Syndicated Loans BrochureDocument24 pagesSyndicated Loans BrochurefaiyazadamNo ratings yet

- Illustration 1: Debt Component Equity ComponentDocument10 pagesIllustration 1: Debt Component Equity ComponentTrang LêNo ratings yet

- Hydro Borat I OnDocument198 pagesHydro Borat I OnEman MoustafaNo ratings yet

- PolymerDocument36 pagesPolymersabetNo ratings yet

- Sukuk Market in Saudi ArabiaDocument19 pagesSukuk Market in Saudi ArabiafathalbabNo ratings yet

- Do - 026 - S2011 (Ibd-Dpwh Diggind On Natl Roads) PDFDocument20 pagesDo - 026 - S2011 (Ibd-Dpwh Diggind On Natl Roads) PDFgabinuang100% (4)

- Leep 501Document16 pagesLeep 501Udit ChaudharyNo ratings yet

- PS3SDFSDFDocument3 pagesPS3SDFSDFsillNo ratings yet

- Basics of Bond Mathematics: Sankarshan BasuDocument68 pagesBasics of Bond Mathematics: Sankarshan BasuUdit GuptaNo ratings yet

- AC2101 SemGrp4 Team4 (Updated)Document41 pagesAC2101 SemGrp4 Team4 (Updated)Kwang Yi JuinNo ratings yet

- Project IN Science: Inorganic CompoundDocument11 pagesProject IN Science: Inorganic CompoundKenneth V PamaNo ratings yet

- Difference Between Bail and Bond (With Comparison Chart) - Key DifferencesDocument4 pagesDifference Between Bail and Bond (With Comparison Chart) - Key DifferencesGaurav Prakash JaiswalNo ratings yet

- Ferric OxalateDocument11 pagesFerric OxalateJoao Diniz100% (1)