You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Ia2 Final Exam A Test Bank - CompressDocument32 pagesIa2 Final Exam A Test Bank - CompressFiona MiralpesNo ratings yet

- NOTES AND INVENTORIES KEY CONCEPTSDocument10 pagesNOTES AND INVENTORIES KEY CONCEPTSAlizah Lariosa BucotNo ratings yet

- Book 1Document2 pagesBook 1Shiela DimaculanganNo ratings yet

- MILLAN CHAPTER 6 Receivables - Additional ConceptsDocument16 pagesMILLAN CHAPTER 6 Receivables - Additional Concepts밀크milkeuNo ratings yet

- Sol. Man. - Chapter 6 - Receivables - Addtl Concepts - Ia Part 1a - 2020 EditionDocument13 pagesSol. Man. - Chapter 6 - Receivables - Addtl Concepts - Ia Part 1a - 2020 EditionJapon, Jenn RossNo ratings yet

- Urdaneta City University Accounts Receivable ChapterDocument12 pagesUrdaneta City University Accounts Receivable ChapterKyla Joy T. SanchezNo ratings yet

- Intacc2 Chapter 3 Answer KeysDocument24 pagesIntacc2 Chapter 3 Answer KeysATHALIAH LUNA MERCADEJASNo ratings yet

- (Chapter 3) Sol Man Intermediate Accounting 2 by Zeus MillanDocument24 pages(Chapter 3) Sol Man Intermediate Accounting 2 by Zeus MillanJonathan Villazon RosalesNo ratings yet

- Pa4-Chapter-3.Garcia J John Vincent DDocument5 pagesPa4-Chapter-3.Garcia J John Vincent DJohn Vincent GarciaNo ratings yet

- Module 5 Notes PayableDocument4 pagesModule 5 Notes PayableAngelie Bocala CatalanNo ratings yet

- Bonds Payable Chapter ConceptsDocument23 pagesBonds Payable Chapter ConceptsAndrei BernardoNo ratings yet

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNo ratings yet

- Notes Payable: Problem 1: True or FalseDocument16 pagesNotes Payable: Problem 1: True or FalseKim HanbinNo ratings yet

- Sol. Man. - Chapter 7 Leases Part 1Document12 pagesSol. Man. - Chapter 7 Leases Part 1Miguel Amihan100% (1)

- Acc 106 P3 LessonDocument6 pagesAcc 106 P3 LessonRowella Mae VillenaNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- Intermediate Accounting 2 Final ExamDocument35 pagesIntermediate Accounting 2 Final ExamJEFFERSON CUTE97% (32)

- (Chapter 2) Sol Man of Intermediate Accounting 2 by Zeus MillanDocument17 pages(Chapter 2) Sol Man of Intermediate Accounting 2 by Zeus MillanJonathan Villazon RosalesNo ratings yet

- Intermediate Accounting 1 Second Grading Examination Key AnswersDocument12 pagesIntermediate Accounting 1 Second Grading Examination Key AnswersAbegail Joy De GuzmanNo ratings yet

- Sol. Man. - Chapter 8 Leases Part 2Document9 pagesSol. Man. - Chapter 8 Leases Part 2Miguel Amihan100% (1)

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- PracticeSet BondsPayableDocument5 pagesPracticeSet BondsPayablearabelle contrerasNo ratings yet

- Answers - Chapter 1 - Current LiabilitiesDocument5 pagesAnswers - Chapter 1 - Current LiabilitiesLhica EsterasNo ratings yet

- National Bank Grants A 10Document2 pagesNational Bank Grants A 10George PascualNo ratings yet

- Intermediate Accounting 2 Millan 221013 124345Document233 pagesIntermediate Accounting 2 Millan 221013 124345Krazy Butterfly100% (1)

- Intermediate Accounting 1A Chapter 10 - Investment in Debt Securities Problem 3Document5 pagesIntermediate Accounting 1A Chapter 10 - Investment in Debt Securities Problem 3Yuki BarracaNo ratings yet

- Due Date Revised Payments PV of 1 @12%, N 0 1 and 2 Present ValueDocument2 pagesDue Date Revised Payments PV of 1 @12%, N 0 1 and 2 Present ValueCamille HornillaNo ratings yet

- Chapter 8 Leases Part 2Document9 pagesChapter 8 Leases Part 2Thalia Rhine AberteNo ratings yet

- Bonds Payable Quiz Part 2Document5 pagesBonds Payable Quiz Part 2justine reine cornico100% (1)

- Group Activities in Receivable FinancingDocument2 pagesGroup Activities in Receivable FinancingTrisha VillegasNo ratings yet

- Solutions Guide: This Is Meant As A Solutions GuideDocument4 pagesSolutions Guide: This Is Meant As A Solutions GuideVivienne Lei BolosNo ratings yet

- ACC106 Notes Receivable IllustrationsDocument23 pagesACC106 Notes Receivable IllustrationsJohn MaynardNo ratings yet

- Problem 6-1: Interest Expense Present ValueDocument3 pagesProblem 6-1: Interest Expense Present ValueAngieNo ratings yet

- Current Liabilities ChapterDocument8 pagesCurrent Liabilities ChapterJonathan Villazon Rosales67% (3)

- Calculating Present Value of Notes ReceivableDocument8 pagesCalculating Present Value of Notes Receivablefinn mertensNo ratings yet

- Problem 5-3 Requirement 1 2020Document7 pagesProblem 5-3 Requirement 1 2020Adyagila Ecarg NelehNo ratings yet

- Chapter 14 HomeworkDocument10 pagesChapter 14 HomeworkSaja AlbarjesNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- Acctg 4 Serdan Quiz 3Document7 pagesAcctg 4 Serdan Quiz 3Rica CatanguiNo ratings yet

- Leases (Part 2) : Problem 1: True or FalseDocument23 pagesLeases (Part 2) : Problem 1: True or FalseKim Hanbin100% (1)

- BAT Unit 5 AssignmentDocument14 pagesBAT Unit 5 AssignmentTalhah WaleedNo ratings yet

- NUDJPIA FAR AND AFAR SOLUTIONS - ReceivablesDocument6 pagesNUDJPIA FAR AND AFAR SOLUTIONS - ReceivablesKyla Artuz Dela CruzNo ratings yet

- Homework SolutionsDocument5 pagesHomework SolutionsAnonymous CuUAaRSNNo ratings yet

- Notes Receivable Chapter 5 SummaryDocument20 pagesNotes Receivable Chapter 5 SummaryJapon, Jenn RossNo ratings yet

- Chapter 22 Current Liabilities ReviewDocument8 pagesChapter 22 Current Liabilities ReviewErwin Dave M. DahaoNo ratings yet

- Ias 32Document3 pagesIas 32Yến Hoàng HảiNo ratings yet

- Computing Present Value For Unequal Periodic PaymentsDocument2 pagesComputing Present Value For Unequal Periodic PaymentsCJ GranadaNo ratings yet

- Bonds Payable Issued at A DiscountDocument10 pagesBonds Payable Issued at A DiscountCris Ann Marie ESPAnOLANo ratings yet

- Bond valuation and stock issuance calculationsDocument13 pagesBond valuation and stock issuance calculationsHENDY YUDHA PRAMANANo ratings yet

- Problem 5 On Loan ReceivableDocument6 pagesProblem 5 On Loan Receivablebm1ma.allysaamorNo ratings yet

- Assignment 1 - SolutionsDocument3 pagesAssignment 1 - SolutionsEsther LiuNo ratings yet

- Chapter 5 Notes Receivable Ia Part 1aDocument12 pagesChapter 5 Notes Receivable Ia Part 1aannyeongNo ratings yet

- Audit of Long Term Liabilities 2Document5 pagesAudit of Long Term Liabilities 2Cesar EsguerraNo ratings yet

- Note PayableDocument6 pagesNote PayablemmhNo ratings yet

- Intacc1A M5Assignment KeyDocument9 pagesIntacc1A M5Assignment KeyGabriel AfricaNo ratings yet

- Lease Acctg ExerciseDocument12 pagesLease Acctg ExerciseIts meh SushiNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Soce2023bskeforms Form2Document1 pageSoce2023bskeforms Form2lavariasmarjorieanne211100% (2)

- Soce2023bskeforms Form3Document1 pageSoce2023bskeforms Form3JENNo ratings yet

- Detailed Lesson Plan in Music 6Document8 pagesDetailed Lesson Plan in Music 6Irene Grace Edralin AdenaNo ratings yet

- Detailed Lesson Plan in Arts 1Document11 pagesDetailed Lesson Plan in Arts 1Irene Grace Edralin AdenaNo ratings yet

- Basic Introduction of MS ExcelDocument9 pagesBasic Introduction of MS ExcelIrene Grace Edralin AdenaNo ratings yet

- Bank lending policies procedures factors determining loan growth mixDocument14 pagesBank lending policies procedures factors determining loan growth mixNadia VirkNo ratings yet

- ACC5116 - HOBA - Additional ProblemsDocument6 pagesACC5116 - HOBA - Additional ProblemsCarl Dhaniel Garcia Salen100% (1)

- Opening Saving Account in HDFC BankDocument31 pagesOpening Saving Account in HDFC BankSukhchain AggarwalNo ratings yet

- Chapter 4 Money Banks (First) PPTDocument22 pagesChapter 4 Money Banks (First) PPTSoha HassanNo ratings yet

- Law 3 PrelimDocument5 pagesLaw 3 PrelimJohn Rey Bantay RodriguezNo ratings yet

- Microsoft Word - CHAPTER - 05 - DEPOSITS - IN - BANKSDocument8 pagesMicrosoft Word - CHAPTER - 05 - DEPOSITS - IN - BANKSDuy Trần TấnNo ratings yet

- Noel Bergonia's Accounting Policies and Estimates GuideDocument8 pagesNoel Bergonia's Accounting Policies and Estimates GuideMika MolinaNo ratings yet

- Detailed Statement: Transactions List - GOOD HOME INC (INR) - 051405500242Document6 pagesDetailed Statement: Transactions List - GOOD HOME INC (INR) - 051405500242aliNo ratings yet

- Topic 1: & Overview of Financial SystemDocument71 pagesTopic 1: & Overview of Financial SystemSarifah SaidsaripudinNo ratings yet

- Promotion Test Material For Officers PDFDocument730 pagesPromotion Test Material For Officers PDFarunrajchoyNo ratings yet

- Financial Accounting 2Document54 pagesFinancial Accounting 2Azee AskingNo ratings yet

- CH 12 P1Document2 pagesCH 12 P1GlaizzaNo ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingvikramtambeNo ratings yet

- M and N 1Document1 pageM and N 1DDdNo ratings yet

- Imp Key Indicators of RRBs 2013Document6 pagesImp Key Indicators of RRBs 2013Pankaj SharmaNo ratings yet

- BDODocument2 pagesBDOBevegel Sasan LlidoNo ratings yet

- RBI Master Circular on Customer ServiceDocument150 pagesRBI Master Circular on Customer ServiceVenkatNo ratings yet

- Change in PSR Test 1Document4 pagesChange in PSR Test 1Faujdar TanishkNo ratings yet

- DUMSSBDDDDocument3 pagesDUMSSBDDDUBCREATIONZ 2019No ratings yet

- Z LKQ EV2 Gaw 58 Cwya 9 M5 Elnqc Diy 7 K KX SF BR SW4 FKDocument1 pageZ LKQ EV2 Gaw 58 Cwya 9 M5 Elnqc Diy 7 K KX SF BR SW4 FKMark RerichaNo ratings yet

- ReceiptDocument1 pageReceiptAbdul Hadi Rashid100% (1)

- CompendiumDocument18 pagesCompendiumpranithroyNo ratings yet

- Verification of Insurance for JEREMY WAREDocument1 pageVerification of Insurance for JEREMY WAREJeremy Ware100% (2)

- List of Urban SchoolDocument90 pagesList of Urban SchoolAbhi RicNo ratings yet

- Statistical Annex Tables on the International Banking MarketDocument115 pagesStatistical Annex Tables on the International Banking MarketAli HabibNo ratings yet

- BCCPE - Registration FormDocument1 pageBCCPE - Registration Formdineshkumar1009No ratings yet

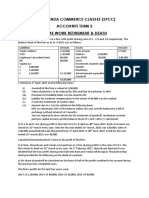

- SPCC Accounts Homework Retirement & DeathDocument3 pagesSPCC Accounts Homework Retirement & DeathBinoy TrevadiaNo ratings yet

- ISRS 4400 Case BookDocument6 pagesISRS 4400 Case BookSaadat AkhundNo ratings yet

- Volume 5 SFMDocument16 pagesVolume 5 SFMrajat sharmaNo ratings yet

- MasterCard GL CompanyDocument2 pagesMasterCard GL CompanyRamneek SinghNo ratings yet