You might also like

- TDS - WorkingDocument13 pagesTDS - WorkingUday tomarNo ratings yet

- CR NotesDocument1 pageCR Notesvivekanantha velappanNo ratings yet

- Economic DevelopmentDocument16 pagesEconomic DevelopmentJake MempinNo ratings yet

- Accounting Standards PDFDocument43 pagesAccounting Standards PDFSai Krishna TejaNo ratings yet

- Ias 21Document13 pagesIas 21f9vertexlearningsolutionsNo ratings yet

- TDS - Working - CA Amit MahajanDocument9 pagesTDS - Working - CA Amit Mahajan42 Rahul RawatNo ratings yet

- Finance For Non-Finance StaffDocument1 pageFinance For Non-Finance Staffyanfong1003No ratings yet

- Another 10 Mark QuestionDocument4 pagesAnother 10 Mark QuestionMyat Htet KoNo ratings yet

- Sources of FinanceDocument8 pagesSources of Financesofiamubarak453No ratings yet

- Ias 38Document14 pagesIas 38Tayyaba RehmanNo ratings yet

- Nism Certification V-A (Mutual Fund) MOck TestDocument36 pagesNism Certification V-A (Mutual Fund) MOck TestAishwarya Adlakha100% (1)

- NJEFA Preliminary Official Statement PDFDocument174 pagesNJEFA Preliminary Official Statement PDFNicholas KerrNo ratings yet

- Cooperatives - PPQDocument22 pagesCooperatives - PPQKerine Williams FigaroNo ratings yet

- CrystallographyDocument1 pageCrystallographySUNANDAN PANDANo ratings yet

- 2021-08-18 Is LM FrameworkDocument9 pages2021-08-18 Is LM FrameworkMansi ParmarNo ratings yet

- Trade - Effects ClifDocument9 pagesTrade - Effects ClifWajiha RajaniNo ratings yet

- FR Revision Day 1 Consolidation-1Document22 pagesFR Revision Day 1 Consolidation-1RENITA FERNANDESNo ratings yet

- Alabi Business PlanDocument17 pagesAlabi Business PlanVicky JeMi100% (2)

- Income Tax Fundamentals 2013 Whittenburg 31st Edition Solutions ManualDocument6 pagesIncome Tax Fundamentals 2013 Whittenburg 31st Edition Solutions Manualbrianbradyogztekbndm100% (48)

- ALBirmingham03b POS PDFDocument437 pagesALBirmingham03b POS PDFSwiert DarasNo ratings yet

- Lessee AccountingDocument7 pagesLessee AccountingYess poooNo ratings yet

- Core Laboratories - Personal Expense Statement: Required Field Expense Type Required FieldDocument3 pagesCore Laboratories - Personal Expense Statement: Required Field Expense Type Required FieldEdwin CastilloNo ratings yet

- Problem Set 3Document7 pagesProblem Set 3Jade BilisNo ratings yet

- Cash Basis Study MaterialDocument12 pagesCash Basis Study MaterialSoheng ReathNo ratings yet

- Handout-And-HomeworkDocument14 pagesHandout-And-Homeworkvedprakash sumanNo ratings yet

- Project Report & CMA Data: S.A.CoconutsDocument15 pagesProject Report & CMA Data: S.A.CoconutsMichael AdonikarNo ratings yet

- Other Financial Assets at Fair ValueDocument1 pageOther Financial Assets at Fair Valuencq6dmzmp4No ratings yet

- Leases Study MaterialDocument37 pagesLeases Study MaterialHammadNo ratings yet

- Untitled Notebook PDFDocument5 pagesUntitled Notebook PDFShehzad QureshiNo ratings yet

- Millan 2 PDF FreeDocument10 pagesMillan 2 PDF FreeMichael Brian TorresNo ratings yet

- Response 13 EPC 2Document4 pagesResponse 13 EPC 2Steven HimawanNo ratings yet

- Financial Statements - RatiosDocument10 pagesFinancial Statements - RatiosHarshit GoyalNo ratings yet

- NJEFA02a POS PDFDocument174 pagesNJEFA02a POS PDFNicholas KerrNo ratings yet

- 2 Ethics - Coram, Cheetah, Bunk - CarterDocument10 pages2 Ethics - Coram, Cheetah, Bunk - Cartersbracca1No ratings yet

- Ias 36Document21 pagesIas 36f9vertexlearningsolutionsNo ratings yet

- Investment SummaryDocument10 pagesInvestment Summary21248deekshakNo ratings yet

- Group Accounts BasicsDocument1 pageGroup Accounts BasicsVaishnavi ChaturvediNo ratings yet

- Liquidation of Cash Advance: Report Date Expense PeriodDocument11 pagesLiquidation of Cash Advance: Report Date Expense PeriodJoyce Anne De Vera RamosNo ratings yet

- F rm.,990-T: Exempt Organization Business Income Tax Return 'Document7 pagesF rm.,990-T: Exempt Organization Business Income Tax Return 'Matias SmithNo ratings yet

- Transaction Cycles Business ProcessesDocument5 pagesTransaction Cycles Business Processeslied27106No ratings yet

- E Nach 4058631816853447162Document1 pageE Nach 4058631816853447162junu raziNo ratings yet

- QA HMS - Expense Claim FormDocument13 pagesQA HMS - Expense Claim Formye min aungNo ratings yet

- 6312 e Civ Idt DC L I 001 - r1 - Idt Station Layout & Details - 13!11!2020 3Document1 page6312 e Civ Idt DC L I 001 - r1 - Idt Station Layout & Details - 13!11!2020 3manikandanNo ratings yet

- Go Dsag s1nb60Document2 pagesGo Dsag s1nb60Muresan SanduNo ratings yet

- Credit TransactionsDocument5 pagesCredit TransactionsDanica ZamoraNo ratings yet

- Unit # 2Document44 pagesUnit # 2Asif FarooqNo ratings yet

- 2023 12 28T100628.773863 - ChequeDocument1 page2023 12 28T100628.773863 - ChequeJohnson WilliamNo ratings yet

- Corporate Finance Cheat SheetDocument1 pageCorporate Finance Cheat SheetbaronfgfNo ratings yet

- Monthly Income & ExpensesDocument7 pagesMonthly Income & ExpensesAj OsborneNo ratings yet

- Thirteen Foundation 2012Document39 pagesThirteen Foundation 2012cmf8926No ratings yet

- Cma Final Old Sylp17 2016sylDocument12 pagesCma Final Old Sylp17 2016sylsankarNo ratings yet

- POA Chap 7Document4 pagesPOA Chap 7Lau Chun GuiNo ratings yet

- 2018 Limited Obligation Bond For Tanger Performing Arts Center in GreensboroDocument236 pages2018 Limited Obligation Bond For Tanger Performing Arts Center in GreensborojeffreyhsykesNo ratings yet

- Ch. 20Document5 pagesCh. 20A JNo ratings yet

- Untitled NotebookDocument3 pagesUntitled Notebookelatalu7No ratings yet

- Cofin - 1Document8 pagesCofin - 1Ana D. ChebacNo ratings yet

- Financing Fintech: YV ALU ATI ONDocument1 pageFinancing Fintech: YV ALU ATI ONcoloradoresourcesNo ratings yet

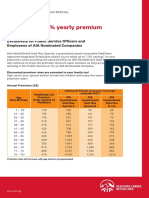

- Enjoy Up To 7.3% Yearly Premium DiscountDocument2 pagesEnjoy Up To 7.3% Yearly Premium DiscountAlvin WangNo ratings yet

- Balance SheetDocument9 pagesBalance SheetShubhrajit MukherjeeNo ratings yet

- Practice Questions A1Document11 pagesPractice Questions A1rishalNo ratings yet

- Now, PLI and RPLI Customers Can Pay Their Premium Online Through Debit/Credit Card, Net Banking, Wallet & UPIDocument1 pageNow, PLI and RPLI Customers Can Pay Their Premium Online Through Debit/Credit Card, Net Banking, Wallet & UPISurya kiranNo ratings yet

- Ias 16 PpeDocument40 pagesIas 16 PpeziyuNo ratings yet

- MI CH 1. The Fundamental of CostingDocument4 pagesMI CH 1. The Fundamental of CostingPonkoj Sarker TutulNo ratings yet

- Long Term Finance: Prepared by Dr. Santosh Solanki Lnct-MbaDocument30 pagesLong Term Finance: Prepared by Dr. Santosh Solanki Lnct-MbaShivamNo ratings yet

- Village Banking: Micro Credit Through Village Development OrganizationsDocument28 pagesVillage Banking: Micro Credit Through Village Development Organizationszeeshan78returntohydNo ratings yet

- 34924bos24617cp5 6Document51 pages34924bos24617cp5 6Piyal HossainNo ratings yet

- FINAL PROJECT SDocument19 pagesFINAL PROJECT SPooja PanjavaniNo ratings yet

- Inflation, Education, and Your ChildDocument10 pagesInflation, Education, and Your ChildAR HemantNo ratings yet

- Npioh, Jurnal Yohana Kretia 41-47Document7 pagesNpioh, Jurnal Yohana Kretia 41-47HasirumanNo ratings yet

- Ms Nthabiseng M Dingaan 2618 Section J Mamelodi West 0122 Dingaanm@Eskom - Co.ZaDocument4 pagesMs Nthabiseng M Dingaan 2618 Section J Mamelodi West 0122 Dingaanm@Eskom - Co.ZaMolly dingaanNo ratings yet

- Northern Province Third Term Examination - 2019 NovemberDocument4 pagesNorthern Province Third Term Examination - 2019 NovemberAshley GazeNo ratings yet

- C2 - Accounting For Cash and RecieviablesDocument69 pagesC2 - Accounting For Cash and RecieviablesHồ ThảoNo ratings yet

- CH 9 Accounting PracticeDocument29 pagesCH 9 Accounting PracticeGernalyn RebanalNo ratings yet

- Application - Loan Overdraft Against DepositDocument5 pagesApplication - Loan Overdraft Against DepositUday Kiran0% (1)

- Chapter 11Document45 pagesChapter 11Nada YoussefNo ratings yet

- Branches in Sarawak: Kuching Laksamana MiriDocument1 pageBranches in Sarawak: Kuching Laksamana MiridomromeoNo ratings yet

- Stock Request Order Rokok MALANG WK 43Document19 pagesStock Request Order Rokok MALANG WK 43Dhika LNo ratings yet

- Chapter 5 - 14thDocument18 pagesChapter 5 - 14thLNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument32 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsAmrita TamangNo ratings yet

- TaxInvoice 01012016Document4 pagesTaxInvoice 01012016Chiong Yew TiongNo ratings yet

- Kuis UTS Genap 21-22 ACCDocument3 pagesKuis UTS Genap 21-22 ACCNatasya FlorenciaNo ratings yet

- Car IjarahDocument5 pagesCar IjarahMuhammad Sadaan ShafiqNo ratings yet

- HjjjejdjsjsDocument1 pageHjjjejdjsjsRey CortesNo ratings yet

- Lesson 1.6 Compound InterestDocument103 pagesLesson 1.6 Compound Interestglenn cardonaNo ratings yet

- Fundamentals of AuditingDocument381 pagesFundamentals of AuditingMiguel CarneiroNo ratings yet

- Unit - 3 Bank Reconciliation StatementDocument21 pagesUnit - 3 Bank Reconciliation StatementMrutyunjay SaramandalNo ratings yet

- PaymentReceipt 1Document2 pagesPaymentReceipt 1hugoiasdNo ratings yet