You might also like

- The Concept and Development of MoneyDocument9 pagesThe Concept and Development of MoneyDorhea Kristha Guian SantosNo ratings yet

- Maths Project: Name: Anshit Gupta Class: X Sec.: A (Commerce) Roll No.: 7Document22 pagesMaths Project: Name: Anshit Gupta Class: X Sec.: A (Commerce) Roll No.: 7Harish GNo ratings yet

- Caie Igcse Economics 0455 Mnemonics v1Document7 pagesCaie Igcse Economics 0455 Mnemonics v1MugiNo ratings yet

- Evolution of Money/ Payments System Payment System: The Method of Conducting Transactions in The Economy. The Payments System Has BeenDocument5 pagesEvolution of Money/ Payments System Payment System: The Method of Conducting Transactions in The Economy. The Payments System Has Beenrabia liaqatNo ratings yet

- MoneyDocument54 pagesMoneyTwinkle MehtaNo ratings yet

- My Content For English ProjectDocument3 pagesMy Content For English ProjectAshutosh RathiNo ratings yet

- What Is Cash?: Legal TenderDocument2 pagesWhat Is Cash?: Legal TenderJonhmark AniñonNo ratings yet

- However, Plastic Money Doesn't Mean The End of Evolution of Money. On The Extreme Ends of Evolution of MoneyDocument2 pagesHowever, Plastic Money Doesn't Mean The End of Evolution of Money. On The Extreme Ends of Evolution of MoneyAditya Vikram SrivastavaNo ratings yet

- The Overview of Money The History of Money: From Barter To BanknotesDocument9 pagesThe Overview of Money The History of Money: From Barter To BanknotesfarahNo ratings yet

- Definition of MoneyDocument4 pagesDefinition of MoneysofiaNo ratings yet

- How Important Is The Environment For Human LifeDocument18 pagesHow Important Is The Environment For Human LifejustanhdungNo ratings yet

- Currency: Barter DeterminedDocument2 pagesCurrency: Barter DeterminedFiantiayu efandiNo ratings yet

- Bet You Thought (Federal Reserve) PDFDocument21 pagesBet You Thought (Federal Reserve) PDFtdon777100% (6)

- Lesson 2 LectureDocument17 pagesLesson 2 LectureQueeny CuraNo ratings yet

- M & B - Lecture 2Document12 pagesM & B - Lecture 2Maria TariqNo ratings yet

- Study On Cash Vs Cashless Indian EconomyDocument91 pagesStudy On Cash Vs Cashless Indian EconomyBhagyashri AhireNo ratings yet

- Evolution of MoneyDocument21 pagesEvolution of MoneyKunal100% (1)

- The Origins of MoneyDocument10 pagesThe Origins of MoneyAgostinho Figurao ChihungueteNo ratings yet

- Plastic MoneyDocument76 pagesPlastic MoneyMukesh ManwaniNo ratings yet

- Group Name Id: A Resarch Proposal Sumitted To Accounting and Finance DepartmentDocument12 pagesGroup Name Id: A Resarch Proposal Sumitted To Accounting and Finance DepartmentMIKIYAS BERHENo ratings yet

- Senior High School: First Semester S.Y. 2020-2021Document9 pagesSenior High School: First Semester S.Y. 2020-2021sheilame nudaloNo ratings yet

- Money and Its EvolutionDocument7 pagesMoney and Its EvolutionCANDA Jennyrose A.No ratings yet

- Raja ChequeDocument6 pagesRaja ChequeMadan VennapusaNo ratings yet

- I. History of Currency Formation: 2.the Transition From Bartering To CurrencyDocument6 pagesI. History of Currency Formation: 2.the Transition From Bartering To CurrencyQuang SọtNo ratings yet

- In The Early Days of CommerceDocument2 pagesIn The Early Days of Commercepitad21.marquezgeraldineNo ratings yet

- Evolution of Payment Transaction MethodsDocument11 pagesEvolution of Payment Transaction MethodsKirubashini S TTGI190112No ratings yet

- Types of MoneyDocument3 pagesTypes of MoneyMilan MinSunNo ratings yet

- Evolution of CurrenciesDocument4 pagesEvolution of CurrenciesViswa KNo ratings yet

- Project WorkDocument51 pagesProject Workvishal galaNo ratings yet

- The Nature and Types of MoneyDocument12 pagesThe Nature and Types of MoneyShiraz KhanNo ratings yet

- Breif Introduction To MoneyDocument8 pagesBreif Introduction To MoneyAbdul SattarNo ratings yet

- Modern MoneyDocument7 pagesModern Moneyjulia1212marshmellowNo ratings yet

- MoneyDocument6 pagesMoneyMD. IBRAHIM KHOLILULLAHNo ratings yet

- Reading Lesson 10Document25 pagesReading Lesson 10AnshumanNo ratings yet

- The Evolution of MoneyDocument7 pagesThe Evolution of MoneyHà Nhi LêNo ratings yet

- Money and BankingDocument12 pagesMoney and Bankingndagarachel015No ratings yet

- Money: Dr. Mary Joy Catipay - Teodosio, LPTDocument57 pagesMoney: Dr. Mary Joy Catipay - Teodosio, LPTalleah tapilNo ratings yet

- 551 ArticleText 1967 1 10 20180615Document23 pages551 ArticleText 1967 1 10 20180615Tran DatNo ratings yet

- Introduction To Money: Inconveniences (Problems) of Barter ExchangeDocument30 pagesIntroduction To Money: Inconveniences (Problems) of Barter ExchangeMahendra Kumar B RNo ratings yet

- Collectivize The Debt Liability Against All Citizens of The Country. Banks Allegedly Evaluate The Risk Involved in EachDocument1 pageCollectivize The Debt Liability Against All Citizens of The Country. Banks Allegedly Evaluate The Risk Involved in Eachforo35No ratings yet

- Role of MoneyDocument13 pagesRole of MoneyShri SpammerNo ratings yet

- Money CreationDocument7 pagesMoney CreationTrifan_DumitruNo ratings yet

- F19BB023 ECON231 Assignment 2Document4 pagesF19BB023 ECON231 Assignment 2Mehreen M AhmadNo ratings yet

- Evolution of Currency: Isha Suhail - 2015-ARCH-05 Amna Kazmi - 2015-ARCH-12 Aqsa Shafique - 2015-ARCH-21Document27 pagesEvolution of Currency: Isha Suhail - 2015-ARCH-05 Amna Kazmi - 2015-ARCH-12 Aqsa Shafique - 2015-ARCH-21Isha ChaudhryNo ratings yet

- 3104 Lesson Plan MoneyDocument77 pages3104 Lesson Plan Moneymahin.ahmed.bd3No ratings yet

- 4 Essential Functions of MoneyDocument19 pages4 Essential Functions of MoneyNehaNo ratings yet

- Eco PDFDocument4 pagesEco PDFyksamy23No ratings yet

- Money and Finance IGCSE ECONOMICS Notes 2020Document3 pagesMoney and Finance IGCSE ECONOMICS Notes 2020TYDK MediaNo ratings yet

- MoneyDocument9 pagesMoneyShayan ChatterjeeNo ratings yet

- Everything You need to Know About Central Bank Digital CurrencyFrom EverandEverything You need to Know About Central Bank Digital CurrencyNo ratings yet

- Plastic MoneyDocument60 pagesPlastic Moneyahmad7920005675100% (1)

- Absurd Monetary SystemDocument3 pagesAbsurd Monetary SystemMubashir HassanNo ratings yet

- Modern Money Mechanics: A Workbook On Bank Reserves and Deposit ExpansionDocument14 pagesModern Money Mechanics: A Workbook On Bank Reserves and Deposit Expansionjethro gibbins100% (2)

- Money Supply: Submitted byDocument15 pagesMoney Supply: Submitted byPrasad GantiNo ratings yet

- Module 2 MoneyDocument78 pagesModule 2 Moneylord kwantoniumNo ratings yet

- Blockchain: An Essential Beginner’s Guide to Understanding Blockchain Technology, Cryptocurrencies, Bitcoin and the Future of MoneyFrom EverandBlockchain: An Essential Beginner’s Guide to Understanding Blockchain Technology, Cryptocurrencies, Bitcoin and the Future of MoneyNo ratings yet

- Overview of MoneyDocument2 pagesOverview of Moneyforo35No ratings yet

- Roshan Project - Roshan GhodeDocument58 pagesRoshan Project - Roshan Ghodedipak tighareNo ratings yet

- Project - Evolution of Money - From Commodities To E-MoneyDocument10 pagesProject - Evolution of Money - From Commodities To E-MoneyENTITYPLAYZZNo ratings yet

- Cryptocurrencies and Blockchain 101:: From Bitcoin to NFTs: Learn Everything About the Metaverse and Get Ready to Be Part of the Crypto RevolutionFrom EverandCryptocurrencies and Blockchain 101:: From Bitcoin to NFTs: Learn Everything About the Metaverse and Get Ready to Be Part of the Crypto RevolutionNo ratings yet

- Evalution of MoneyDocument3 pagesEvalution of MoneyPrincess GeminiNo ratings yet

- Fintech in Africa 1675424459Document207 pagesFintech in Africa 1675424459Serge Kanga100% (1)

- Logistics and DistributionDocument34 pagesLogistics and DistributionAgnihotri VikasNo ratings yet

- Chapter 05 - Accounting For Merchaindising OperationsDocument79 pagesChapter 05 - Accounting For Merchaindising OperationsMinh NguyệtNo ratings yet

- 5th Year DesertationDocument16 pages5th Year DesertationghNo ratings yet

- Social Studies Sample Scope and Sequence Updated - Grade 6 PDFDocument287 pagesSocial Studies Sample Scope and Sequence Updated - Grade 6 PDFJC Zapata67% (3)

- Introduction To Global Finance With Electronic 1 BankingDocument4 pagesIntroduction To Global Finance With Electronic 1 Bankingcharlenealvarez59No ratings yet

- Comparative Advantage TheoryDocument10 pagesComparative Advantage Theorydevam chandraNo ratings yet

- Internship Report Mastercopy-1111Document52 pagesInternship Report Mastercopy-1111Nishant GauravNo ratings yet

- ROZY MAM If & MarketingDocument41 pagesROZY MAM If & Marketingraj rmnNo ratings yet

- Interest Rates SummaryDocument28 pagesInterest Rates SummaryMichael ArevaloNo ratings yet

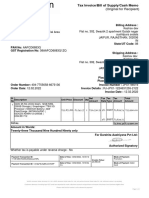

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)erjasdNo ratings yet

- Senate Bill 2968 - Customs Modernization and Tariff ActDocument157 pagesSenate Bill 2968 - Customs Modernization and Tariff ActPortCallsNo ratings yet

- Abm 1 - Module Part 1Document7 pagesAbm 1 - Module Part 1Alvin Ryan CaballeroNo ratings yet

- Cms INVM2 K230001117Document3 pagesCms INVM2 K230001117jatinyaduvanshi57No ratings yet

- To Indian Financial System: Courses Offered: Rbi Grade B Sebi Grade A Nabard Grade A and B Ugc Net Paper 1 and 2Document12 pagesTo Indian Financial System: Courses Offered: Rbi Grade B Sebi Grade A Nabard Grade A and B Ugc Net Paper 1 and 2Aishwarya SharmaNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Gadgets GuruNo ratings yet

- Money, Output and Inflation in Classical Economics : Roy. GreenDocument27 pagesMoney, Output and Inflation in Classical Economics : Roy. GreenBruno DuarteNo ratings yet

- 3RD Term SS2 Economics Note For StudentsDocument36 pages3RD Term SS2 Economics Note For StudentsinyamahchinonsoNo ratings yet

- Class-X-Study-Material SST PDFDocument95 pagesClass-X-Study-Material SST PDFPrasant Kumar SahooNo ratings yet

- Incoterms Changes 2000 Vs 2010Document5 pagesIncoterms Changes 2000 Vs 2010Shanti Prakhar AwasthiNo ratings yet

- Sales Attachment 2Document10 pagesSales Attachment 2hamrawikebedeNo ratings yet

- Solana Airdrop Guide 3 in 1Document6 pagesSolana Airdrop Guide 3 in 1Ion TataruNo ratings yet

- Ibm 1Document172 pagesIbm 1Sarika PatilNo ratings yet

- Unit 5 - Business CorrespondenceDocument29 pagesUnit 5 - Business CorrespondenceTang TeacherNo ratings yet

- Commercial Invoice FINALDocument1 pageCommercial Invoice FINALWalter A. MarinNo ratings yet

- Week 6 Self AssessmentDocument13 pagesWeek 6 Self AssessmentDaniel NikiemaNo ratings yet

- Intern Part 1Document11 pagesIntern Part 1Mrinal DasNo ratings yet

- Cambridge International AS & A Level: Economics 9708/22Document21 pagesCambridge International AS & A Level: Economics 9708/22kitszimbabweNo ratings yet