You might also like

- Aus Allergens SummaryDocument2 pagesAus Allergens SummaryDion LamontNo ratings yet

- India Dairy Industry Snapshot Apr Jun 2020Document10 pagesIndia Dairy Industry Snapshot Apr Jun 2020NAVYASHREE B 1NC21BA050No ratings yet

- Daily Diet JournalDownloadable ProofDocument52 pagesDaily Diet JournalDownloadable ProofMohamed labibiNo ratings yet

- Dairy Sept 09 ReportDocument140 pagesDairy Sept 09 ReportmahigaduNo ratings yet

- Feed Formulas For Dairy Animals - LivestockingDocument15 pagesFeed Formulas For Dairy Animals - LivestockingAbbasali AshariyaNo ratings yet

- Khudahuspe PDFDocument16 pagesKhudahuspe PDFmehek mishraNo ratings yet

- Dairy Market Report July 2020Document5 pagesDairy Market Report July 2020Brittany EtheridgeNo ratings yet

- Pricing of Milk by State GovernmentDocument8 pagesPricing of Milk by State Governmentarpit85No ratings yet

- SAP Solutions For The: Dairy, Meat & Fish IndustryDocument29 pagesSAP Solutions For The: Dairy, Meat & Fish IndustryAlexey MalakhovNo ratings yet

- Dairy Market: Commercial Use of Dairy ProductsDocument5 pagesDairy Market: Commercial Use of Dairy ProductsBrittany EtheridgeNo ratings yet

- Grain and Feed Annual - Kuala Lumpur - Malaysia - MY2023-0001Document14 pagesGrain and Feed Annual - Kuala Lumpur - Malaysia - MY2023-0001Chin YeeNo ratings yet

- Suguna Group - HRDocument26 pagesSuguna Group - HRsri lakshmiNo ratings yet

- BulletinFeb2015 DraftDocument57 pagesBulletinFeb2015 Draftsakshi maheshwariNo ratings yet

- Q3 2022 Livestocks StatsDocument1 pageQ3 2022 Livestocks StatsjcNo ratings yet

- Gem Jeleu MarmeladaDocument15 pagesGem Jeleu Marmeladadorinutza280No ratings yet

- Case StudymilkDocument3 pagesCase StudymilkSunil GamageNo ratings yet

- The Six Food Exchange List For Meal DesignDocument6 pagesThe Six Food Exchange List For Meal DesignKhaled SalehNo ratings yet

- Milk DataDocument3 pagesMilk Dataniravjadav28No ratings yet

- Dairy Industry-CorporateDocument2 pagesDairy Industry-CorporateAta AlahiNo ratings yet

- Chapter 7. Dairy and Dairy ProductsDocument10 pagesChapter 7. Dairy and Dairy ProductsAryan KothotyaNo ratings yet

- Factors Effecting Quality of ButterDocument4 pagesFactors Effecting Quality of ButtermohsinNo ratings yet

- Godrej Agrovet: Agri Behemoth in The MakingDocument38 pagesGodrej Agrovet: Agri Behemoth in The MakingADNo ratings yet

- Godrej Agrovet: Agri Behemoth in The MakingDocument38 pagesGodrej Agrovet: Agri Behemoth in The MakingADNo ratings yet

- Global Poultry Production and Market Outlook 2030Document37 pagesGlobal Poultry Production and Market Outlook 2030Reffiadi saputra kahfiNo ratings yet

- Paneer WriteupDocument34 pagesPaneer Writeuprajuhardware04No ratings yet

- Usual Levels of Various Feedstuffs in Swine RationsDocument4 pagesUsual Levels of Various Feedstuffs in Swine Rationshelbert medrosoNo ratings yet

- Dairy Market Report - September 2021Document5 pagesDairy Market Report - September 2021Brittany EtheridgeNo ratings yet

- Should Amul Diversify To Plant Based Products ?Document15 pagesShould Amul Diversify To Plant Based Products ?Himadri JanaNo ratings yet

- Brochure Vitavance WebDocument11 pagesBrochure Vitavance WebLim Chee SiangNo ratings yet

- Amul Cattle FeedDocument15 pagesAmul Cattle Feedgaurang0% (1)

- Estimated Costs of Crop Production in Iowa-2023: Ag Decision MakerDocument13 pagesEstimated Costs of Crop Production in Iowa-2023: Ag Decision Makeramberhahn571No ratings yet

- AgricultureDocument1 pageAgriculturejekow26815No ratings yet

- Schematic Diagram of Production Process of Bioethanol, Gluten and CdsDocument1 pageSchematic Diagram of Production Process of Bioethanol, Gluten and CdsMuhammad NomanNo ratings yet

- Indian Dairy IndustryDocument11 pagesIndian Dairy IndustryRibhanshu RajNo ratings yet

- Zenitro Kemin Research PaperDocument6 pagesZenitro Kemin Research PaperSUBRATA PARAINo ratings yet

- 1544421906GIM Opportunities For Investmentr in Food Processing in TNDocument28 pages1544421906GIM Opportunities For Investmentr in Food Processing in TNGokulNo ratings yet

- Indian Dairy Industry - Driven by Value-Added ProductsDocument15 pagesIndian Dairy Industry - Driven by Value-Added ProductsyatharthNo ratings yet

- MSP Complete Concept 2022Document7 pagesMSP Complete Concept 2022Babariya DigvijayNo ratings yet

- Present Status and Future Prospects For Dairying, Compound Feed and Feed Additives in IndiaDocument17 pagesPresent Status and Future Prospects For Dairying, Compound Feed and Feed Additives in IndiaAbhishek SharmaNo ratings yet

- Investment Opportunities in The Ethiopian Dairy Sector TRAIDE EthiopiaDocument24 pagesInvestment Opportunities in The Ethiopian Dairy Sector TRAIDE EthiopiaYiftusira DesalegnNo ratings yet

- NDDB Ar 2019 English 24022020 - 2 PDFDocument98 pagesNDDB Ar 2019 English 24022020 - 2 PDFAsanga KumarNo ratings yet

- Hassan Union Marketing Plan - 15dec19Document14 pagesHassan Union Marketing Plan - 15dec19Pankaj SinghNo ratings yet

- Food & Allied: Poultry Feed IndustryDocument14 pagesFood & Allied: Poultry Feed IndustryUmer FarooqNo ratings yet

- 82 The Gazette of India: Extraordinary (P Iii-S - 4) : ART ECDocument3 pages82 The Gazette of India: Extraordinary (P Iii-S - 4) : ART ECchiranjevi rajaNo ratings yet

- Annual Report - 0 - Part00002Document2 pagesAnnual Report - 0 - Part00002siva kumarNo ratings yet

- Milk CompositionDocument4 pagesMilk CompositionNaaggaaNo ratings yet

- Shimul and Eeshwar TradersDocument80 pagesShimul and Eeshwar TradersPrajwal HiremathNo ratings yet

- Beef Fattening Decision Support SystemDocument7 pagesBeef Fattening Decision Support SystemSaipolNo ratings yet

- Starch Sector Report - AASPL - 23-07-10Document15 pagesStarch Sector Report - AASPL - 23-07-10DFrancis007No ratings yet

- IntroductionDocument28 pagesIntroductionNitin PatidarNo ratings yet

- Jasons PDF RemediatedDocument4 pagesJasons PDF Remediatedsalah.rekani542No ratings yet

- Dairy ReportDocument6 pagesDairy ReportthehedonistNo ratings yet

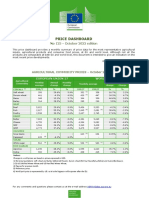

- Commodity Price Dashboard 2022 11 enDocument9 pagesCommodity Price Dashboard 2022 11 enoscarNo ratings yet

- PPA 2 - Carbohydrate-III (Pengetahuan Produk Agroindustri)Document53 pagesPPA 2 - Carbohydrate-III (Pengetahuan Produk Agroindustri)ItsAndrioNo ratings yet

- Bhutan Food InformationDocument113 pagesBhutan Food InformationAna OrriolsNo ratings yet

- Gazette & Draft Regulations For R&D TeamDocument4 pagesGazette & Draft Regulations For R&D Teamsushant deyNo ratings yet

- Poultry Feed - PACRA Research - January'23 - 1674655244Document23 pagesPoultry Feed - PACRA Research - January'23 - 1674655244Ali ArsalanNo ratings yet

- Dairy Blends A5Document16 pagesDairy Blends A5Kadiwala Dairy FarmNo ratings yet

- Starch & Vegetable Fats & Oils World Summary: Market Values & Financials by CountryFrom EverandStarch & Vegetable Fats & Oils World Summary: Market Values & Financials by CountryNo ratings yet

- Augmentation of Productivity of Micro or Small Goat Entrepreneurship through Adaptation of Sustainable Practices and Advanced Marketing Management Strategies to Double the Farmer’s IncomeFrom EverandAugmentation of Productivity of Micro or Small Goat Entrepreneurship through Adaptation of Sustainable Practices and Advanced Marketing Management Strategies to Double the Farmer’s IncomeNo ratings yet

- Thesis Manuscript 11 PDFDocument69 pagesThesis Manuscript 11 PDFLorenz San DiegoNo ratings yet

- Pe 1 Lesson 3 NutritionDocument95 pagesPe 1 Lesson 3 Nutritiondario serranoNo ratings yet

- Student Summative Assessment Creation Grade: 4 Topic: Where Do I Live? Habitats, Food Chains, and Food WebsDocument11 pagesStudent Summative Assessment Creation Grade: 4 Topic: Where Do I Live? Habitats, Food Chains, and Food WebsJopher Dominguez Delos SantosNo ratings yet

- An Open Letter To The Honorable Senators of The Philippine SenateDocument4 pagesAn Open Letter To The Honorable Senators of The Philippine SenateJhannz SimNo ratings yet

- Building A Performance Plate WebDocument2 pagesBuilding A Performance Plate Webapi-266990480No ratings yet

- Fast Food Consumption of U.S. Adults: Impact On Energy and Nutrient Intakes and Overweight StatusDocument7 pagesFast Food Consumption of U.S. Adults: Impact On Energy and Nutrient Intakes and Overweight StatusSamiul AlamNo ratings yet

- Sahaja - Aharam Producer CompanyDocument28 pagesSahaja - Aharam Producer CompanySri HimajaNo ratings yet

- Migraine - More Than A HeadacheDocument11 pagesMigraine - More Than A HeadacheLuma De Fátima Louro AitaNo ratings yet

- Eat Fit - Burn More Fat (Issue 13) (2015) PDFDocument124 pagesEat Fit - Burn More Fat (Issue 13) (2015) PDFsalem100% (1)

- Project Report PMDocument75 pagesProject Report PMMurtaza ramzanNo ratings yet

- Effective Workflow in KitchenDocument2 pagesEffective Workflow in KitchenMa Hdi Choudhury60% (5)

- Lebanese CuisineDocument300 pagesLebanese Cuisinejuancgr77100% (3)

- Assignment 2 2020PGP054 SohamDocument2 pagesAssignment 2 2020PGP054 SohamSoham ChaudhuriNo ratings yet

- Breville JE95XL ManualDocument58 pagesBreville JE95XL ManualBrevilleNo ratings yet

- G8 Lesson 2.1Document35 pagesG8 Lesson 2.1Ima blinkNo ratings yet

- Methodological Recommendations For Summative Assessment On The Subject The English Language Grade 10Document39 pagesMethodological Recommendations For Summative Assessment On The Subject The English Language Grade 10Saranyn anasyNo ratings yet

- Colon Cancer Care PlanDocument4 pagesColon Cancer Care PlanTony Festa100% (3)

- Sales and Marketing Job DescriptionDocument1 pageSales and Marketing Job DescriptionMichael448No ratings yet

- Does China S Going Out Strategy Prefigure A New Food RegimeDocument40 pagesDoes China S Going Out Strategy Prefigure A New Food RegimeAgostina CostantinoNo ratings yet

- Intermittent FastingDocument1 pageIntermittent FastingAsyraf Fatullah0% (1)

- Electric Pressure Cooker: EN FR ESDocument28 pagesElectric Pressure Cooker: EN FR ESalexandra130409No ratings yet

- Ral BrandingDocument26 pagesRal BrandingkhushiYNo ratings yet

- Cattle Pen Fattening Business Project Proposal: Promoter: - Beruf Fattening PLCDocument39 pagesCattle Pen Fattening Business Project Proposal: Promoter: - Beruf Fattening PLCDereje Abera90% (39)

- MET - Grammar - Reading 24-03-19Document11 pagesMET - Grammar - Reading 24-03-19Rafael Rodriguez LopezNo ratings yet

- Chapter One 1.1 History of SiwesDocument19 pagesChapter One 1.1 History of SiwesOpeyemi JamalNo ratings yet

- BRC Global Standard For Packaging MaterialDocument16 pagesBRC Global Standard For Packaging MaterialflathonNo ratings yet

- Policies Pursued by The Government of Zimbabwe in Terms of Agricultural Input Supply To Farmers.Document6 pagesPolicies Pursued by The Government of Zimbabwe in Terms of Agricultural Input Supply To Farmers.Wellington BandasonNo ratings yet

- Chinese Empire Ill 00 AlloDocument370 pagesChinese Empire Ill 00 AlloMillitte WalkerNo ratings yet

- PE - Q3 PPT MAPEH10 - Lesson 1Document15 pagesPE - Q3 PPT MAPEH10 - Lesson 1Ocib LuenNo ratings yet

- Fortified Instant Noodle SpecsDocument4 pagesFortified Instant Noodle Specsnietz2No ratings yet