You might also like

- FAR Midterm ReviewerDocument4 pagesFAR Midterm ReviewerCresel ReposoNo ratings yet

- Accounting ReviewerDocument7 pagesAccounting ReviewerAdrian PeñafielNo ratings yet

- ACC406 - Chapter 1Document14 pagesACC406 - Chapter 1Carol LeslyNo ratings yet

- FAR Midterm Reviewer1Document4 pagesFAR Midterm Reviewer1Cresel ReposoNo ratings yet

- Module1 Introduction To AcctgDocument20 pagesModule1 Introduction To AcctgRian Hanz AlbercaNo ratings yet

- ACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneDocument33 pagesACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneGabriel L. CaringalNo ratings yet

- Elements of Financial StatementDocument33 pagesElements of Financial StatementKertik Singh100% (1)

- Midterm Exam (Reviewer)Document84 pagesMidterm Exam (Reviewer)Mj PamintuanNo ratings yet

- Chapter 1 Introduction To AcctgDocument11 pagesChapter 1 Introduction To AcctgNUR ANIS SYAMIMI BINTI MUSTAFA / UPMNo ratings yet

- ACC106 Chapter 1Document20 pagesACC106 Chapter 1ErynNo ratings yet

- BBAW2103 Topic 1Document30 pagesBBAW2103 Topic 1MOHD SYUKRI BIN ABDUL WAHAB STUDENTNo ratings yet

- MODULE 1 NotesDocument3 pagesMODULE 1 NotesJoshua AlvarezNo ratings yet

- (Lesson 1 P2) Importance of Accounting in BusinessDocument2 pages(Lesson 1 P2) Importance of Accounting in BusinessNEIL OBINARIONo ratings yet

- Slide of Session 1-2Document32 pagesSlide of Session 1-2tranhlthNo ratings yet

- Internal External: Prepared by M.T. SacramedDocument2 pagesInternal External: Prepared by M.T. SacramedLawrence CasullaNo ratings yet

- 1.1 Nature and Purpose of AccountsDocument12 pages1.1 Nature and Purpose of AccountsJustin MarshallNo ratings yet

- Fundamentals of AccountingDocument26 pagesFundamentals of AccountingSofia Naraine OnilongoNo ratings yet

- Introduction To Financial Accounting-Unit 1-1Document57 pagesIntroduction To Financial Accounting-Unit 1-1B-ton LimbeNo ratings yet

- Chapter 1-Introduction To Financial Accounting (Acc106)Document17 pagesChapter 1-Introduction To Financial Accounting (Acc106)Syahirah AzlyzanNo ratings yet

- Accounting and Its Environment - PowerPoint PresentationDocument30 pagesAccounting and Its Environment - PowerPoint PresentationBhea G. ManaloNo ratings yet

- Fundamentals of Accountancy Business and ManagementDocument7 pagesFundamentals of Accountancy Business and ManagementhansoNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- Introduction To Accounting: Caec 1 & 2: Financial Accounting and ReportingDocument6 pagesIntroduction To Accounting: Caec 1 & 2: Financial Accounting and ReportingKlucifer XinNo ratings yet

- Accounting 1Document3 pagesAccounting 1Carmina Dongcayan100% (1)

- CFAS Reviewer Ch. 1 5Document3 pagesCFAS Reviewer Ch. 1 5Precious AnneNo ratings yet

- Note 1-Government AccountingDocument5 pagesNote 1-Government AccountingAngelica RubiosNo ratings yet

- Accounting ReviewerDocument30 pagesAccounting ReviewerCheesy MacNo ratings yet

- Basic AccountingDocument15 pagesBasic AccountingShellalyn RigonNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- Funac Final Handouts 1 PDFDocument3 pagesFunac Final Handouts 1 PDFAubrey SalvadorNo ratings yet

- A1 NotesDocument43 pagesA1 NotesAndrea ReyesNo ratings yet

- CHAPTER 1 (Lecture Notes)Document20 pagesCHAPTER 1 (Lecture Notes)Nor Farhanah NanaNo ratings yet

- Far AssignmentDocument5 pagesFar AssignmentMy everyday LifeeeNo ratings yet

- LS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Document53 pagesLS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Danielle Angel Malana100% (1)

- Cfas NotesDocument3 pagesCfas NotesUyara LeisbergNo ratings yet

- Accounting and BookkeepingDocument2 pagesAccounting and BookkeepingClaire PintorNo ratings yet

- Finalized Mod 1&2 ReviewerDocument4 pagesFinalized Mod 1&2 ReviewerJoshua AlvarezNo ratings yet

- AD1101 AY15 - 16 Sem 1 Lecture 1Document21 pagesAD1101 AY15 - 16 Sem 1 Lecture 1weeeeeshNo ratings yet

- ACC 106 Chapter 1Document13 pagesACC 106 Chapter 1Firdaus Yahaya100% (4)

- Financial Accounting and ReportingDocument9 pagesFinancial Accounting and ReportingVipul 663No ratings yet

- CHAPTER 1 and 2 Overview and Concepts in AccountingDocument15 pagesCHAPTER 1 and 2 Overview and Concepts in AccountingVin FajardoNo ratings yet

- Financial Accounting: Acctg. 1Document19 pagesFinancial Accounting: Acctg. 1charie santosNo ratings yet

- Corporation: Meaning of BusinessDocument16 pagesCorporation: Meaning of BusinessAngelica ManahanNo ratings yet

- Entrep Group 9Document124 pagesEntrep Group 9Elizabeth VillarealNo ratings yet

- Fabm 2 PDFDocument3 pagesFabm 2 PDFgk concepcionNo ratings yet

- Good Gov ReviewerrrDocument12 pagesGood Gov ReviewerrrAlyssa GalivoNo ratings yet

- REVIEWERDocument12 pagesREVIEWEREva Mae LabardaNo ratings yet

- 18 AIS 012 (MD Jubayed Hossen)Document9 pages18 AIS 012 (MD Jubayed Hossen)Md JubayedNo ratings yet

- Session 1 With NotesDocument36 pagesSession 1 With NotesAhmad Ridwan FauziNo ratings yet

- Accounting in ActionDocument31 pagesAccounting in ActionTasim IshraqueNo ratings yet

- FM FinalsDocument8 pagesFM FinalsShane VelascoNo ratings yet

- I. Ms Concepts, Practices and Standards II. Cost Concepts and Classifications Iii. Financial Statement AnalysisDocument6 pagesI. Ms Concepts, Practices and Standards II. Cost Concepts and Classifications Iii. Financial Statement AnalysisDensNo ratings yet

- MBA 2021 - Pre-LOB - Sessions 1 and 2Document42 pagesMBA 2021 - Pre-LOB - Sessions 1 and 2martinNo ratings yet

- Accounting 01Document9 pagesAccounting 01reagan blaireNo ratings yet

- Introduction To Financial AccountingDocument30 pagesIntroduction To Financial AccountingSaad SulemanNo ratings yet

- Conceptual FrameworkDocument13 pagesConceptual FrameworkKate Louie RamasNo ratings yet

- Recording Classifying Summarizing: Sole ProprietorshipDocument6 pagesRecording Classifying Summarizing: Sole ProprietorshipLenmariel GallegoNo ratings yet

- Accounting EnvironmentDocument6 pagesAccounting EnvironmentdinishiappuhamyNo ratings yet

- Financial Accounting Valix Summary 1-7Document13 pagesFinancial Accounting Valix Summary 1-7Noel Guerra94% (65)

- Assignment in Partnership Operations (1)Document4 pagesAssignment in Partnership Operations (1)caraaatbongNo ratings yet

- Enhancing Procurement Strategies For Resolving Agency Issues in ClientDocument6 pagesEnhancing Procurement Strategies For Resolving Agency Issues in ClientcaraaatbongNo ratings yet

- Finals Reviewer DevpsychDocument15 pagesFinals Reviewer DevpsychcaraaatbongNo ratings yet

- Reviewer in Business FinanceDocument2 pagesReviewer in Business FinancecaraaatbongNo ratings yet

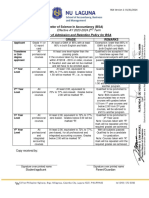

- NU Laguna BSA Admission and Retention Policy Revised 02152024Document1 pageNU Laguna BSA Admission and Retention Policy Revised 02152024caraaatbongNo ratings yet

- POCHEBSA231CDocument1 pagePOCHEBSA231CcaraaatbongNo ratings yet

- NSTP 1 ReviewerDocument6 pagesNSTP 1 ReviewercaraaatbongNo ratings yet

- Jemina InsightsDocument1 pageJemina InsightscaraaatbongNo ratings yet

- The Contemporary World ReviewerDocument4 pagesThe Contemporary World ReviewercaraaatbongNo ratings yet

- Giants of DawleyDocument94 pagesGiants of DawleytoobaziNo ratings yet

- Enterprise Risk ManagementDocument12 pagesEnterprise Risk ManagementAnoop Chaudhary67% (3)

- Oregon Drivers Manual - Oregon Drivers HandbookDocument128 pagesOregon Drivers Manual - Oregon Drivers HandbookpermittestNo ratings yet

- Philippine Health Care Providers, Inc. Vs CIR Case DigestDocument2 pagesPhilippine Health Care Providers, Inc. Vs CIR Case DigestJet jet NuevaNo ratings yet

- Jawaban Kieso Intermediate Accounting p19-4Document3 pagesJawaban Kieso Intermediate Accounting p19-4nadiaulyNo ratings yet

- Facebook Expose Part 1 of WitnessesDocument5 pagesFacebook Expose Part 1 of WitnessesByronHubbardNo ratings yet

- GE 103 Lecture 4Document13 pagesGE 103 Lecture 4aljonNo ratings yet

- Health Records and The Law 5th EditionDocument436 pagesHealth Records and The Law 5th Editionprasad sardarNo ratings yet

- CSI Effect PaperDocument6 pagesCSI Effect PaperDanelya ShaikenovaNo ratings yet

- POS Retail User GuideDocument61 pagesPOS Retail User GuideDigitalpay DepartmentNo ratings yet

- Medical Malpractice Claim FormDocument2 pagesMedical Malpractice Claim Formq747cxmgc8No ratings yet

- Ratio AnalysisDocument36 pagesRatio AnalysisHARVENDRA9022 SINGHNo ratings yet

- Declaration of Ruth Stoner Muzzin 2-08-17Document75 pagesDeclaration of Ruth Stoner Muzzin 2-08-17L. A. PatersonNo ratings yet

- APHYD00136810000170072 NewDocument3 pagesAPHYD00136810000170072 NewNithin Sunny ChackoNo ratings yet

- WCL8 (Assembly)Document1 pageWCL8 (Assembly)Md.Bellal HossainNo ratings yet

- Samyu AgreementDocument16 pagesSamyu AgreementMEENA VEERIAHNo ratings yet

- Important Notice For Passengers Travelling To and From IndiaDocument3 pagesImportant Notice For Passengers Travelling To and From IndiaGokul RajNo ratings yet

- The UCC and The IRSDocument14 pagesThe UCC and The IRSjsands51100% (2)

- Tabang vs. National Labor Relations CommissionDocument6 pagesTabang vs. National Labor Relations CommissionRMC PropertyLawNo ratings yet

- Vasquez Vs CADocument8 pagesVasquez Vs CABerNo ratings yet

- Vocabulary Quiz 5 Group ADocument1 pageVocabulary Quiz 5 Group Aanna barchukNo ratings yet

- Copyreading and Headline Writing Exercise 2 KeyDocument2 pagesCopyreading and Headline Writing Exercise 2 KeyPaul Marcine C. DayogNo ratings yet

- Mongodb Use Case GuidanceDocument25 pagesMongodb Use Case Guidancecresnera01No ratings yet

- Downloads - Azure Data Services - Módulo 2Document11 pagesDownloads - Azure Data Services - Módulo 2hzumarragaNo ratings yet

- Ise II Writing A Formal Letter OfaDocument1 pageIse II Writing A Formal Letter OfaCristina ParraNo ratings yet

- Vikrant SinghDocument3 pagesVikrant SinghUtkarshNo ratings yet

- Solved Problems in Compound InterestDocument3 pagesSolved Problems in Compound Interestjaine ylevreb100% (1)

- Deed of Real Estate MortgageDocument6 pagesDeed of Real Estate MortgageCristopher ReyesNo ratings yet

- Crb84a5dddid2474989 BorrowerDocument13 pagesCrb84a5dddid2474989 BorrowerKaran SharmaNo ratings yet

- Informal Market and Work Decent 212689Document507 pagesInformal Market and Work Decent 212689Lenin Dos Santos PiresNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 5 out of 5 stars5/5 (13)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditFrom EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditRating: 5 out of 5 stars5/5 (1)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)