You might also like

- An Empirical Analysis of Financial Risk Tolerance and Demographic Factors of Business Graduates in PakistanDocument16 pagesAn Empirical Analysis of Financial Risk Tolerance and Demographic Factors of Business Graduates in PakistanMuhammad Asad KhanNo ratings yet

- Muhammad Saeed Iqbal P (104-132)Document29 pagesMuhammad Saeed Iqbal P (104-132)International Journal of Management Research and Emerging SciencesNo ratings yet

- Introducing The Overall Risk Scoring As An Early Warning SystemDocument10 pagesIntroducing The Overall Risk Scoring As An Early Warning SystemNirvana CélesteNo ratings yet

- Literature Review of Risk Management in Indian BanksDocument4 pagesLiterature Review of Risk Management in Indian BanksafmzzbfdgoupjxNo ratings yet

- Awareness and Perception of Investors To PDFDocument14 pagesAwareness and Perception of Investors To PDFakshayNo ratings yet

- Integrity Risks and Red Flags in Agriculture, Natural Resources, and Rural Development ProjectsFrom EverandIntegrity Risks and Red Flags in Agriculture, Natural Resources, and Rural Development ProjectsNo ratings yet

- The Enabling Environment for Disaster Risk Financing in Pakistan: Country Diagnostics AssessmentFrom EverandThe Enabling Environment for Disaster Risk Financing in Pakistan: Country Diagnostics AssessmentNo ratings yet

- 25 10 1108 - Ajar 08 2020 0071Document13 pages25 10 1108 - Ajar 08 2020 0071Hafiz Muhammad SaleemNo ratings yet

- Comparative Study of Islamic and Conventional Banking in Pakistan Based On Customer SatisfactionDocument7 pagesComparative Study of Islamic and Conventional Banking in Pakistan Based On Customer Satisfactionkazi mahmudurNo ratings yet

- 10 1108 - Ijse 06 2022 0441Document31 pages10 1108 - Ijse 06 2022 0441Yoyo PlayNo ratings yet

- GJBR V4N2 2010Document161 pagesGJBR V4N2 2010Yash SeetaramNo ratings yet

- MOSES KINYANJUI EMPIRICAL FINANCE SEMINAR PAPER RevisedDocument24 pagesMOSES KINYANJUI EMPIRICAL FINANCE SEMINAR PAPER RevisedMIRADOR ACCOUNTANTS KENYANo ratings yet

- The Impact of Behavioral Factors On EnvironmentalDocument19 pagesThe Impact of Behavioral Factors On EnvironmentalRai Saif SiddiqNo ratings yet

- Khan Et Al (2020) - NPL DeterminantsDocument11 pagesKhan Et Al (2020) - NPL Determinants20212111047 TEUKU MAULANA ARDIANSYAHNo ratings yet

- Factors That Affect Financial Sustainability of Microfinance Institution: Literature ReviewDocument7 pagesFactors That Affect Financial Sustainability of Microfinance Institution: Literature ReviewAntonette RayanNo ratings yet

- Risk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferenceDocument12 pagesRisk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferencePavithra GowthamNo ratings yet

- Empirical Study On Financial Literacy, Investors' Personality, Overcon Dence Bias and Investment Decisions and Risk Tolerance As Mediator FactorDocument22 pagesEmpirical Study On Financial Literacy, Investors' Personality, Overcon Dence Bias and Investment Decisions and Risk Tolerance As Mediator FactorZubaria BashirNo ratings yet

- 1 s2.0 S2214845022000837 MainDocument15 pages1 s2.0 S2214845022000837 MainSandara PepitoNo ratings yet

- IJFE-21-1594 Proof HiDocument16 pagesIJFE-21-1594 Proof HiShahid HussainNo ratings yet

- Cointegration of Loans-Libre PDFDocument15 pagesCointegration of Loans-Libre PDFGodfred AbleduNo ratings yet

- Financial Risk, Capital Adequacy and Liquidity Performance of Deposit Money Banks in NigeriaDocument12 pagesFinancial Risk, Capital Adequacy and Liquidity Performance of Deposit Money Banks in NigeriaEditor IJTSRDNo ratings yet

- A Comparative Study of Islamic and Conventional Banks Risk Management Practices - Empirical Evidence From PakistanDocument17 pagesA Comparative Study of Islamic and Conventional Banks Risk Management Practices - Empirical Evidence From Pakistanrashid.m.dzamboNo ratings yet

- 1 s2.0 S1877042814029760 MainDocument9 pages1 s2.0 S1877042814029760 MainVittaya RiaNo ratings yet

- Abdou, H. A. (2009) PDFDocument17 pagesAbdou, H. A. (2009) PDFJULIO CESAR MILLAN SOLARTENo ratings yet

- Title NEWDocument8 pagesTitle NEWshubhambachhav47No ratings yet

- Basiruddin & Ahmed (2020) Corporate Governance and Shariah Non-Compliant Risk in Islamic Banks Evidence From Southeast AsiaDocument23 pagesBasiruddin & Ahmed (2020) Corporate Governance and Shariah Non-Compliant Risk in Islamic Banks Evidence From Southeast Asiabaehaqi17No ratings yet

- Literature Review On Risk Management in Indian BanksDocument7 pagesLiterature Review On Risk Management in Indian BankscpifhhwgfNo ratings yet

- 37 6. Article 5 V2P1Document12 pages37 6. Article 5 V2P1Hafiz Muhammad SaleemNo ratings yet

- A AaaaaaaaaaDocument58 pagesA AaaaaaaaaachelangatNo ratings yet

- The Effect of Islamic Financing On Financing Risk in Islamic Commercial Banks in Indonesia (Empirical Study On Islamic Commercial Banks in Indonesia 2016-2020)Document7 pagesThe Effect of Islamic Financing On Financing Risk in Islamic Commercial Banks in Indonesia (Empirical Study On Islamic Commercial Banks in Indonesia 2016-2020)International Journal of Innovative Science and Research TechnologyNo ratings yet

- Risk Management, Strategic PDFDocument380 pagesRisk Management, Strategic PDFCong NguyenNo ratings yet

- Corporate Governance and Risk Disclosure: Evidence From Saudi ArabiaDocument22 pagesCorporate Governance and Risk Disclosure: Evidence From Saudi ArabiaAhli JurnalNo ratings yet

- 1321 ArticleText 1840 2 10 20210830Document19 pages1321 ArticleText 1840 2 10 20210830hasibabdullah527No ratings yet

- Interaction Effects of Professional Commitment, Customer Risk, Independent Pressure and Money Laundering Risk JudgmentDocument18 pagesInteraction Effects of Professional Commitment, Customer Risk, Independent Pressure and Money Laundering Risk Judgmenterfina istyaningrumNo ratings yet

- IC and Bank StabilityDocument30 pagesIC and Bank StabilityDharmendra SinghNo ratings yet

- 12 Hrushikesh and KaboorDocument7 pages12 Hrushikesh and KaboorSayan GaraiNo ratings yet

- Factors Affecting Liquidity Risk of Banks Empirical Evidence From The Banking Industry of BangladeshDocument7 pagesFactors Affecting Liquidity Risk of Banks Empirical Evidence From The Banking Industry of BangladeshInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Islamic Banks Credit Risk: A Panel Study: SciencedirectDocument8 pagesIslamic Banks Credit Risk: A Panel Study: SciencedirectafifahfauziyahNo ratings yet

- Challenges Facing The Development of Takaful Industry in Bangladesh and IndonesiaDocument14 pagesChallenges Facing The Development of Takaful Industry in Bangladesh and IndonesiaMuhammad Ali KhanNo ratings yet

- SC SustDocument26 pagesSC SustAziz Ibn MusahNo ratings yet

- 10 1108 - Ajeb 06 2021 0074Document31 pages10 1108 - Ajeb 06 2021 0074Rani LarassatiNo ratings yet

- Literature Review On Indian Banking SectorDocument7 pagesLiterature Review On Indian Banking Sectorafdtrzkhw100% (1)

- 3705 9837 2 PBDocument9 pages3705 9837 2 PBKhalis amnaNo ratings yet

- Credit Risk Management of Customers at Iranian BanksDocument11 pagesCredit Risk Management of Customers at Iranian BanksnhlNo ratings yet

- Farooq, Azantouti, Zaman 2024 - Non-Financial Information Assurance A Review of The Literature and Directions For Future ResearchDocument37 pagesFarooq, Azantouti, Zaman 2024 - Non-Financial Information Assurance A Review of The Literature and Directions For Future ResearchNathalia PereiraNo ratings yet

- Project Submitted in Partial Fulfilment of The Requirement For The Award of The Degree ofDocument7 pagesProject Submitted in Partial Fulfilment of The Requirement For The Award of The Degree ofNikhilNo ratings yet

- Literature Review Risk ManagementDocument4 pagesLiterature Review Risk Managementc5rr5sqw100% (1)

- Consumer Acceptance Toward Takaful in Pakistan: An Application of Diffusion of Innovation TheoryDocument20 pagesConsumer Acceptance Toward Takaful in Pakistan: An Application of Diffusion of Innovation TheoryTayyab KamalNo ratings yet

- Pacific-Basin Finance Journal: Karim Mimouni, Houcem Smaoui, Akram Temimi, Moh'd Al-Azzam TDocument13 pagesPacific-Basin Finance Journal: Karim Mimouni, Houcem Smaoui, Akram Temimi, Moh'd Al-Azzam TdeaNo ratings yet

- The Enabling Environment for Disaster Risk Financing in Nepal: Country Diagnostics AssessmentFrom EverandThe Enabling Environment for Disaster Risk Financing in Nepal: Country Diagnostics AssessmentNo ratings yet

- Rethinking Infrastructure Financing for Southeast Asia in the Post-Pandemic EraFrom EverandRethinking Infrastructure Financing for Southeast Asia in the Post-Pandemic EraNo ratings yet

- Financial Risk ND ProfitabilityDocument22 pagesFinancial Risk ND Profitabilitytungeena waseemNo ratings yet

- Imp Papr DissertationDocument24 pagesImp Papr DissertationSonaliNo ratings yet

- Islamic Banking and Finance Literature ReviewDocument10 pagesIslamic Banking and Finance Literature Reviewafmzmajcevielt100% (1)

- MBA1929-Article Text-2612-4-10-20230311Document8 pagesMBA1929-Article Text-2612-4-10-20230311Neha TaankNo ratings yet

- Anuradha BFDocument19 pagesAnuradha BFsarkiawalia84No ratings yet

- ISSN: 2320-5407 Int. J. Adv. Res. 7 (1), 811-849: Article DOI:10.21474/IJAR01/8392 Doi UrlDocument39 pagesISSN: 2320-5407 Int. J. Adv. Res. 7 (1), 811-849: Article DOI:10.21474/IJAR01/8392 Doi UrlSurajit SarbabidyaNo ratings yet

- 6051-Article Text-15476-1-10-20190204Document16 pages6051-Article Text-15476-1-10-20190204ZelekeNo ratings yet

- Facility Name / Country Audit Score 0: General InformationDocument233 pagesFacility Name / Country Audit Score 0: General InformationAbdul Hanan NasirNo ratings yet

- Lec 13Document20 pagesLec 13Abdul Hanan NasirNo ratings yet

- Presentation DataDocument1 pagePresentation DataAbdul Hanan NasirNo ratings yet

- Research Proposal Timeline Gantt ChartDocument1 pageResearch Proposal Timeline Gantt ChartAbdul Hanan NasirNo ratings yet

- Fast School of Management FYP Guidelines Fall-2023Document42 pagesFast School of Management FYP Guidelines Fall-2023Abdul Hanan NasirNo ratings yet

- HananDocument1 pageHananAbdul Hanan NasirNo ratings yet

- Green Marketing and Its Impact On ConsumersDocument9 pagesGreen Marketing and Its Impact On ConsumersAbdul Hanan NasirNo ratings yet

- Lab 1 TasksDocument1 pageLab 1 TasksAbdul Hanan NasirNo ratings yet

- SM AsignmentDocument5 pagesSM AsignmentAbdul Hanan NasirNo ratings yet

- Student ID Midterm 1 Midterm 2 Quizzes Assignmetns Class Participation Final Exam 15 15 5 10 5 50Document2 pagesStudent ID Midterm 1 Midterm 2 Quizzes Assignmetns Class Participation Final Exam 15 15 5 10 5 50Abdul Hanan NasirNo ratings yet

- 20F-0016 Assignment 2Document9 pages20F-0016 Assignment 2Abdul Hanan NasirNo ratings yet

- CSR SM AssignmentDocument4 pagesCSR SM AssignmentAbdul Hanan NasirNo ratings yet

- Employee Sample DataDocument60 pagesEmployee Sample DataAbdul Hanan NasirNo ratings yet

- Strategic Management: Rehbar Majeed TextilesDocument9 pagesStrategic Management: Rehbar Majeed TextilesAbdul Hanan NasirNo ratings yet

- Retail Supply Chain Concept & CasesDocument21 pagesRetail Supply Chain Concept & CasesAbdul Hanan NasirNo ratings yet

- From Pilot To Platform in Rural Pakistan - Case For First ClassDocument22 pagesFrom Pilot To Platform in Rural Pakistan - Case For First ClassAbdul Hanan NasirNo ratings yet

- Barringer E3 PPT 11Document34 pagesBarringer E3 PPT 11Abdul Hanan NasirNo ratings yet

- Assignment 2Document4 pagesAssignment 2Abdul Hanan NasirNo ratings yet

- Employee Feedback FormDocument2 pagesEmployee Feedback FormAbdul Hanan NasirNo ratings yet

- 16A Assignment1Document5 pages16A Assignment1Abdul Hanan NasirNo ratings yet

- Untitled DocumentDocument42 pagesUntitled DocumentAbdul Hanan NasirNo ratings yet

- Final Presentation FYPDocument21 pagesFinal Presentation FYPAbdul Hanan NasirNo ratings yet

- Employee Hiring FormDocument2 pagesEmployee Hiring FormAbdul Hanan NasirNo ratings yet

- Barringer E3 PPT 14Document31 pagesBarringer E3 PPT 14Abdul Hanan NasirNo ratings yet

- Student Biryani George Yip ModelDocument1 pageStudent Biryani George Yip ModelAbdul Hanan NasirNo ratings yet

- Barringer E3 PPT 12Document25 pagesBarringer E3 PPT 12Abdul Hanan NasirNo ratings yet

- Seminario 23-11-2015 Regina VivianeDocument14 pagesSeminario 23-11-2015 Regina VivianeAbdul Hanan NasirNo ratings yet

- Surah Baqarah Last 2 Ayat - Google SearchDocument1 pageSurah Baqarah Last 2 Ayat - Google SearchAbdul Hanan NasirNo ratings yet

- Environmental Factors Affecting Green Purchase Behaviors 2023 Cleaner EnviroDocument10 pagesEnvironmental Factors Affecting Green Purchase Behaviors 2023 Cleaner EnviroAbdul Hanan NasirNo ratings yet

- Problems W12Document14 pagesProblems W12Abdul Hanan NasirNo ratings yet

- Banyan Tree Case StudyDocument9 pagesBanyan Tree Case StudyFarhan Haseeb67% (3)

- Modern Marketing What It Is What It Isnt 2Document10 pagesModern Marketing What It Is What It Isnt 2Shashank SauravNo ratings yet

- SaaS FinOps Maturity Model - ChargebeeDocument19 pagesSaaS FinOps Maturity Model - ChargebeeJoão DobbinNo ratings yet

- AAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyDocument3 pagesAAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyJigar MakwanaNo ratings yet

- Government CorruptionDocument10 pagesGovernment Corruptionangel bNo ratings yet

- Met466 Module 4 NotesDocument16 pagesMet466 Module 4 NotesFarhan Vakkeparambil ShajahanNo ratings yet

- 01 Homework - Urbino Bsa - 4aDocument8 pages01 Homework - Urbino Bsa - 4aVeralou UrbinoNo ratings yet

- Value Stream Mapping PresentationDocument182 pagesValue Stream Mapping PresentationmohammedNo ratings yet

- SICS - Framework Overview Final v1 1Document40 pagesSICS - Framework Overview Final v1 1Hender PovedaNo ratings yet

- FT ActivPilot Concept C PVC KT 603 012022 enDocument252 pagesFT ActivPilot Concept C PVC KT 603 012022 enCase Lemn Polianske DerevoNo ratings yet

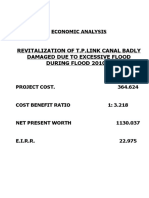

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- Mba-Ii Section - A Week 1 ReportDocument11 pagesMba-Ii Section - A Week 1 ReportHaris AmirNo ratings yet

- Sarigumba - Donato C. Cruz Trading Corp. v. CADocument2 pagesSarigumba - Donato C. Cruz Trading Corp. v. CANorberto Sarigumba IIINo ratings yet

- Human Resource Management - Key Challenges For 21st CenturyDocument3 pagesHuman Resource Management - Key Challenges For 21st Centuryarcherselevators50% (2)

- BS en 10216-1-2002Document28 pagesBS en 10216-1-2002David JayNo ratings yet

- DSR013847 1 Guest Pro Forma PDFDocument2 pagesDSR013847 1 Guest Pro Forma PDFEstherNo ratings yet

- Bustax Quiz 1 ReviewerDocument10 pagesBustax Quiz 1 ReviewerEleina Bea BernardoNo ratings yet

- SSG104Document65 pagesSSG104Nguyen Hoang Kien (K16HL)No ratings yet

- Foundations of Information Systems in BusinessDocument48 pagesFoundations of Information Systems in Businessmotz100% (8)

- ICAI GST Newsletter (26th Edition) PDFDocument24 pagesICAI GST Newsletter (26th Edition) PDFrohilacaNo ratings yet

- E Class Sra ConnnetDocument3 pagesE Class Sra ConnnetdmklNo ratings yet

- Lecture 10-Foreign Exchange MarketDocument42 pagesLecture 10-Foreign Exchange MarketfarahNo ratings yet

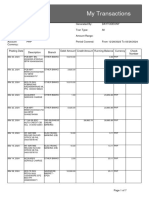

- My Transactions PDFDocument7 pagesMy Transactions PDFcavite.pautangNo ratings yet

- Lesson 08Document7 pagesLesson 08bc200200813 JUNAID ARSHADNo ratings yet

- English Micro Project 22101Document27 pagesEnglish Micro Project 22101GaneshNo ratings yet

- Indiamart Case StudyDocument35 pagesIndiamart Case StudyGrim ReaperNo ratings yet

- Factors Affecting Business Performance A Case Study of Small and Medium Enterprises in Ho Chi Minh CityDocument12 pagesFactors Affecting Business Performance A Case Study of Small and Medium Enterprises in Ho Chi Minh CityJanice PongpongNo ratings yet

- Kraken Intelligence's Crypto Rewards StakingDocument20 pagesKraken Intelligence's Crypto Rewards Stakingnukke1No ratings yet

- Tata Motors - AnalysisDocument22 pagesTata Motors - Analysissdhamangaonkar726489% (18)

- Treasury Design: The World of Corporate TreasuryDocument19 pagesTreasury Design: The World of Corporate TreasuryROUNAQ 11952No ratings yet