Current Liability

Current Liability

You might also like

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- Soal Dan Lembar KerjaDocument143 pagesSoal Dan Lembar KerjaDio Alfarras100% (1)

- Q No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsDocument6 pagesQ No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsMuhammad Haris100% (1)

- AC 1201 EFFECTIVE INTEREST METHOD Amortized Cost FVOCI and FVPLDocument23 pagesAC 1201 EFFECTIVE INTEREST METHOD Amortized Cost FVOCI and FVPLKabalaNo ratings yet

- Suggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"Document2 pagesSuggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"cutieaikoNo ratings yet

- Lease Financing Assignment (Excel)Document6 pagesLease Financing Assignment (Excel)Ashraful IslamNo ratings yet

- Audit CompletionDocument5 pagesAudit CompletionEunice CoronadoNo ratings yet

- Case StudyDocument2 pagesCase Studyの変化 ナザレNo ratings yet

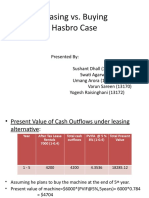

- Leasing vs. Buying Hasbro CaseDocument14 pagesLeasing vs. Buying Hasbro CaseUmang AroraNo ratings yet

- FF - Karil Koiriyah - 180421621551 - Tugas 4Document92 pagesFF - Karil Koiriyah - 180421621551 - Tugas 4karinaNo ratings yet

- Accounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreaDocument5 pagesAccounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreazarifNo ratings yet

- White Lightning Inc. Reported Income From Continuing Operations Before Income Taxes of $626,000Document9 pagesWhite Lightning Inc. Reported Income From Continuing Operations Before Income Taxes of $626,000Almarie gilNo ratings yet

- FfsDocument9 pagesFfsDivya PoornamNo ratings yet

- Teacher's Manual - Chapter 22 Current LiabilitiesDocument8 pagesTeacher's Manual - Chapter 22 Current LiabilitiesErwin Dave M. DahaoNo ratings yet

- Taxes and Depreciation: MacrsDocument20 pagesTaxes and Depreciation: MacrsRonald GibsonNo ratings yet

- Taxation of Hire Purchase Suspensive Sale TransactionsDocument30 pagesTaxation of Hire Purchase Suspensive Sale TransactionsJeremiah NcubeNo ratings yet

- Accounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreaDocument5 pagesAccounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreazarifNo ratings yet

- Sole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005Document8 pagesSole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005MahmozNo ratings yet

- 02 FAR02-answersDocument18 pages02 FAR02-answersBea GarciaNo ratings yet

- New Microsoft Excel WorksheetDocument4 pagesNew Microsoft Excel WorksheetAlexandraNo ratings yet

- Teacher's Manual - Financial Acctg 2Document233 pagesTeacher's Manual - Financial Acctg 2Adrian Mallari71% (21)

- Accounting For Long - Term Debt Instruments and Investments: Instructor: Mussa J AssadDocument33 pagesAccounting For Long - Term Debt Instruments and Investments: Instructor: Mussa J AssadERICK MLINGWANo ratings yet

- AnswerDocument23 pagesAnswerYousaf BhuttaNo ratings yet

- Chapter 3 - Bonds PayableDocument6 pagesChapter 3 - Bonds PayablePatricia EsplagoNo ratings yet

- ACCT EXAM NceshDocument7 pagesACCT EXAM Nceshncedilembokazi23No ratings yet

- Cash Flow Statement 1231Document26 pagesCash Flow Statement 1231Souvik DeNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- ACC106 Notes Receivable IllustrationsDocument23 pagesACC106 Notes Receivable IllustrationsJohn MaynardNo ratings yet

- Financial Accounting Cat 1 JonathanDocument14 pagesFinancial Accounting Cat 1 JonathanjonathanNo ratings yet

- 3 C Ifrs 16 Example Finance Lease by Lessor 01Document4 pages3 C Ifrs 16 Example Finance Lease by Lessor 01Imelda FebriputriNo ratings yet

- Income StatementDocument3 pagesIncome StatementBiswajit SarmaNo ratings yet

- Data Dukung NS Dan Catatan Atas Laporan KeuanganDocument57 pagesData Dukung NS Dan Catatan Atas Laporan KeuanganHafizd Az ZeinNo ratings yet

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Book Solutions Ch2 To Ch11Document45 pagesBook Solutions Ch2 To Ch11FayzanAhmedKhanNo ratings yet

- Chapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document26 pagesChapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din Sheryar100% (1)

- Tax 3702 Exam Pack 2016Document18 pagesTax 3702 Exam Pack 2016nhlakaniphoNo ratings yet

- Tugas Akuntansi Maulana Ramadhan 22522014Document25 pagesTugas Akuntansi Maulana Ramadhan 22522014King AzazirNo ratings yet

- Cash FlowDocument5 pagesCash FlowDivesh BabariaNo ratings yet

- Note Payable 2023Document27 pagesNote Payable 2023Avrille MacalinaoNo ratings yet

- Current Liability 2. Aspe 3. Added To The Bank Balance 4. Change in Current Portion of Bank Loan Payable 5. Statement of Financial Position 6. DDocument3 pagesCurrent Liability 2. Aspe 3. Added To The Bank Balance 4. Change in Current Portion of Bank Loan Payable 5. Statement of Financial Position 6. DPrateek ChandnaNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- CMA April - 14 Exam Question SolutionDocument55 pagesCMA April - 14 Exam Question Solutionkhandakeralihossain50% (2)

- Project: Submitted To: Prof. Touheed AlamDocument16 pagesProject: Submitted To: Prof. Touheed AlamSibghaNo ratings yet

- Intermediate Accounting Exam 3 SolutionsDocument7 pagesIntermediate Accounting Exam 3 SolutionsAlex SchuldinerNo ratings yet

- Kisi AklanDocument26 pagesKisi AklanTytii Softiarini YusufNo ratings yet

- Chapter 06 - AdjustmentsDocument26 pagesChapter 06 - AdjustmentsMkhonto Xulu100% (1)

- Current Liabilities and Warranties p2Document4 pagesCurrent Liabilities and Warranties p2James AngklaNo ratings yet

- Tutorial QuestionsDocument5 pagesTutorial QuestionsRavinesh PrasadNo ratings yet

- Profit Planning Activity-Based Budgeting and E-Budgeting - Exercise SolutionDocument6 pagesProfit Planning Activity-Based Budgeting and E-Budgeting - Exercise Solutionjha_abhijitNo ratings yet

- Solutions For Cash Flow Sums OnlyDocument11 pagesSolutions For Cash Flow Sums OnlyS. GOWRINo ratings yet

- FAP - Bodie Industrial Supply - LT 2Document16 pagesFAP - Bodie Industrial Supply - LT 2Marcus McWile MorningstarNo ratings yet

- Complex GroupDocument5 pagesComplex Grouptαtmαn dє grєαtNo ratings yet

- Kertas Kerja (Yesaya Ab 92 Ol RS 2) - Susper A - PPH BadanDocument7 pagesKertas Kerja (Yesaya Ab 92 Ol RS 2) - Susper A - PPH BadanRayentNo ratings yet

- Delta AzemDocument5 pagesDelta AzemAzema Azhybekova100% (2)

- Module 1 - Seatwork Answer KeyDocument3 pagesModule 1 - Seatwork Answer KeyKATHRYN CLAUDETTE RESENTENo ratings yet

- Leases (Part 2) : Problem 1: True or FalseDocument23 pagesLeases (Part 2) : Problem 1: True or FalseKim Hanbin100% (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Current LiabilityDocument21 pagesCurrent LiabilityMuhammad HarisNo ratings yet

- Sandak SlippersDocument3 pagesSandak SlippersMuhammad HarisNo ratings yet

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocument4 pagesBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- Class ExerciseDocument1 pageClass ExerciseMuhammad HarisNo ratings yet

- Session 2Document8 pagesSession 2Muhammad Haris100% (1)

- IBF Assignment Time Value of MoneyDocument3 pagesIBF Assignment Time Value of MoneyMuhammad HarisNo ratings yet

- Channel Design Process: Define Customer NeedsDocument30 pagesChannel Design Process: Define Customer NeedsMuhammad HarisNo ratings yet

- Channel Management SlideDocument25 pagesChannel Management SlideMuhammad HarisNo ratings yet

- Supply and Deman QuestionsDocument3 pagesSupply and Deman QuestionsMuhammad HarisNo ratings yet

- OMBUDSMAN v. CSC G.R. No. 159940Document1 pageOMBUDSMAN v. CSC G.R. No. 159940rommel alimagnoNo ratings yet

- Phantoms and Monsters - Pulse of The ParanormalDocument14 pagesPhantoms and Monsters - Pulse of The ParanormalRaHorusNo ratings yet

- SC Verdict On Hindu Women's Inheritance Rights: Why in NewsDocument3 pagesSC Verdict On Hindu Women's Inheritance Rights: Why in NewsSaurabh YadavNo ratings yet

- FFFFDocument3 pagesFFFFMotlatso MaakeNo ratings yet

- Chilanga Cement PLC Vs Kasote Singogo-2Document5 pagesChilanga Cement PLC Vs Kasote Singogo-2Thandiwe Deborah0% (1)

- Petitioner Respondent: First DivisionDocument5 pagesPetitioner Respondent: First DivisionJakielyn Anne CruzNo ratings yet

- People vs. TyDocument6 pagesPeople vs. TyNash LedesmaNo ratings yet

- Consumer Right - Class 10Document5 pagesConsumer Right - Class 10santha banumthiNo ratings yet

- JD - Credit ManagerDocument2 pagesJD - Credit Managersanket patilNo ratings yet

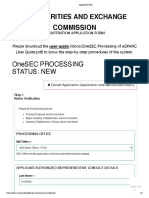

- Securities and Exchange Commission: Onesec Processing Status: NewDocument4 pagesSecurities and Exchange Commission: Onesec Processing Status: NewMikee PortesNo ratings yet

- LBP vs. CADocument2 pagesLBP vs. CAermeline tampusNo ratings yet

- New Labour CodesDocument3 pagesNew Labour CodesAnsh GulatiNo ratings yet

- Ethics IntroDocument16 pagesEthics IntroAngela YlaganNo ratings yet

- Key Assumptions in International Relations and Global GovernanceDocument4 pagesKey Assumptions in International Relations and Global GovernancezuennamarieNo ratings yet

- Topic 3 Ethical Requirements 2Document8 pagesTopic 3 Ethical Requirements 2Niña VictoriaNo ratings yet

- Legal Methods ProjectDocument22 pagesLegal Methods Projectuma mishraNo ratings yet

- After Blenheim Extracts 7 &8Document1 pageAfter Blenheim Extracts 7 &8Kaushik MishraNo ratings yet

- FSF - BARS Audit Agreement Version 12.1Document18 pagesFSF - BARS Audit Agreement Version 12.1Marcela AgudeloNo ratings yet

- 1300SRM1455 (06 2017) Us en PDF PDF Clutch Transmission (Mechanics)Document1 page1300SRM1455 (06 2017) Us en PDF PDF Clutch Transmission (Mechanics)6hvbc98br7No ratings yet

- On The Morality of Human Acts (Norms and Determinants of Human Acts)Document50 pagesOn The Morality of Human Acts (Norms and Determinants of Human Acts)NarelJade AtamosaNo ratings yet

- Charitable TrustDocument2 pagesCharitable TrustvipingplNo ratings yet

- Translating 4567Document5 pagesTranslating 4567Huỳnh NhưNo ratings yet

- Requirements in B.S. Pmi BoholDocument2 pagesRequirements in B.S. Pmi BoholNorwin Alcaide50% (2)

- 09 Leanoejspring 14Document9 pages09 Leanoejspring 14hamdaNo ratings yet

- B.A. (Hons.) Pol. Science 2nd SemesterDocument23 pagesB.A. (Hons.) Pol. Science 2nd SemesterNAVYA BANSAL BBG220461No ratings yet

- 1123 135933 Awardees For Jus Festum - AcademicDocument2 pages1123 135933 Awardees For Jus Festum - AcademicAnnon CriticNo ratings yet

- Malaybalay City Youth Development Office: The ProposedDocument10 pagesMalaybalay City Youth Development Office: The ProposedDence Cris RondonNo ratings yet

- Lobby Floor Plan (Ground)Document1 pageLobby Floor Plan (Ground)Ma. Isabel RodriguezNo ratings yet

- 2020 Commiment of ChaperonDocument1 page2020 Commiment of ChaperonEric Cris TorresNo ratings yet

- Jo 6Document5 pagesJo 6Sachin JainNo ratings yet

You might also like

- Accounting For Managers (Assignment One (E-Finance) ) Question OneDocument7 pagesAccounting For Managers (Assignment One (E-Finance) ) Question OnehananNo ratings yet

- Soal Dan Lembar KerjaDocument143 pagesSoal Dan Lembar KerjaDio Alfarras100% (1)

- Q No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsDocument6 pagesQ No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsMuhammad Haris100% (1)

- AC 1201 EFFECTIVE INTEREST METHOD Amortized Cost FVOCI and FVPLDocument23 pagesAC 1201 EFFECTIVE INTEREST METHOD Amortized Cost FVOCI and FVPLKabalaNo ratings yet

- Suggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"Document2 pagesSuggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"cutieaikoNo ratings yet

- Lease Financing Assignment (Excel)Document6 pagesLease Financing Assignment (Excel)Ashraful IslamNo ratings yet

- Audit CompletionDocument5 pagesAudit CompletionEunice CoronadoNo ratings yet

- Case StudyDocument2 pagesCase Studyの変化 ナザレNo ratings yet

- Leasing vs. Buying Hasbro CaseDocument14 pagesLeasing vs. Buying Hasbro CaseUmang AroraNo ratings yet

- FF - Karil Koiriyah - 180421621551 - Tugas 4Document92 pagesFF - Karil Koiriyah - 180421621551 - Tugas 4karinaNo ratings yet

- Accounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreaDocument5 pagesAccounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreazarifNo ratings yet

- White Lightning Inc. Reported Income From Continuing Operations Before Income Taxes of $626,000Document9 pagesWhite Lightning Inc. Reported Income From Continuing Operations Before Income Taxes of $626,000Almarie gilNo ratings yet

- FfsDocument9 pagesFfsDivya PoornamNo ratings yet

- Teacher's Manual - Chapter 22 Current LiabilitiesDocument8 pagesTeacher's Manual - Chapter 22 Current LiabilitiesErwin Dave M. DahaoNo ratings yet

- Taxes and Depreciation: MacrsDocument20 pagesTaxes and Depreciation: MacrsRonald GibsonNo ratings yet

- Taxation of Hire Purchase Suspensive Sale TransactionsDocument30 pagesTaxation of Hire Purchase Suspensive Sale TransactionsJeremiah NcubeNo ratings yet

- Accounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreaDocument5 pagesAccounts Register of Aline Glory Plot No. 964, Road No.13, Block-G Bashundhara Residential AreazarifNo ratings yet

- Sole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005Document8 pagesSole Trader - Final Accounts: The Following Trial Balance Was Extracted From The Books of K. Kelly On 31/12/2005MahmozNo ratings yet

- 02 FAR02-answersDocument18 pages02 FAR02-answersBea GarciaNo ratings yet

- New Microsoft Excel WorksheetDocument4 pagesNew Microsoft Excel WorksheetAlexandraNo ratings yet

- Teacher's Manual - Financial Acctg 2Document233 pagesTeacher's Manual - Financial Acctg 2Adrian Mallari71% (21)

- Accounting For Long - Term Debt Instruments and Investments: Instructor: Mussa J AssadDocument33 pagesAccounting For Long - Term Debt Instruments and Investments: Instructor: Mussa J AssadERICK MLINGWANo ratings yet

- AnswerDocument23 pagesAnswerYousaf BhuttaNo ratings yet

- Chapter 3 - Bonds PayableDocument6 pagesChapter 3 - Bonds PayablePatricia EsplagoNo ratings yet

- ACCT EXAM NceshDocument7 pagesACCT EXAM Nceshncedilembokazi23No ratings yet

- Cash Flow Statement 1231Document26 pagesCash Flow Statement 1231Souvik DeNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- ACC106 Notes Receivable IllustrationsDocument23 pagesACC106 Notes Receivable IllustrationsJohn MaynardNo ratings yet

- Financial Accounting Cat 1 JonathanDocument14 pagesFinancial Accounting Cat 1 JonathanjonathanNo ratings yet

- 3 C Ifrs 16 Example Finance Lease by Lessor 01Document4 pages3 C Ifrs 16 Example Finance Lease by Lessor 01Imelda FebriputriNo ratings yet

- Income StatementDocument3 pagesIncome StatementBiswajit SarmaNo ratings yet

- Data Dukung NS Dan Catatan Atas Laporan KeuanganDocument57 pagesData Dukung NS Dan Catatan Atas Laporan KeuanganHafizd Az ZeinNo ratings yet

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Book Solutions Ch2 To Ch11Document45 pagesBook Solutions Ch2 To Ch11FayzanAhmedKhanNo ratings yet

- Chapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document26 pagesChapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din Sheryar100% (1)

- Tax 3702 Exam Pack 2016Document18 pagesTax 3702 Exam Pack 2016nhlakaniphoNo ratings yet

- Tugas Akuntansi Maulana Ramadhan 22522014Document25 pagesTugas Akuntansi Maulana Ramadhan 22522014King AzazirNo ratings yet

- Cash FlowDocument5 pagesCash FlowDivesh BabariaNo ratings yet

- Note Payable 2023Document27 pagesNote Payable 2023Avrille MacalinaoNo ratings yet

- Current Liability 2. Aspe 3. Added To The Bank Balance 4. Change in Current Portion of Bank Loan Payable 5. Statement of Financial Position 6. DDocument3 pagesCurrent Liability 2. Aspe 3. Added To The Bank Balance 4. Change in Current Portion of Bank Loan Payable 5. Statement of Financial Position 6. DPrateek ChandnaNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- CMA April - 14 Exam Question SolutionDocument55 pagesCMA April - 14 Exam Question Solutionkhandakeralihossain50% (2)

- Project: Submitted To: Prof. Touheed AlamDocument16 pagesProject: Submitted To: Prof. Touheed AlamSibghaNo ratings yet

- Intermediate Accounting Exam 3 SolutionsDocument7 pagesIntermediate Accounting Exam 3 SolutionsAlex SchuldinerNo ratings yet

- Kisi AklanDocument26 pagesKisi AklanTytii Softiarini YusufNo ratings yet

- Chapter 06 - AdjustmentsDocument26 pagesChapter 06 - AdjustmentsMkhonto Xulu100% (1)

- Current Liabilities and Warranties p2Document4 pagesCurrent Liabilities and Warranties p2James AngklaNo ratings yet

- Tutorial QuestionsDocument5 pagesTutorial QuestionsRavinesh PrasadNo ratings yet

- Profit Planning Activity-Based Budgeting and E-Budgeting - Exercise SolutionDocument6 pagesProfit Planning Activity-Based Budgeting and E-Budgeting - Exercise Solutionjha_abhijitNo ratings yet

- Solutions For Cash Flow Sums OnlyDocument11 pagesSolutions For Cash Flow Sums OnlyS. GOWRINo ratings yet

- FAP - Bodie Industrial Supply - LT 2Document16 pagesFAP - Bodie Industrial Supply - LT 2Marcus McWile MorningstarNo ratings yet

- Complex GroupDocument5 pagesComplex Grouptαtmαn dє grєαtNo ratings yet

- Kertas Kerja (Yesaya Ab 92 Ol RS 2) - Susper A - PPH BadanDocument7 pagesKertas Kerja (Yesaya Ab 92 Ol RS 2) - Susper A - PPH BadanRayentNo ratings yet

- Delta AzemDocument5 pagesDelta AzemAzema Azhybekova100% (2)

- Module 1 - Seatwork Answer KeyDocument3 pagesModule 1 - Seatwork Answer KeyKATHRYN CLAUDETTE RESENTENo ratings yet

- Leases (Part 2) : Problem 1: True or FalseDocument23 pagesLeases (Part 2) : Problem 1: True or FalseKim Hanbin100% (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Current LiabilityDocument21 pagesCurrent LiabilityMuhammad HarisNo ratings yet

- Sandak SlippersDocument3 pagesSandak SlippersMuhammad HarisNo ratings yet

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocument4 pagesBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- Class ExerciseDocument1 pageClass ExerciseMuhammad HarisNo ratings yet

- Session 2Document8 pagesSession 2Muhammad Haris100% (1)

- IBF Assignment Time Value of MoneyDocument3 pagesIBF Assignment Time Value of MoneyMuhammad HarisNo ratings yet

- Channel Design Process: Define Customer NeedsDocument30 pagesChannel Design Process: Define Customer NeedsMuhammad HarisNo ratings yet

- Channel Management SlideDocument25 pagesChannel Management SlideMuhammad HarisNo ratings yet

- Supply and Deman QuestionsDocument3 pagesSupply and Deman QuestionsMuhammad HarisNo ratings yet

- OMBUDSMAN v. CSC G.R. No. 159940Document1 pageOMBUDSMAN v. CSC G.R. No. 159940rommel alimagnoNo ratings yet

- Phantoms and Monsters - Pulse of The ParanormalDocument14 pagesPhantoms and Monsters - Pulse of The ParanormalRaHorusNo ratings yet

- SC Verdict On Hindu Women's Inheritance Rights: Why in NewsDocument3 pagesSC Verdict On Hindu Women's Inheritance Rights: Why in NewsSaurabh YadavNo ratings yet

- FFFFDocument3 pagesFFFFMotlatso MaakeNo ratings yet

- Chilanga Cement PLC Vs Kasote Singogo-2Document5 pagesChilanga Cement PLC Vs Kasote Singogo-2Thandiwe Deborah0% (1)

- Petitioner Respondent: First DivisionDocument5 pagesPetitioner Respondent: First DivisionJakielyn Anne CruzNo ratings yet

- People vs. TyDocument6 pagesPeople vs. TyNash LedesmaNo ratings yet

- Consumer Right - Class 10Document5 pagesConsumer Right - Class 10santha banumthiNo ratings yet

- JD - Credit ManagerDocument2 pagesJD - Credit Managersanket patilNo ratings yet

- Securities and Exchange Commission: Onesec Processing Status: NewDocument4 pagesSecurities and Exchange Commission: Onesec Processing Status: NewMikee PortesNo ratings yet

- LBP vs. CADocument2 pagesLBP vs. CAermeline tampusNo ratings yet

- New Labour CodesDocument3 pagesNew Labour CodesAnsh GulatiNo ratings yet

- Ethics IntroDocument16 pagesEthics IntroAngela YlaganNo ratings yet

- Key Assumptions in International Relations and Global GovernanceDocument4 pagesKey Assumptions in International Relations and Global GovernancezuennamarieNo ratings yet

- Topic 3 Ethical Requirements 2Document8 pagesTopic 3 Ethical Requirements 2Niña VictoriaNo ratings yet

- Legal Methods ProjectDocument22 pagesLegal Methods Projectuma mishraNo ratings yet

- After Blenheim Extracts 7 &8Document1 pageAfter Blenheim Extracts 7 &8Kaushik MishraNo ratings yet

- FSF - BARS Audit Agreement Version 12.1Document18 pagesFSF - BARS Audit Agreement Version 12.1Marcela AgudeloNo ratings yet

- 1300SRM1455 (06 2017) Us en PDF PDF Clutch Transmission (Mechanics)Document1 page1300SRM1455 (06 2017) Us en PDF PDF Clutch Transmission (Mechanics)6hvbc98br7No ratings yet

- On The Morality of Human Acts (Norms and Determinants of Human Acts)Document50 pagesOn The Morality of Human Acts (Norms and Determinants of Human Acts)NarelJade AtamosaNo ratings yet

- Charitable TrustDocument2 pagesCharitable TrustvipingplNo ratings yet

- Translating 4567Document5 pagesTranslating 4567Huỳnh NhưNo ratings yet

- Requirements in B.S. Pmi BoholDocument2 pagesRequirements in B.S. Pmi BoholNorwin Alcaide50% (2)

- 09 Leanoejspring 14Document9 pages09 Leanoejspring 14hamdaNo ratings yet

- B.A. (Hons.) Pol. Science 2nd SemesterDocument23 pagesB.A. (Hons.) Pol. Science 2nd SemesterNAVYA BANSAL BBG220461No ratings yet

- 1123 135933 Awardees For Jus Festum - AcademicDocument2 pages1123 135933 Awardees For Jus Festum - AcademicAnnon CriticNo ratings yet

- Malaybalay City Youth Development Office: The ProposedDocument10 pagesMalaybalay City Youth Development Office: The ProposedDence Cris RondonNo ratings yet

- Lobby Floor Plan (Ground)Document1 pageLobby Floor Plan (Ground)Ma. Isabel RodriguezNo ratings yet

- 2020 Commiment of ChaperonDocument1 page2020 Commiment of ChaperonEric Cris TorresNo ratings yet

- Jo 6Document5 pagesJo 6Sachin JainNo ratings yet