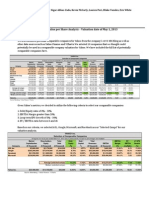

Financial Feasibility Study

Financial Feasibility Study

You might also like

- IE54500 - Problem Set 4: 1. Pure and Mixed Nash EquilibriaDocument5 pagesIE54500 - Problem Set 4: 1. Pure and Mixed Nash EquilibriaM100% (1)

- Case Star Hub AnswersDocument2 pagesCase Star Hub AnswersTarannum TahsinNo ratings yet

- Auditing CA Final Investigation and Due DiligenceDocument26 pagesAuditing CA Final Investigation and Due Diligencevarunmonga90No ratings yet

- Pricing StrategiesDocument4 pagesPricing StrategiesvinniieeNo ratings yet

- CH - 4 - Time Value of MoneyDocument49 pagesCH - 4 - Time Value of Moneyak sNo ratings yet

- 6W2X - Business Model Canvas With ExplanationsDocument2 pages6W2X - Business Model Canvas With ExplanationstorqtechNo ratings yet

- Feasibility Study of ProjectDocument15 pagesFeasibility Study of ProjectMauliddha RachmiNo ratings yet

- Days-Sales-Outstanding-TemplateDocument3 pagesDays-Sales-Outstanding-TemplateKaren Anne Pineda IngenteNo ratings yet

- Pestle Analysis - Alesh and GroupDocument18 pagesPestle Analysis - Alesh and GroupJay KapoorNo ratings yet

- Financial For Feasibility StudyDocument15 pagesFinancial For Feasibility StudyAbigail GeronimoNo ratings yet

- Actuaries 4Document69 pagesActuaries 4MuradNo ratings yet

- Val PacketDocument157 pagesVal PacketKumar PrashantNo ratings yet

- Capital+budgeting UnsolvedDocument4 pagesCapital+budgeting UnsolvedutamiNo ratings yet

- Create Application: Equity Template BuilderDocument1 pageCreate Application: Equity Template Builderattikouris100% (1)

- Chapter14, Pricing StrategyDocument25 pagesChapter14, Pricing StrategysekaramariliesNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- Innovation Management Types Management Practices and Innovation Performance in Services Industry of Developing EconomiesDocument15 pagesInnovation Management Types Management Practices and Innovation Performance in Services Industry of Developing EconomiesLilis PurnamasariNo ratings yet

- Finquiz - Curriculum Note Study Session 2 Reading 5Document7 pagesFinquiz - Curriculum Note Study Session 2 Reading 5api-289145400No ratings yet

- FCFE ValuationDocument27 pagesFCFE ValuationTaleya FatimaNo ratings yet

- Aicpa Accounting GlossaryDocument24 pagesAicpa Accounting GlossaryRafael AlemanNo ratings yet

- Pricing StrategiesDocument14 pagesPricing StrategiesAnonymous ibmeej9No ratings yet

- MUG Business Models UplDocument23 pagesMUG Business Models UplChristoph MagistraNo ratings yet

- Discounted Cash Flow ApplicationsDocument27 pagesDiscounted Cash Flow ApplicationsAvinash DasNo ratings yet

- The Challenges of Integrating Peace Journalism Into Conventional Journalism Practice - A Case Study of The LRA Peace ProcessDocument136 pagesThe Challenges of Integrating Peace Journalism Into Conventional Journalism Practice - A Case Study of The LRA Peace ProcessBirungi KamaraNo ratings yet

- The Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinDocument45 pagesThe Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinSobia NasreenNo ratings yet

- Investment Behaviour PDFDocument44 pagesInvestment Behaviour PDFSajoy P.B.100% (1)

- Extra WorkDocument3 pagesExtra WorkSarfaraj OviNo ratings yet

- Q1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?Document18 pagesQ1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?udayvadapalliNo ratings yet

- Feasibility Study On New BusinessDocument8 pagesFeasibility Study On New BusinessWyn OkpapiNo ratings yet

- Case StudyDocument20 pagesCase Studywenkyganda100% (1)

- Strategic Planning and ImplementationDocument12 pagesStrategic Planning and ImplementationShiva LKLNo ratings yet

- Financial AspectDocument13 pagesFinancial AspectAngelica CalubayNo ratings yet

- Marketing Plan MR Bean SingaporeDocument19 pagesMarketing Plan MR Bean SingaporejennifersmithsahNo ratings yet

- A Case Study of Snowhite Dry Cleaners Pakistan PDFDocument104 pagesA Case Study of Snowhite Dry Cleaners Pakistan PDFhisroyalmajestyNo ratings yet

- A Feasibility Study For A Cleaning CompanyDocument53 pagesA Feasibility Study For A Cleaning CompanyRogerNo ratings yet

- 171 Value Proposition CanvassDocument2 pages171 Value Proposition CanvassNaruto UzumakiNo ratings yet

- Pre-Money Valuation: Multiple ApproachDocument16 pagesPre-Money Valuation: Multiple ApproachDavid ChikhladzeNo ratings yet

- L8 Raising CapitalDocument26 pagesL8 Raising CapitalKranthi ManthriNo ratings yet

- NPV and IRRDocument7 pagesNPV and IRRWondim GenetNo ratings yet

- Marketing Aspect: Learning OutcomesDocument23 pagesMarketing Aspect: Learning OutcomesKristine Lirose BordeosNo ratings yet

- Ch1 - Management of Technology - An OverviewDocument36 pagesCh1 - Management of Technology - An OverviewMuhd ShaddetnyNo ratings yet

- Forecasting Cases Final 1Document43 pagesForecasting Cases Final 1Vipul SinghNo ratings yet

- Case: Feuture, Inc.: Far Eastern UniversityDocument11 pagesCase: Feuture, Inc.: Far Eastern UniversityAmro Ahmed RazigNo ratings yet

- Lucio, Mary-Ann Grace S. Real-World FocusDocument2 pagesLucio, Mary-Ann Grace S. Real-World FocusGrace SimonNo ratings yet

- Yahoo! Inc. Valuation ProjectDocument8 pagesYahoo! Inc. Valuation ProjectNigar_AbbasNo ratings yet

- Solved Forecasting The Success of New Product Introductions Is Notoriously DifficultDocument1 pageSolved Forecasting The Success of New Product Introductions Is Notoriously DifficultM Bilal SaleemNo ratings yet

- Goal SseekDocument5 pagesGoal SseekFilip NikolovskiNo ratings yet

- Case Study 4 STMicroelectronics - TQM Implementation and Policy Deployment Cua To DayDocument10 pagesCase Study 4 STMicroelectronics - TQM Implementation and Policy Deployment Cua To DayMy NguyễnNo ratings yet

- Technological Institute of The PhilippinesDocument31 pagesTechnological Institute of The PhilippinesEUNICE ANGELA LASCONIANo ratings yet

- Valuing Private Companies:: Factors and Approaches To ConsiderDocument35 pagesValuing Private Companies:: Factors and Approaches To ConsiderAvinash DasNo ratings yet

- Sonali Bank CSRDocument16 pagesSonali Bank CSRUSHA IT100% (1)

- Forecasting PDFDocument69 pagesForecasting PDFSuba NitaNo ratings yet

- Equivalent Annual AnnuityDocument10 pagesEquivalent Annual Annuitymohsin_ali07428097No ratings yet

- Capital Budgeting 55Document54 pagesCapital Budgeting 55Hitesh Jain0% (1)

- Chapter 13 ValuationDocument23 pagesChapter 13 ValuationIndah Dwi RetnoNo ratings yet

- Lecture 7 (Financial Analysis Section 2) RevisedDocument35 pagesLecture 7 (Financial Analysis Section 2) RevisedHari SharmaNo ratings yet

- The Time Value of MoneyDocument66 pagesThe Time Value of MoneyrachealllNo ratings yet

- Stock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaDocument40 pagesStock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaJOHN PAOLO EVORANo ratings yet

- RC Equity Research Report Essentials CFA InstituteDocument3 pagesRC Equity Research Report Essentials CFA InstitutetheakjNo ratings yet

- Ratio AnalysisDocument33 pagesRatio AnalysisJhagantini PalaniveluNo ratings yet

- Capital Budgeting & Decision...Document3 pagesCapital Budgeting & Decision...Ajit Mohan DasNo ratings yet

- 2023 Article 688Document13 pages2023 Article 688Ariandindi AriandiNo ratings yet

- LTE UE Power Consumption Model PDFDocument5 pagesLTE UE Power Consumption Model PDFNikNo ratings yet

- Article 7 TG October December 2020 Ms ChitraSharma DR Shaifali Full1036Document5 pagesArticle 7 TG October December 2020 Ms ChitraSharma DR Shaifali Full1036Putri Azzahra Salsabila putriazzahra.2019No ratings yet

- 11 Biology - Test Maker @Document1 page11 Biology - Test Maker @Waleed AnsariNo ratings yet

- MeasurIT Flexim ADM6725 Application Water Consumption Bottling Line 0809Document1 pageMeasurIT Flexim ADM6725 Application Water Consumption Bottling Line 0809cwiejkowskaNo ratings yet

- MIDTERMDocument6 pagesMIDTERMLiana XudabaxshyanNo ratings yet

- T M P S R P C: He Anagement of Ublic Ector Ecords: Rinciples and OntextDocument161 pagesT M P S R P C: He Anagement of Ublic Ector Ecords: Rinciples and OntextSaiful QazaNo ratings yet

- What Is DesulfurizationDocument20 pagesWhat Is DesulfurizationYash NandurkarNo ratings yet

- NJRSF Poster 2020Document2 pagesNJRSF Poster 2020api-502690136No ratings yet

- E 1067 TestDocument12 pagesE 1067 Testpandi007No ratings yet

- Flow Control Valve Serial Number PDFDocument3 pagesFlow Control Valve Serial Number PDFusman khanNo ratings yet

- Pak Matiari-Lahore Transmission Company (Private) LimitedDocument4 pagesPak Matiari-Lahore Transmission Company (Private) LimitedAftab Ejaz QureshiNo ratings yet

- Material Transfer Agreement FormDocument2 pagesMaterial Transfer Agreement FormFritz CarpenteroNo ratings yet

- Quick Start Guide: What You GetDocument8 pagesQuick Start Guide: What You GetAle NietoNo ratings yet

- Fundamentals SyllabusDocument12 pagesFundamentals SyllabusRoy CabarlesNo ratings yet

- Data Sheet Milk Reception Unit.1 enDocument2 pagesData Sheet Milk Reception Unit.1 enBoricean Gheorghita100% (1)

- Committee of Permanent Representatives To Asean in JakartaDocument1 pageCommittee of Permanent Representatives To Asean in Jakartamiharbi cortezNo ratings yet

- How To Resolve Costing ErrorsDocument38 pagesHow To Resolve Costing ErrorsNathanNo ratings yet

- NG Rtgs Ver 16th June14Document3 pagesNG Rtgs Ver 16th June14Supreeth SharmaNo ratings yet

- Brazing RiskDocument2 pagesBrazing Riskanon_12627423No ratings yet

- What Is A Share or Stock?Document12 pagesWhat Is A Share or Stock?Vicky MbaNo ratings yet

- Essay The Government Has No Business Being in BusinessDocument2 pagesEssay The Government Has No Business Being in BusinessNikhil Johri100% (1)

- Job Application Email PracticeDocument1 pageJob Application Email PracticeGilda MoNo ratings yet

- ExpectationsDocument11 pagesExpectationsapi-341254245No ratings yet

- 8.12 Live DinieDocument24 pages8.12 Live DinieAdiff CxainzNo ratings yet

- East West Pesticide and Fungicide ListDocument10 pagesEast West Pesticide and Fungicide ListnormanwillowNo ratings yet

- SRF060424 03Document18 pagesSRF060424 03nailgrpNo ratings yet

- FABM 112 Week 1 9 LegitDocument9 pagesFABM 112 Week 1 9 Legitjean heidi espinas25% (4)

- The Millennium Park Bus DepotDocument2 pagesThe Millennium Park Bus DepotSaiRajuNo ratings yet

You might also like

- IE54500 - Problem Set 4: 1. Pure and Mixed Nash EquilibriaDocument5 pagesIE54500 - Problem Set 4: 1. Pure and Mixed Nash EquilibriaM100% (1)

- Case Star Hub AnswersDocument2 pagesCase Star Hub AnswersTarannum TahsinNo ratings yet

- Auditing CA Final Investigation and Due DiligenceDocument26 pagesAuditing CA Final Investigation and Due Diligencevarunmonga90No ratings yet

- Pricing StrategiesDocument4 pagesPricing StrategiesvinniieeNo ratings yet

- CH - 4 - Time Value of MoneyDocument49 pagesCH - 4 - Time Value of Moneyak sNo ratings yet

- 6W2X - Business Model Canvas With ExplanationsDocument2 pages6W2X - Business Model Canvas With ExplanationstorqtechNo ratings yet

- Feasibility Study of ProjectDocument15 pagesFeasibility Study of ProjectMauliddha RachmiNo ratings yet

- Days-Sales-Outstanding-TemplateDocument3 pagesDays-Sales-Outstanding-TemplateKaren Anne Pineda IngenteNo ratings yet

- Pestle Analysis - Alesh and GroupDocument18 pagesPestle Analysis - Alesh and GroupJay KapoorNo ratings yet

- Financial For Feasibility StudyDocument15 pagesFinancial For Feasibility StudyAbigail GeronimoNo ratings yet

- Actuaries 4Document69 pagesActuaries 4MuradNo ratings yet

- Val PacketDocument157 pagesVal PacketKumar PrashantNo ratings yet

- Capital+budgeting UnsolvedDocument4 pagesCapital+budgeting UnsolvedutamiNo ratings yet

- Create Application: Equity Template BuilderDocument1 pageCreate Application: Equity Template Builderattikouris100% (1)

- Chapter14, Pricing StrategyDocument25 pagesChapter14, Pricing StrategysekaramariliesNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- Innovation Management Types Management Practices and Innovation Performance in Services Industry of Developing EconomiesDocument15 pagesInnovation Management Types Management Practices and Innovation Performance in Services Industry of Developing EconomiesLilis PurnamasariNo ratings yet

- Finquiz - Curriculum Note Study Session 2 Reading 5Document7 pagesFinquiz - Curriculum Note Study Session 2 Reading 5api-289145400No ratings yet

- FCFE ValuationDocument27 pagesFCFE ValuationTaleya FatimaNo ratings yet

- Aicpa Accounting GlossaryDocument24 pagesAicpa Accounting GlossaryRafael AlemanNo ratings yet

- Pricing StrategiesDocument14 pagesPricing StrategiesAnonymous ibmeej9No ratings yet

- MUG Business Models UplDocument23 pagesMUG Business Models UplChristoph MagistraNo ratings yet

- Discounted Cash Flow ApplicationsDocument27 pagesDiscounted Cash Flow ApplicationsAvinash DasNo ratings yet

- The Challenges of Integrating Peace Journalism Into Conventional Journalism Practice - A Case Study of The LRA Peace ProcessDocument136 pagesThe Challenges of Integrating Peace Journalism Into Conventional Journalism Practice - A Case Study of The LRA Peace ProcessBirungi KamaraNo ratings yet

- The Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinDocument45 pagesThe Accounting Cycle: Capturing Economic Events: Mcgraw-Hill/IrwinSobia NasreenNo ratings yet

- Investment Behaviour PDFDocument44 pagesInvestment Behaviour PDFSajoy P.B.100% (1)

- Extra WorkDocument3 pagesExtra WorkSarfaraj OviNo ratings yet

- Q1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?Document18 pagesQ1) What Is Cost of Capital? How Is It Calculated For Different Sources of Capital? How Is Average Weighted Cost of Capital Measured?udayvadapalliNo ratings yet

- Feasibility Study On New BusinessDocument8 pagesFeasibility Study On New BusinessWyn OkpapiNo ratings yet

- Case StudyDocument20 pagesCase Studywenkyganda100% (1)

- Strategic Planning and ImplementationDocument12 pagesStrategic Planning and ImplementationShiva LKLNo ratings yet

- Financial AspectDocument13 pagesFinancial AspectAngelica CalubayNo ratings yet

- Marketing Plan MR Bean SingaporeDocument19 pagesMarketing Plan MR Bean SingaporejennifersmithsahNo ratings yet

- A Case Study of Snowhite Dry Cleaners Pakistan PDFDocument104 pagesA Case Study of Snowhite Dry Cleaners Pakistan PDFhisroyalmajestyNo ratings yet

- A Feasibility Study For A Cleaning CompanyDocument53 pagesA Feasibility Study For A Cleaning CompanyRogerNo ratings yet

- 171 Value Proposition CanvassDocument2 pages171 Value Proposition CanvassNaruto UzumakiNo ratings yet

- Pre-Money Valuation: Multiple ApproachDocument16 pagesPre-Money Valuation: Multiple ApproachDavid ChikhladzeNo ratings yet

- L8 Raising CapitalDocument26 pagesL8 Raising CapitalKranthi ManthriNo ratings yet

- NPV and IRRDocument7 pagesNPV and IRRWondim GenetNo ratings yet

- Marketing Aspect: Learning OutcomesDocument23 pagesMarketing Aspect: Learning OutcomesKristine Lirose BordeosNo ratings yet

- Ch1 - Management of Technology - An OverviewDocument36 pagesCh1 - Management of Technology - An OverviewMuhd ShaddetnyNo ratings yet

- Forecasting Cases Final 1Document43 pagesForecasting Cases Final 1Vipul SinghNo ratings yet

- Case: Feuture, Inc.: Far Eastern UniversityDocument11 pagesCase: Feuture, Inc.: Far Eastern UniversityAmro Ahmed RazigNo ratings yet

- Lucio, Mary-Ann Grace S. Real-World FocusDocument2 pagesLucio, Mary-Ann Grace S. Real-World FocusGrace SimonNo ratings yet

- Yahoo! Inc. Valuation ProjectDocument8 pagesYahoo! Inc. Valuation ProjectNigar_AbbasNo ratings yet

- Solved Forecasting The Success of New Product Introductions Is Notoriously DifficultDocument1 pageSolved Forecasting The Success of New Product Introductions Is Notoriously DifficultM Bilal SaleemNo ratings yet

- Goal SseekDocument5 pagesGoal SseekFilip NikolovskiNo ratings yet

- Case Study 4 STMicroelectronics - TQM Implementation and Policy Deployment Cua To DayDocument10 pagesCase Study 4 STMicroelectronics - TQM Implementation and Policy Deployment Cua To DayMy NguyễnNo ratings yet

- Technological Institute of The PhilippinesDocument31 pagesTechnological Institute of The PhilippinesEUNICE ANGELA LASCONIANo ratings yet

- Valuing Private Companies:: Factors and Approaches To ConsiderDocument35 pagesValuing Private Companies:: Factors and Approaches To ConsiderAvinash DasNo ratings yet

- Sonali Bank CSRDocument16 pagesSonali Bank CSRUSHA IT100% (1)

- Forecasting PDFDocument69 pagesForecasting PDFSuba NitaNo ratings yet

- Equivalent Annual AnnuityDocument10 pagesEquivalent Annual Annuitymohsin_ali07428097No ratings yet

- Capital Budgeting 55Document54 pagesCapital Budgeting 55Hitesh Jain0% (1)

- Chapter 13 ValuationDocument23 pagesChapter 13 ValuationIndah Dwi RetnoNo ratings yet

- Lecture 7 (Financial Analysis Section 2) RevisedDocument35 pagesLecture 7 (Financial Analysis Section 2) RevisedHari SharmaNo ratings yet

- The Time Value of MoneyDocument66 pagesThe Time Value of MoneyrachealllNo ratings yet

- Stock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaDocument40 pagesStock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaJOHN PAOLO EVORANo ratings yet

- RC Equity Research Report Essentials CFA InstituteDocument3 pagesRC Equity Research Report Essentials CFA InstitutetheakjNo ratings yet

- Ratio AnalysisDocument33 pagesRatio AnalysisJhagantini PalaniveluNo ratings yet

- Capital Budgeting & Decision...Document3 pagesCapital Budgeting & Decision...Ajit Mohan DasNo ratings yet

- 2023 Article 688Document13 pages2023 Article 688Ariandindi AriandiNo ratings yet

- LTE UE Power Consumption Model PDFDocument5 pagesLTE UE Power Consumption Model PDFNikNo ratings yet

- Article 7 TG October December 2020 Ms ChitraSharma DR Shaifali Full1036Document5 pagesArticle 7 TG October December 2020 Ms ChitraSharma DR Shaifali Full1036Putri Azzahra Salsabila putriazzahra.2019No ratings yet

- 11 Biology - Test Maker @Document1 page11 Biology - Test Maker @Waleed AnsariNo ratings yet

- MeasurIT Flexim ADM6725 Application Water Consumption Bottling Line 0809Document1 pageMeasurIT Flexim ADM6725 Application Water Consumption Bottling Line 0809cwiejkowskaNo ratings yet

- MIDTERMDocument6 pagesMIDTERMLiana XudabaxshyanNo ratings yet

- T M P S R P C: He Anagement of Ublic Ector Ecords: Rinciples and OntextDocument161 pagesT M P S R P C: He Anagement of Ublic Ector Ecords: Rinciples and OntextSaiful QazaNo ratings yet

- What Is DesulfurizationDocument20 pagesWhat Is DesulfurizationYash NandurkarNo ratings yet

- NJRSF Poster 2020Document2 pagesNJRSF Poster 2020api-502690136No ratings yet

- E 1067 TestDocument12 pagesE 1067 Testpandi007No ratings yet

- Flow Control Valve Serial Number PDFDocument3 pagesFlow Control Valve Serial Number PDFusman khanNo ratings yet

- Pak Matiari-Lahore Transmission Company (Private) LimitedDocument4 pagesPak Matiari-Lahore Transmission Company (Private) LimitedAftab Ejaz QureshiNo ratings yet

- Material Transfer Agreement FormDocument2 pagesMaterial Transfer Agreement FormFritz CarpenteroNo ratings yet

- Quick Start Guide: What You GetDocument8 pagesQuick Start Guide: What You GetAle NietoNo ratings yet

- Fundamentals SyllabusDocument12 pagesFundamentals SyllabusRoy CabarlesNo ratings yet

- Data Sheet Milk Reception Unit.1 enDocument2 pagesData Sheet Milk Reception Unit.1 enBoricean Gheorghita100% (1)

- Committee of Permanent Representatives To Asean in JakartaDocument1 pageCommittee of Permanent Representatives To Asean in Jakartamiharbi cortezNo ratings yet

- How To Resolve Costing ErrorsDocument38 pagesHow To Resolve Costing ErrorsNathanNo ratings yet

- NG Rtgs Ver 16th June14Document3 pagesNG Rtgs Ver 16th June14Supreeth SharmaNo ratings yet

- Brazing RiskDocument2 pagesBrazing Riskanon_12627423No ratings yet

- What Is A Share or Stock?Document12 pagesWhat Is A Share or Stock?Vicky MbaNo ratings yet

- Essay The Government Has No Business Being in BusinessDocument2 pagesEssay The Government Has No Business Being in BusinessNikhil Johri100% (1)

- Job Application Email PracticeDocument1 pageJob Application Email PracticeGilda MoNo ratings yet

- ExpectationsDocument11 pagesExpectationsapi-341254245No ratings yet

- 8.12 Live DinieDocument24 pages8.12 Live DinieAdiff CxainzNo ratings yet

- East West Pesticide and Fungicide ListDocument10 pagesEast West Pesticide and Fungicide ListnormanwillowNo ratings yet

- SRF060424 03Document18 pagesSRF060424 03nailgrpNo ratings yet

- FABM 112 Week 1 9 LegitDocument9 pagesFABM 112 Week 1 9 Legitjean heidi espinas25% (4)

- The Millennium Park Bus DepotDocument2 pagesThe Millennium Park Bus DepotSaiRajuNo ratings yet