You might also like

- Management - BLGF - ELSP HandoutDocument112 pagesManagement - BLGF - ELSP HandoutNash A. Dugasan100% (1)

- Date: Decenober 4,: RudgerDocument9 pagesDate: Decenober 4,: RudgerRaine Buenaventura-EleazarNo ratings yet

- Coordinating and Communicating Local Treasury Matters With StakeholdersDocument38 pagesCoordinating and Communicating Local Treasury Matters With Stakeholdersbull jack75% (4)

- DAMA 01 IntroductionDocument27 pagesDAMA 01 IntroductionAlgen S. GomezNo ratings yet

- Local Budget Process GuideDocument22 pagesLocal Budget Process GuideNash A. Dugasan100% (3)

- GR NO 179155 Lozada Vs Bracewell Et AlDocument5 pagesGR NO 179155 Lozada Vs Bracewell Et AlNash A. DugasanNo ratings yet

- ICLTE-A.1-Data Analytics - Investment Programming and FRMDocument31 pagesICLTE-A.1-Data Analytics - Investment Programming and FRMNash A. Dugasan100% (1)

- ICLTE-C.3-Public Expenditure MGT & Financial Accountability - Local Funds Management and UtilizationDocument84 pagesICLTE-C.3-Public Expenditure MGT & Financial Accountability - Local Funds Management and UtilizationNash A. DugasanNo ratings yet

- GR NO 180027 Republic Vs Santos Et AlDocument5 pagesGR NO 180027 Republic Vs Santos Et AlNash A. DugasanNo ratings yet

- ICLTE-B.1-Strategic ResMob - Understanding LGU Credit Financing and Debt ManagementDocument33 pagesICLTE-B.1-Strategic ResMob - Understanding LGU Credit Financing and Debt ManagementNash A. DugasanNo ratings yet

- Supreme Court Rules in Favor of Landowner in Property Registration CaseDocument7 pagesSupreme Court Rules in Favor of Landowner in Property Registration CaseNash A. DugasanNo ratings yet

- Republic of The Philippines Department of Social Welfare and DevelopmentDocument36 pagesRepublic of The Philippines Department of Social Welfare and DevelopmentNash A. DugasanNo ratings yet

- GR NO 167707 Secretary of DENR Vs Yap Et AlDocument12 pagesGR NO 167707 Secretary of DENR Vs Yap Et AlNash A. DugasanNo ratings yet

- GR NO 166748 Hermoso Vs CADocument7 pagesGR NO 166748 Hermoso Vs CANash A. DugasanNo ratings yet

- GR NO 170757 Valiao Vs RepublicDocument4 pagesGR NO 170757 Valiao Vs RepublicNash A. DugasanNo ratings yet

- GR NO 157485 Republic Vs Heirs of Sin Et AlDocument6 pagesGR NO 157485 Republic Vs Heirs of Sin Et AlNash A. DugasanNo ratings yet

- GR NO 166748 Hermoso Vs CADocument7 pagesGR NO 166748 Hermoso Vs CANash A. DugasanNo ratings yet

- RDO No. 3 - San Fernando City, La UnionDocument1,698 pagesRDO No. 3 - San Fernando City, La UnionNash A. Dugasan100% (1)

- GR NO 134209 Republic Vs NaguiatDocument3 pagesGR NO 134209 Republic Vs NaguiatNash A. DugasanNo ratings yet

- GR NO 135385 Cruz Et Al Vs Secretary of DENR Et AlDocument93 pagesGR NO 135385 Cruz Et Al Vs Secretary of DENR Et AlNash A. DugasanNo ratings yet

- v1 (Redacted) Advisory Opinion No. 2019-023Document4 pagesv1 (Redacted) Advisory Opinion No. 2019-023Nash A. DugasanNo ratings yet

- April 11 2020 6PM APOR654731141Document12 pagesApril 11 2020 6PM APOR654731141Nash A. DugasanNo ratings yet

- GR NO 107751 Ligon Vs CADocument3 pagesGR NO 107751 Ligon Vs CANash A. DugasanNo ratings yet

- Heirs of Pedro Palanca win land caseDocument6 pagesHeirs of Pedro Palanca win land caseNash A. DugasanNo ratings yet

- COA Resolution on Qualification StandardsDocument3 pagesCOA Resolution on Qualification StandardsKelee100% (1)

- LEBMO No.1Document83 pagesLEBMO No.1Marian Chavez75% (8)

- Provincial Advisory-14-Additional-Essential-BusinessDocument3 pagesProvincial Advisory-14-Additional-Essential-BusinessNash A. DugasanNo ratings yet

- Lgu Plaridel Bulacan Jan 11 2019Document7 pagesLgu Plaridel Bulacan Jan 11 2019Nash A. DugasanNo ratings yet

- Ecology and Ecological ProblemsDocument68 pagesEcology and Ecological ProblemsNash A. DugasanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- E - Banking in IndiaDocument52 pagesE - Banking in IndiaYatriShah100% (1)

- Dynamics GP 2010 Table ListDocument159 pagesDynamics GP 2010 Table ListIsaac Namukoa100% (1)

- Statistical Analysis of The Exchange Rate of Bitcoin: Jeffrey Chu, Saralees Nadarajah, Stephen ChanDocument27 pagesStatistical Analysis of The Exchange Rate of Bitcoin: Jeffrey Chu, Saralees Nadarajah, Stephen Chanugoala brightNo ratings yet

- Icc 400 / 500 / 600Document9 pagesIcc 400 / 500 / 600Sayaga Globalindo100% (15)

- Assainment of Online BankingDocument21 pagesAssainment of Online BankingMOHAMMAD SAIFUL ISLAM100% (1)

- All About CreditDocument4 pagesAll About CreditShaira VeronicaNo ratings yet

- Bank of Philippine Islands vs Intermediate CourtDocument2 pagesBank of Philippine Islands vs Intermediate CourtJohnny EnglishNo ratings yet

- May 2020 credit card statement summaryDocument2 pagesMay 2020 credit card statement summaryMark WilliamsNo ratings yet

- Account Summary Payment Information: New Balance $135.86Document6 pagesAccount Summary Payment Information: New Balance $135.86thinh thanh100% (2)

- Microsoft Dynamics NAV 2013 - 80434 - Fixed AssetsDocument306 pagesMicrosoft Dynamics NAV 2013 - 80434 - Fixed AssetsRamin MarghiNo ratings yet

- ICC 400/600 Agreement Protects Buyer & Seller FeesDocument6 pagesICC 400/600 Agreement Protects Buyer & Seller Feesfabio ramirez mancholaNo ratings yet

- Tally ERP 9.0 Material Basics of Accounting 01Document10 pagesTally ERP 9.0 Material Basics of Accounting 01Raghavendra yadav KM100% (1)

- Consumers' Attitude Towards Credit Cards: An Empirical StudyDocument19 pagesConsumers' Attitude Towards Credit Cards: An Empirical Studyprincy goyalNo ratings yet

- Class 7 NotesDocument66 pagesClass 7 NotestimckjkjdfdNo ratings yet

- Interpreter Bulletin 038 - Capital OneDocument3 pagesInterpreter Bulletin 038 - Capital OnehiepwinNo ratings yet

- 2015 Guardian Angel Knitting BookDocument12 pages2015 Guardian Angel Knitting BookManicNo ratings yet

- Frequently Asked Questions: RewardDocument6 pagesFrequently Asked Questions: RewardSuhailShaikhNo ratings yet

- Executive Summary My ReportDocument1 pageExecutive Summary My ReportNirob Hasan VoorNo ratings yet

- RBC Visa Classic: Low Rate OptionDocument4 pagesRBC Visa Classic: Low Rate OptionThe VaultNo ratings yet

- Dialogue Credit CardDocument3 pagesDialogue Credit CardHILDA ADHITYA NINGSIHNo ratings yet

- Individual Pricing PDFDocument14 pagesIndividual Pricing PDFKapone TälentNo ratings yet

- III. Central Banks and Payments in The Digital EraDocument30 pagesIII. Central Banks and Payments in The Digital EraForkLogNo ratings yet

- E - CommerceDocument9 pagesE - CommerceVishal Kumar ShawNo ratings yet

- Uganda Martyrs ERD for Daycare ManagementTITLE FastFlight Airlines Flight Reservation ERD TITLE Online Auction Site EERD ModelTITLE Baseball League Database ERDDocument2 pagesUganda Martyrs ERD for Daycare ManagementTITLE FastFlight Airlines Flight Reservation ERD TITLE Online Auction Site EERD ModelTITLE Baseball League Database ERDmusokedaudiNo ratings yet

- SFAC No 7Document41 pagesSFAC No 7Sophia Febriyani SimarmataNo ratings yet

- LiquidityDocument26 pagesLiquidityPallavi RanjanNo ratings yet

- Capital Vs Revenue TransactionsDocument24 pagesCapital Vs Revenue TransactionsShruti KapoorNo ratings yet

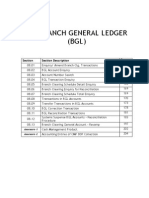

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- LogistrixDocument19 pagesLogistrixAnthony StevenNo ratings yet

- Activity 2 - Analysis of Business TransactionDocument4 pagesActivity 2 - Analysis of Business Transactionjay100% (1)