You might also like

- Continuous Improvement Policy and ProcedureDocument3 pagesContinuous Improvement Policy and ProcedureCandiceNo ratings yet

- GMCC Rotary Compressor Manual Provides Technical DetailsDocument24 pagesGMCC Rotary Compressor Manual Provides Technical Detailsyeancarlo sequera0% (1)

- Financial Management:: The Cost of CapitalDocument94 pagesFinancial Management:: The Cost of CapitalSarah SaluquenNo ratings yet

- Solutions Nss NC 11Document19 pagesSolutions Nss NC 11saadullahNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument29 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte ChanNo ratings yet

- Product Recall SOPDocument3 pagesProduct Recall SOPvioletaflora81% (16)

- 08 - Chapter 8Document71 pages08 - Chapter 8hunkieNo ratings yet

- Modigliani Miller TheoremDocument4 pagesModigliani Miller TheoremmeetwithsanjayNo ratings yet

- Project Financials with Prospective AnalysisDocument34 pagesProject Financials with Prospective AnalysisAzhar SeptariNo ratings yet

- Stress Testing ProjectDocument28 pagesStress Testing Projectjeetu998800No ratings yet

- ElectricityDocument1 pageElectricityDarge GmentizaNo ratings yet

- Cost of capital analysis for Stansted AirportDocument37 pagesCost of capital analysis for Stansted AirportJames HoldenNo ratings yet

- IPPTChap005 (The Production Process and Costs)Document42 pagesIPPTChap005 (The Production Process and Costs)Ryan Hegar SuryadinathaNo ratings yet

- Chapter OneDocument18 pagesChapter OneBelsti AsresNo ratings yet

- EPGP-11 Sec B - LCA - Marriott - EPGP-11-153Document8 pagesEPGP-11 Sec B - LCA - Marriott - EPGP-11-153Chaitanya RavankarNo ratings yet

- L2 Efficient Capital Markets CH14Document25 pagesL2 Efficient Capital Markets CH14TenkaNo ratings yet

- Accounting For ManagersDocument286 pagesAccounting For ManagersSatyam Rastogi100% (1)

- Core Principles and Applications of Corporate Finance: Stephen A. RossDocument12 pagesCore Principles and Applications of Corporate Finance: Stephen A. RossAHMED MOHAMED YUSUFNo ratings yet

- ICPAP Advanced Management AccountingDocument326 pagesICPAP Advanced Management Accountingelite76100% (2)

- Influencer Marketing GuideDocument23 pagesInfluencer Marketing GuideInfo e AnaliseNo ratings yet

- Customer Profitability AnalysisDocument1 pageCustomer Profitability AnalysisAdrianaNo ratings yet

- Financial Management:: Stock ValuationDocument57 pagesFinancial Management:: Stock ValuationSarah SaluquenNo ratings yet

- Financial Management:: Investment Decision CriteriaDocument96 pagesFinancial Management:: Investment Decision CriteriaBen OusoNo ratings yet

- Financial Management:: Risk and Return - Capital Market TheoryDocument56 pagesFinancial Management:: Risk and Return - Capital Market TheoryBen OusoNo ratings yet

- Group 5 Weekly Task Accounting Theory 11th Meeting A Brief Review of Cost Allocation MethodDocument6 pagesGroup 5 Weekly Task Accounting Theory 11th Meeting A Brief Review of Cost Allocation MethodEggie Auliya HusnaNo ratings yet

- Mployee Stakeholders and Workplace IssuesDocument25 pagesMployee Stakeholders and Workplace IssuesAlexander Agung HRDNo ratings yet

- Financial Management:: An Introduction To Risk and Return - History of Financial Market ReturnsDocument69 pagesFinancial Management:: An Introduction To Risk and Return - History of Financial Market ReturnsBen OusoNo ratings yet

- NPV and investment criteria for acquiring NorthGate MineralsDocument30 pagesNPV and investment criteria for acquiring NorthGate MineralsAkash TalwarNo ratings yet

- Final Thesis IntanDocument77 pagesFinal Thesis IntanKarina RusmanNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument40 pagesFinancial Statement Analysis: K R Subramanyam John J WildEmma SuryaniNo ratings yet

- Besley 14e ch08Document48 pagesBesley 14e ch08ljismeok80% (5)

- Titman PPT CH18Document79 pagesTitman PPT CH18IKA RAHMAWATINo ratings yet

- ACCT504 Case Study 3 Cash BudgetingDocument2 pagesACCT504 Case Study 3 Cash BudgetingtiburonlynnNo ratings yet

- 13 Capital Structure (Slides) by Zubair Arshad PDFDocument34 pages13 Capital Structure (Slides) by Zubair Arshad PDFZubair ArshadNo ratings yet

- Factors Influencing Effective Debt Collection of Yoma BankDocument65 pagesFactors Influencing Effective Debt Collection of Yoma BankkringNo ratings yet

- Pengaruh Employee Stock Ownership Program (ESOP) Dan Leverage Terhadap Kinerja Keuangan PDFDocument8 pagesPengaruh Employee Stock Ownership Program (ESOP) Dan Leverage Terhadap Kinerja Keuangan PDFDio ChandraNo ratings yet

- Chapter 1: The Investment Environment: Problem SetsDocument6 pagesChapter 1: The Investment Environment: Problem SetsMehrab Jami Aumit 1812818630No ratings yet

- Factors Influencing The Effectiveness of Internal Audit On Organizational PerformanceDocument8 pagesFactors Influencing The Effectiveness of Internal Audit On Organizational PerformanceIjaems JournalNo ratings yet

- Chapter-10 Market Risk Math Problems and SolutionsDocument6 pagesChapter-10 Market Risk Math Problems and SolutionsruponNo ratings yet

- TUGAS KELOMPOK AKUNTANSI MANAJEMEN / LDocument3 pagesTUGAS KELOMPOK AKUNTANSI MANAJEMEN / LMuhammad Rizki NoorNo ratings yet

- Designing A Capital StructureDocument16 pagesDesigning A Capital StructureDHARMA DAZZLE100% (1)

- Hansen AISE IM Ch07Document54 pagesHansen AISE IM Ch07AimanNo ratings yet

- Risk Management FundamentalsDocument21 pagesRisk Management FundamentalsAjay Chauhan100% (1)

- Capital Budgeting Narain NotesDocument35 pagesCapital Budgeting Narain NoteskrishanptfmsNo ratings yet

- Entrepreneurship: Successfully Launching New Ventures: Feasibility AnalysisDocument5 pagesEntrepreneurship: Successfully Launching New Ventures: Feasibility Analysisziyad albednah100% (1)

- Pepsi and Coke Financial ManagementDocument11 pagesPepsi and Coke Financial ManagementNazish Sohail100% (1)

- Understanding Financial StatementsDocument103 pagesUnderstanding Financial StatementsLawa LopezNo ratings yet

- Chapter 8 Producing Quality Goods and ServicesDocument24 pagesChapter 8 Producing Quality Goods and ServicesPete JoempraditwongNo ratings yet

- Financial Management:: The Time Value of Money-The BasicsDocument67 pagesFinancial Management:: The Time Value of Money-The Basicsfreakguy 313No ratings yet

- Theoretical FrameworkDocument3 pagesTheoretical Frameworkm_ihamNo ratings yet

- Capital Investment DecisionsDocument20 pagesCapital Investment Decisionsmubasheralijamro0% (1)

- Financial ManagementDocument191 pagesFinancial ManagementJohn SamonteNo ratings yet

- Financial Management SummaryDocument3 pagesFinancial Management SummaryChristoph MagistraNo ratings yet

- Kieso - IFRS - ch11 - IfRS (Depreciation, Impairments, and Depletion)Document73 pagesKieso - IFRS - ch11 - IfRS (Depreciation, Impairments, and Depletion)Muzi RahayuNo ratings yet

- CH 5Document69 pagesCH 5Chang Chan Chong100% (1)

- Strategic Finance Assignment CalculatorDocument6 pagesStrategic Finance Assignment CalculatorSOHAIL TARIQNo ratings yet

- Critical Analysis of Nigeria's BVN Project and RecommendationsDocument13 pagesCritical Analysis of Nigeria's BVN Project and RecommendationsOwolabi PetersNo ratings yet

- Chapter 07 Positive Accounting TheoryDocument15 pagesChapter 07 Positive Accounting Theorymehrabshawn75% (4)

- Arens Auditing C13e PPT Ch01Document17 pagesArens Auditing C13e PPT Ch01MeowNo ratings yet

- Capital Structure Basic ConceptsDocument25 pagesCapital Structure Basic ConceptsisratzamananuNo ratings yet

- Product Costing & Segment ReportingDocument2 pagesProduct Costing & Segment ReportingLovely De CastroNo ratings yet

- TKM CH 13Document102 pagesTKM CH 13Marriz TanNo ratings yet

- Capital Budgeting Risk AnalysisDocument39 pagesCapital Budgeting Risk AnalysisJulia Ciarra PeraltaNo ratings yet

- Merged Notes - FM-2Document11 pagesMerged Notes - FM-2KushalNo ratings yet

- Chapter 11 (Investment Decicions) Class 1Document75 pagesChapter 11 (Investment Decicions) Class 1wstNo ratings yet

- Capital Budgeting: A Brief OverviewDocument14 pagesCapital Budgeting: A Brief OverviewJanica BerbaNo ratings yet

- Financial Management:: Analyzing Project Cash FlowsDocument70 pagesFinancial Management:: Analyzing Project Cash FlowsSarah SaluquenNo ratings yet

- Financial Management:: Stock ValuationDocument57 pagesFinancial Management:: Stock ValuationSarah SaluquenNo ratings yet

- Financial Management:: Risk Analysis and Project EvaluationDocument79 pagesFinancial Management:: Risk Analysis and Project EvaluationSarah SaluquenNo ratings yet

- C11Document51 pagesC11Sarah SaluquenNo ratings yet

- Rizal Technological University College of EducationDocument1 pageRizal Technological University College of EducationSarah SaluquenNo ratings yet

- Case of The Unidentified IndustriesDocument2 pagesCase of The Unidentified IndustriesNishanth K SNo ratings yet

- Rizal Technological University College of EducationDocument1 pageRizal Technological University College of EducationSarah SaluquenNo ratings yet

- ch12Document32 pagesch12Ara E. Caballero100% (1)

- Rail Kit FabricationDocument1 pageRail Kit FabricationSarah SaluquenNo ratings yet

- Case of The Unidentified IndustriesDocument2 pagesCase of The Unidentified IndustriesNishanth K SNo ratings yet

- Brochure - Attom - Smoothair In-Row Cooling PDFDocument16 pagesBrochure - Attom - Smoothair In-Row Cooling PDFSarah SaluquenNo ratings yet

- Chcolate Project - Five BrandsDocument46 pagesChcolate Project - Five BrandsNitinAgnihotriNo ratings yet

- Passenger Terminal Expansion Works Materials CatalogueDocument82 pagesPassenger Terminal Expansion Works Materials CatalogueMariam MousaNo ratings yet

- Service Quality in The Retail Banking Sector-A Study of Selected Public and New Indian Private Sector Banks in IndiaDocument7 pagesService Quality in The Retail Banking Sector-A Study of Selected Public and New Indian Private Sector Banks in IndiaSowmya Reddy ReddyNo ratings yet

- 20 BCD7263 Sam AltmanDocument32 pages20 BCD7263 Sam Altmananunay.20bcd7263No ratings yet

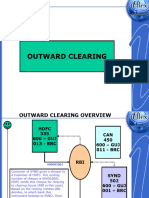

- 5-SETTLEMENT-Outward Clearing 1Document21 pages5-SETTLEMENT-Outward Clearing 1ola.cloudsNo ratings yet

- Assignment: Financial Management Unit 1Document2 pagesAssignment: Financial Management Unit 1sachinNo ratings yet

- Othm Report Unit 1.Document16 pagesOthm Report Unit 1.PRG ARMYNo ratings yet

- Test Bank For Marketing For Hospitality and Tourism 6Th Edition Kotler Bowen Makens 0132784025 9780132784023 Full Chapter PDFDocument28 pagesTest Bank For Marketing For Hospitality and Tourism 6Th Edition Kotler Bowen Makens 0132784025 9780132784023 Full Chapter PDFjenny.goyco725100% (11)

- Plant GM with 15+ Years Operations ExperienceDocument6 pagesPlant GM with 15+ Years Operations ExperiencemohammedNo ratings yet

- BASF - Rebranding Old Vs New Names - 2011-10-07 V5Document2 pagesBASF - Rebranding Old Vs New Names - 2011-10-07 V5Valentina PangayomanNo ratings yet

- Agm Compliance ChecklistDocument3 pagesAgm Compliance ChecklistAkshay kumar Mishra100% (1)

- Assignment Taxation 2Document13 pagesAssignment Taxation 2afiq hisyamNo ratings yet

- V - 62 Caroni, Trinidad, Tuesday 14th March, 2023-Price $1.00 N - 39Document17 pagesV - 62 Caroni, Trinidad, Tuesday 14th March, 2023-Price $1.00 N - 39ERSKINE LONEYNo ratings yet

- Confide Ntial: Sale and Purchase AgreementDocument6 pagesConfide Ntial: Sale and Purchase AgreementJake Joan PasculadoNo ratings yet

- Trading gold and forex with an initial capital of 3000Document18 pagesTrading gold and forex with an initial capital of 3000SơnNamNo ratings yet

- Distribution Network For BritanniaDocument5 pagesDistribution Network For BritanniaSaba Dabir100% (3)

- Restaurant Feasibility ReportDocument7 pagesRestaurant Feasibility ReportJoneric RamosNo ratings yet

- Marks and Spencer: A Retail HistoryDocument11 pagesMarks and Spencer: A Retail HistorysteffijasperNo ratings yet

- PM2 Motor List: View Motors Serviced and Stored in PM2 AreaDocument44 pagesPM2 Motor List: View Motors Serviced and Stored in PM2 AreaMohd A IshakNo ratings yet

- FAC11A1Document9 pagesFAC11A1sacey20.hbNo ratings yet

- Introduction To Research Methods A Hands On Approach 1st Edition Pajo Test BankDocument12 pagesIntroduction To Research Methods A Hands On Approach 1st Edition Pajo Test Bankethelbertsangffz100% (30)

- Portfolio Management GuideDocument13 pagesPortfolio Management GuideRicha KumariNo ratings yet

- Personal Branding Persevering Towards Success Leza KlenkDocument13 pagesPersonal Branding Persevering Towards Success Leza KlenkPrabhuNo ratings yet

- Fast Fulfillment: The Machine That Changed RetailingDocument40 pagesFast Fulfillment: The Machine That Changed RetailingCharlene Kronstedt0% (1)

- 3 Day Tour Package Costing SheetDocument4 pages3 Day Tour Package Costing SheetRica Marie BarbenNo ratings yet