You might also like

- Asset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceFrom EverandAsset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceNo ratings yet

- Risk and Managerial Options in Capital BudgetingDocument43 pagesRisk and Managerial Options in Capital BudgetingShan amirNo ratings yet

- CH 14Document43 pagesCH 14Imran AliNo ratings yet

- Option in Cap. BudDocument26 pagesOption in Cap. BudHassan KhanNo ratings yet

- Risk and Managerial (Real) Options in Capital Budgeting Risk and Managerial (Real) Options in Capital BudgetingDocument42 pagesRisk and Managerial (Real) Options in Capital Budgeting Risk and Managerial (Real) Options in Capital BudgetingAhmed El KhateebNo ratings yet

- Risk and Managerial (Real) Options in Capital BudgetingDocument40 pagesRisk and Managerial (Real) Options in Capital BudgetingRaazia ImranNo ratings yet

- A-09.21.051 D .NAKUL Holmes BFDocument14 pagesA-09.21.051 D .NAKUL Holmes BFAustin GomesNo ratings yet

- 05 Park ISM ch05 PDFDocument39 pages05 Park ISM ch05 PDFBenn DoucetNo ratings yet

- A3 Capital Budgeting Jose Solivan v1Document3 pagesA3 Capital Budgeting Jose Solivan v1Jose Javier Solivan RiveraNo ratings yet

- L12: Actual and Constant DollarsDocument11 pagesL12: Actual and Constant DollarsSajid IqbalNo ratings yet

- This Study Resource Was: ANSWER KEY (Additional Problems On Operating Exposure)Document3 pagesThis Study Resource Was: ANSWER KEY (Additional Problems On Operating Exposure)SriSaraswathyNo ratings yet

- AFN Equation and Financial StatementDocument4 pagesAFN Equation and Financial StatementWawex DavisNo ratings yet

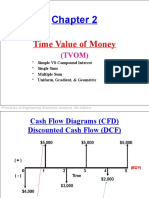

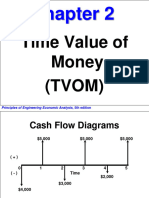

- Time Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th EditionDocument96 pagesTime Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th EditionnorahNo ratings yet

- The Partnership of Undoy, Vennie and Wally Was Dissolved On June 30, 2005 and Account Balances After Non-Cash Assets Were Converted Into Cash OnDocument7 pagesThe Partnership of Undoy, Vennie and Wally Was Dissolved On June 30, 2005 and Account Balances After Non-Cash Assets Were Converted Into Cash OnToni MarquezNo ratings yet

- Akmen Chapter 13 KadishaDocument5 pagesAkmen Chapter 13 Kadishakidus.gaming52No ratings yet

- TutDocument2 pagesTutElzubair EljaaliNo ratings yet

- Chapter 2Document14 pagesChapter 2Kumar ShivamNo ratings yet

- CH2 - Time Value of Money IDocument56 pagesCH2 - Time Value of Money IAjlan AlajlanNo ratings yet

- Assignment 4 - Contemporary Engineering BookDocument9 pagesAssignment 4 - Contemporary Engineering BookDhiraj NayakNo ratings yet

- Cla 22222222 FinanceDocument21 pagesCla 22222222 FinanceSneha MaharjanNo ratings yet

- This Spreadsheet Supports STUDENT Analysis of The Cases "Ballis's Benchmark (A) and (B) " (UVA-F-1621 and UVA-F-1622)Document6,049 pagesThis Spreadsheet Supports STUDENT Analysis of The Cases "Ballis's Benchmark (A) and (B) " (UVA-F-1621 and UVA-F-1622)Arbaaz MahmoodNo ratings yet

- Incremental Analysis: Lecture No. 21 Professor C. S. Park Fundamentals of Engineering EconomicsDocument21 pagesIncremental Analysis: Lecture No. 21 Professor C. S. Park Fundamentals of Engineering EconomicsNivika TiffanyNo ratings yet

- Oper&Scm SupaDocument58 pagesOper&Scm Supa장현우No ratings yet

- 2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 2 (Part 2)Document5 pages2020 Sem 1 ACC10007 Discussion Questions (And Solutions) - Topic 2 (Part 2)Renee WongNo ratings yet

- Evaluate Earth Mover AcquisitionDocument2 pagesEvaluate Earth Mover AcquisitionMohNo ratings yet

- Chapter 05Document26 pagesChapter 05slee11829% (7)

- Chap 018Document27 pagesChap 018Nazifah100% (1)

- Ch. 9 Money Creation by Topic Past Paper Marking SchemeDocument3 pagesCh. 9 Money Creation by Topic Past Paper Marking SchemeyanaaNo ratings yet

- ISEN 667 Engineering Economic Analysis: Class 02. Cash Flow and Interest CalculationDocument58 pagesISEN 667 Engineering Economic Analysis: Class 02. Cash Flow and Interest Calculationharish shanbhagNo ratings yet

- Financial Planning and ForecastingDocument25 pagesFinancial Planning and ForecastingAhsan100% (2)

- Deferred Financing-BOC Presentation Aug 19 2009-FINALDocument19 pagesDeferred Financing-BOC Presentation Aug 19 2009-FINALsmf 4LAKidsNo ratings yet

- Risk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPM / SMLDocument31 pagesRisk and Rates of Return: Stand-Alone Risk Portfolio Risk Risk & Return: CAPM / SMLArslan QayyumNo ratings yet

- Assigment 4 SolutionDocument2 pagesAssigment 4 SolutionRamy ShabanaNo ratings yet

- Study Questions For IE305 Miderm IDocument4 pagesStudy Questions For IE305 Miderm IArif Berk GARİPNo ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)Document4 pagesNanyang Business School AB1201 Financial Management Tutorial 8: The Basics of Capital Budgeting (Common Questions)asdsadsaNo ratings yet

- 7110 Principles of Accounts: MARK SCHEME For The October/November 2012 SeriesDocument7 pages7110 Principles of Accounts: MARK SCHEME For The October/November 2012 SeriesJě Sűis KëShNo ratings yet

- ACCT510 Week1 SolvedProblemsDocument11 pagesACCT510 Week1 SolvedProblemsdoctornazNo ratings yet

- The Basics of Capital Budgeting: Net Present ValueDocument10 pagesThe Basics of Capital Budgeting: Net Present ValueNIVETHIKHA RAVICHANDRANNo ratings yet

- Practice Questions 1 and 2 ReviewDocument8 pagesPractice Questions 1 and 2 ReviewHashani KumarasingheNo ratings yet

- Capital BudgetingDocument25 pagesCapital BudgetingPhuntru PhiNo ratings yet

- 10 Non-Current AssetsDocument25 pages10 Non-Current AssetsDayaan ANo ratings yet

- Question #1: Jordan Enterprises Raw MaterialDocument35 pagesQuestion #1: Jordan Enterprises Raw MaterialAimen sakimdadNo ratings yet

- Class 1 - SolutionsDocument2 pagesClass 1 - SolutionsMCamilleNo ratings yet

- Time Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th EditionDocument154 pagesTime Value of Money (TVOM) : Principles of Engineering Economic Analysis, 5th Editionmohammed alqNo ratings yet

- Question 1Document10 pagesQuestion 1Aqsa AnumNo ratings yet

- 7110 Principles of Accounts: MARK SCHEME For The May/June 2010 Question Paper For The Guidance of TeachersDocument7 pages7110 Principles of Accounts: MARK SCHEME For The May/June 2010 Question Paper For The Guidance of TeachersArumugam ManickamNo ratings yet

- 2 - Breakeven Analysis & Decision Trees PDFDocument35 pages2 - Breakeven Analysis & Decision Trees PDFRajat AgrawalNo ratings yet

- Chapter 2 Principles of Corporate Finance PDFDocument4 pagesChapter 2 Principles of Corporate Finance PDFchatuuuu123No ratings yet

- NPV Calculation and Project EvaluationDocument2 pagesNPV Calculation and Project EvaluationAtiqullah sherzadNo ratings yet

- EE - Assignment Chapter 9-10 SolutionDocument11 pagesEE - Assignment Chapter 9-10 SolutionXuân ThànhNo ratings yet

- CourseheroDocument2 pagesCourseheroSharjaaah50% (2)

- Chap09 Tutorial AnsDocument9 pagesChap09 Tutorial AnsSong PhươngNo ratings yet

- Principles of Corporate Finance 10th Edition Brealey Solutions ManualDocument25 pagesPrinciples of Corporate Finance 10th Edition Brealey Solutions ManualJacquelineHillqtbs98% (57)

- PDF PDFDocument7 pagesPDF PDFMikey MadRatNo ratings yet

- Whastapp AssgnmDocument9 pagesWhastapp AssgnmSyed Zeeshan ArshadNo ratings yet

- Payback Period Year Cash Flows Cumulative Cash FlowsDocument8 pagesPayback Period Year Cash Flows Cumulative Cash Flowsfarhann JattNo ratings yet

- Minggu 2 - 3 - Time Value of MoneyDocument79 pagesMinggu 2 - 3 - Time Value of MoneylisdhiyantoNo ratings yet

- Group 8 Capital BudgetingDocument18 pagesGroup 8 Capital BudgetingjovibonNo ratings yet

- Sundries Cinema Solution F 22Document4 pagesSundries Cinema Solution F 22Falguni ShomeNo ratings yet

- 532-16-Isnaini Nur Fauziah (2.2)Document53 pages532-16-Isnaini Nur Fauziah (2.2)isnaininurfauziah123No ratings yet

- Training Program For Traffic Shift Peshawar Month: September, 2020Document2 pagesTraining Program For Traffic Shift Peshawar Month: September, 2020aftab_sweet3024No ratings yet

- Tea Bar & Stationary Items For Dec 2020: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)Document1 pageTea Bar & Stationary Items For Dec 2020: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)aftab_sweet3024No ratings yet

- Tea Bar & Stationary Items For July, 2019: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)Document1 pageTea Bar & Stationary Items For July, 2019: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)aftab_sweet3024No ratings yet

- Tea Bar & Stationary Items For Mar, 2019: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)Document1 pageTea Bar & Stationary Items For Mar, 2019: Departments Tea Box SUGAR (KG) Everyday Dry Milk (KG)aftab_sweet3024No ratings yet

- Training For Shift BDocument1 pageTraining For Shift Baftab_sweet3024No ratings yet

- Complaint Recorded and Received in Caa Feedback/Suggestion CellDocument3 pagesComplaint Recorded and Received in Caa Feedback/Suggestion Cellaftab_sweet3024No ratings yet

- Web Query DJIA Components and Contribution To ChangeDocument3 pagesWeb Query DJIA Components and Contribution To Changeaftab_sweet3024No ratings yet

- Workbook1 2Document83 pagesWorkbook1 2aftab_sweet3024No ratings yet

- Office ChairsDocument1 pageOffice Chairsaftab_sweet3024No ratings yet

- Altman Z-Score AnalysisDocument3 pagesAltman Z-Score Analysismc limNo ratings yet

- WaccDocument1 pageWaccMuhammad Ahsan MukhtarNo ratings yet

- Guide to the 10 Main Cloud TypesDocument3 pagesGuide to the 10 Main Cloud Typesaftab_sweet3024No ratings yet

- Required Returns and The Cost of CapitalDocument49 pagesRequired Returns and The Cost of Capitalaftab_sweet3024No ratings yet

- Workbook1 2Document83 pagesWorkbook1 2aftab_sweet3024No ratings yet

- Operating and Financial LeverageDocument63 pagesOperating and Financial Leverageaftab_sweet3024No ratings yet

- CH 12Document31 pagesCH 12Mochammad RidwanNo ratings yet

- CH 05Document56 pagesCH 05aftab_sweet3024No ratings yet

- Mergers and Other Forms of Corporate RestructuringDocument47 pagesMergers and Other Forms of Corporate Restructuringaftab_sweet3024No ratings yet

- CH 12Document31 pagesCH 12Mochammad RidwanNo ratings yet

- CH 11Document40 pagesCH 11aftab_sweet3024No ratings yet

- CH 13Document58 pagesCH 13AbdullahJatholNo ratings yet

- The Valuation of Long-Term SecuritiesDocument82 pagesThe Valuation of Long-Term Securitiesaftab_sweet3024No ratings yet

- Overview of Working Capital ManagementDocument25 pagesOverview of Working Capital Managementaftab_sweet3024No ratings yet

- CH 06Document68 pagesCH 06aftab_sweet3024No ratings yet

- CH 01Document20 pagesCH 01aftab_sweet3024No ratings yet

- CH 03Document86 pagesCH 03aftab_sweet3024No ratings yet

- Fund Analysis, Cash-Flow Analysis, and Financial PlanningDocument58 pagesFund Analysis, Cash-Flow Analysis, and Financial Planningaftab_sweet3024No ratings yet

- The Business, Tax, and Financial EnvironmentsDocument44 pagesThe Business, Tax, and Financial Environmentsaftab_sweet3024No ratings yet

- 1 PointDocument7 pages1 Pointaftab_sweet3024No ratings yet

- Name: K K ID#: Lab Partner: V S Date: Wednesday 22 Course Code: BIOL 2363 - Metabolism Title of Lab: Assay of Tissue GlycogenDocument7 pagesName: K K ID#: Lab Partner: V S Date: Wednesday 22 Course Code: BIOL 2363 - Metabolism Title of Lab: Assay of Tissue GlycogenKarina KhanNo ratings yet

- The Metatronic KeysDocument10 pagesThe Metatronic KeysArnulfo Yu Laniba100% (1)

- (Historical Materialism Book Series 32) Lapavitsas, Costas - Financialisation in Crisis (2012, Brill Academic Pub)Document276 pages(Historical Materialism Book Series 32) Lapavitsas, Costas - Financialisation in Crisis (2012, Brill Academic Pub)monikaNo ratings yet

- Gpfs Overview v33Document54 pagesGpfs Overview v33Farha AzadNo ratings yet

- Remote Access Portal User GuideDocument3 pagesRemote Access Portal User GuidezeljavaNo ratings yet

- BMEn 3301 Spring 2013 SyllabusDocument13 pagesBMEn 3301 Spring 2013 SyllabussfairhuNo ratings yet

- Ch1 SlidesDocument47 pagesCh1 SlidesPierreNo ratings yet

- VampireRev4-Page Editable PDFDocument4 pagesVampireRev4-Page Editable PDFNicholas DoranNo ratings yet

- BA Mckesson Interview 2Document3 pagesBA Mckesson Interview 2Vikram hostNo ratings yet

- Eng. XI, U18 Meaning Into WordsDocument4 pagesEng. XI, U18 Meaning Into Wordssanad BhattaraiNo ratings yet

- Lec # 10 Earthing and GroundingDocument68 pagesLec # 10 Earthing and GroundingSaddam jatt786No ratings yet

- Case Study of Haleeb FoodDocument18 pagesCase Study of Haleeb Foodjazi_4u86% (22)

- CAT D7H Track-Type Tractor Electrical System Schematic - SENR4182SENR4182 - SIS PDFDocument2 pagesCAT D7H Track-Type Tractor Electrical System Schematic - SENR4182SENR4182 - SIS PDFKomatsu Perkins HitachiNo ratings yet

- Handley MouleDocument4 pagesHandley MouleAnonymous vcdqCTtS9No ratings yet

- GPSForex Robot V2 User GuideDocument40 pagesGPSForex Robot V2 User GuideMiguel Angel PerezNo ratings yet

- ZEOLITEDocument13 pagesZEOLITEShubham Yele100% (1)

- Electronics, Furniture, Clothing and Home Stores in KalkaDocument4 pagesElectronics, Furniture, Clothing and Home Stores in KalkaMANSA MARKETINGNo ratings yet

- Anatolii PapanovDocument8 pagesAnatolii PapanovKyrademNo ratings yet

- Process Payments & ReceiptsDocument12 pagesProcess Payments & ReceiptsAnne FrondaNo ratings yet

- Laptops and Desktop-MAY PRICE 2011Document8 pagesLaptops and Desktop-MAY PRICE 2011Innocent StrangerNo ratings yet

- An Investigation Into The Effects of Unsteady Parameters On The Aerodynamics of A Low Reynolds Number Pitching AirfoilDocument15 pagesAn Investigation Into The Effects of Unsteady Parameters On The Aerodynamics of A Low Reynolds Number Pitching AirfoilMANNE SAHITHINo ratings yet

- Currency DerivativesDocument16 pagesCurrency DerivativesAdityaNandaNo ratings yet

- Small Events in The Royal ParksDocument6 pagesSmall Events in The Royal ParksTroy HealyNo ratings yet

- Calculating production costs and selling pricesDocument2 pagesCalculating production costs and selling pricesMitch BelmonteNo ratings yet

- Photoshop Cheat SheetDocument11 pagesPhotoshop Cheat SheetGiova RossiNo ratings yet

- Maths English Medium 7 To 10Document13 pagesMaths English Medium 7 To 10TNGTASELVASOLAINo ratings yet

- Awfpc 2022Document7 pagesAwfpc 2022Jay-p BayonaNo ratings yet

- Selected Questions Revised 20200305 2HRDocument3 pagesSelected Questions Revised 20200305 2HRTimmy LeeNo ratings yet

- Insurance - Unit 3&4Document20 pagesInsurance - Unit 3&4Dhruv GandhiNo ratings yet

- Advertisement AnalysisDocument15 pagesAdvertisement AnalysisDaipayan DuttaNo ratings yet