You might also like

- Collection of Pitch Decks From Venture Capital Funded StartupsDocument22 pagesCollection of Pitch Decks From Venture Capital Funded StartupsAlan Petzold50% (2)

- Assignment 2 - Consumer Research, Inc.Document9 pagesAssignment 2 - Consumer Research, Inc.orestes chavez tiburcioNo ratings yet

- Math, Grade 4: Strengthening Basic Skills with Jokes, Comics, and RiddlesFrom EverandMath, Grade 4: Strengthening Basic Skills with Jokes, Comics, and RiddlesNo ratings yet

- Time Scedul Jepon BogorejoDocument1 pageTime Scedul Jepon Bogorejoainana151719No ratings yet

- Week 21Document22 pagesWeek 21jujuekyoNo ratings yet

- SC EduleDocument1 pageSC Edulebstn ydkNo ratings yet

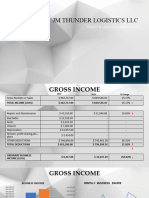

- JM Thunder Logistics LLCDocument5 pagesJM Thunder Logistics LLCJan Ray Oviedo EscotoNo ratings yet

- 3rd Quarter SMEPA 2022-2023Document15 pages3rd Quarter SMEPA 2022-2023Anne Cerna ElgaNo ratings yet

- SPSS Ian FinalDocument4 pagesSPSS Ian FinalEvan FondxNo ratings yet

- A Study On The Performance of Canara Bank in The Effective Supply of The Agricultural Credit (With Reference To Tirunelveli Region)Document10 pagesA Study On The Performance of Canara Bank in The Effective Supply of The Agricultural Credit (With Reference To Tirunelveli Region)smilingeyes_nicNo ratings yet

- Lecture 03Document66 pagesLecture 03Thi NtdNo ratings yet

- Six Sigma 2022 Yellow Belt Rpid4 - No.18 Victory TeamDocument30 pagesSix Sigma 2022 Yellow Belt Rpid4 - No.18 Victory TeamDandi RawhideNo ratings yet

- Expense Report Lrvi Enginnering Solutions (P) LTDDocument1 pageExpense Report Lrvi Enginnering Solutions (P) LTDselvakumarNo ratings yet

- 2017.10.23 Denton Presentation v1.2Document38 pages2017.10.23 Denton Presentation v1.2LaryNo ratings yet

- Anandam Manufacturing Company.1Document2 pagesAnandam Manufacturing Company.1AkshitNo ratings yet

- 12daily Production Report December.2020Document165 pages12daily Production Report December.2020Melaku AlemuNo ratings yet

- Flujo Proy Helados KicosDocument3 pagesFlujo Proy Helados Kicosgio.vany107No ratings yet

- EMI Calculator ExcelDocument20 pagesEMI Calculator ExcelSheru Shri100% (1)

- Labour Market Dashboard VictoriaDocument1 pageLabour Market Dashboard VictoriaNatalia AvendañoNo ratings yet

- Earned Value Calculation Total ActualDocument2 pagesEarned Value Calculation Total ActualKev Wilk0% (1)

- Acad-Canal Yupash P-03Document1 pageAcad-Canal Yupash P-03Ingessi SrlNo ratings yet

- Tata Steel - Financial Model - 2016-2025Document95 pagesTata Steel - Financial Model - 2016-2025Prabhdeep DadyalNo ratings yet

- Placment New SummaryDocument5 pagesPlacment New SummaryD Y Patil Institute of MCA and MBANo ratings yet

- ManpowerDocument1 pageManpowerAbbas FarisNo ratings yet

- Truck Refrigration Import Duty CostDocument1 pageTruck Refrigration Import Duty Costsrk1066997No ratings yet

- 6.3 Identity 3: Div and Curl Of: Lecture 6. Vector Operator IdentitiesDocument1 page6.3 Identity 3: Div and Curl Of: Lecture 6. Vector Operator IdentitiesRubensVilhenaFonsecaNo ratings yet

- Ministry of TourismDocument4 pagesMinistry of TourismVruddhi GalaNo ratings yet

- Statistics Assignment 2Document9 pagesStatistics Assignment 2Nguyễn Thu HươngNo ratings yet

- Higher Education in Oregon:: Sustaining The MomentumDocument25 pagesHigher Education in Oregon:: Sustaining The MomentumStatesman JournalNo ratings yet

- StatDocument3 pagesStatCrisel BelmonteNo ratings yet

- Revenue History ChartDocument2 pagesRevenue History ChartjsweigartNo ratings yet

- S CurveDocument3 pagesS Curveilham fdhlman11No ratings yet

- Abb Roi CalculationDocument1 pageAbb Roi Calculationapples.kingdom16No ratings yet

- LN11 BubblesDocument8 pagesLN11 BubblesChiu Tat ChanNo ratings yet

- Weekly Debt Portfolio Summary 12202023Document2 pagesWeekly Debt Portfolio Summary 12202023final bossuNo ratings yet

- BHMH 2002 A2 Ans Sheets Including Cover 2223 S2-1Document5 pagesBHMH 2002 A2 Ans Sheets Including Cover 2223 S2-1Yan YanNo ratings yet

- EKMX Spot Buy Management: Direct MaterialDocument24 pagesEKMX Spot Buy Management: Direct MaterialsaintchagNo ratings yet

- JM Thunder LogisticsDocument5 pagesJM Thunder LogisticsJan Ray Oviedo EscotoNo ratings yet

- Work Together 6-1 6-2 6-3Document1 pageWork Together 6-1 6-2 6-3James SargentNo ratings yet

- Statistics Assignment 2: Matteo Conta Femba 9BDocument9 pagesStatistics Assignment 2: Matteo Conta Femba 9BKireeti RepalaNo ratings yet

- 2) Solution To Problem No 2 On Flexible BudgetDocument7 pages2) Solution To Problem No 2 On Flexible BudgetVikas guptaNo ratings yet

- PM Presentation Baba GroupDocument9 pagesPM Presentation Baba GroupHuzaifa Iftikhar CHNo ratings yet

- 3G Congestion OptimizationDocument4 pages3G Congestion Optimizationmuh47irNo ratings yet

- 5 Feb - 10 FebDocument1 page5 Feb - 10 Febsaptalestarinusantara2020No ratings yet

- Nestle: Final Task in Fundamentals of Accountancy, Business and ManagementDocument43 pagesNestle: Final Task in Fundamentals of Accountancy, Business and ManagementApply Ako Work EhNo ratings yet

- catalogo-fkgroup-2020-ENG ES-web 210610 145601 210705 094438Document25 pagescatalogo-fkgroup-2020-ENG ES-web 210610 145601 210705 094438Damian Matute QuinterosNo ratings yet

- Yqj6 - Bahan Tayang Progres Kinerja APBN TA. 2021 KLHK S.D 27 DES 2021Document2 pagesYqj6 - Bahan Tayang Progres Kinerja APBN TA. 2021 KLHK S.D 27 DES 2021Muhammad Rifki SetiawanNo ratings yet

- Toolholder LenczewskiDocument1 pageToolholder Lenczewskiapi-537721748No ratings yet

- EMI Calculator - Prepayment OptionDocument22 pagesEMI Calculator - Prepayment Optionsushaht modiNo ratings yet

- Problem Set 2 SolutionsDocument34 pagesProblem Set 2 SolutionsglavchevanasikNo ratings yet

- Diesel Progress - November 2022-16Document2 pagesDiesel Progress - November 2022-16Matias121212No ratings yet

- Chapter 08Document60 pagesChapter 08Maram MaheshNo ratings yet

- 02 Update On Measles Rubella EliminationDocument32 pages02 Update On Measles Rubella Eliminationnavneet singhNo ratings yet

- Macroeconomic AnalysisDocument19 pagesMacroeconomic AnalysisJestoni VillareizNo ratings yet

- Material DashboardDocument1 pageMaterial DashboardmdcegyptNo ratings yet

- Chapter 13 ForecastingDocument21 pagesChapter 13 Forecastingapi-25888404No ratings yet

- Regresi Dan Korelasi RifdaDocument7 pagesRegresi Dan Korelasi RifdaNurmilaNo ratings yet

- Income Tax Calculator 2023-24 v08 02Document6 pagesIncome Tax Calculator 2023-24 v08 02syedfurkhan41No ratings yet

- 2.3 Pareto Charts SlidesDocument2 pages2.3 Pareto Charts Slidesal_snowNo ratings yet

- Analytics Portatil - Jaca.com - BR 200610 Dashboard Report)Document6 pagesAnalytics Portatil - Jaca.com - BR 200610 Dashboard Report)macintoxicNo ratings yet

- Bar Chart and S-Curve: 1. Mechanization of Steelgates at MC Sta 17+701Document1 pageBar Chart and S-Curve: 1. Mechanization of Steelgates at MC Sta 17+701Planning Unit Pangasinan IMONo ratings yet

- India's Foreign Trade Policy - 29 August 2021Document17 pagesIndia's Foreign Trade Policy - 29 August 2021Akanksha GuptaNo ratings yet

- Discussion IDocument1 pageDiscussion IAkanksha GuptaNo ratings yet

- Export Import Procedures and Documentation MBA 243Document21 pagesExport Import Procedures and Documentation MBA 243Akanksha GuptaNo ratings yet

- Regulation of International Trade - 29 August 2021Document7 pagesRegulation of International Trade - 29 August 2021Akanksha GuptaNo ratings yet

- India's Foreign Trade Policy - 29 August 2021Document17 pagesIndia's Foreign Trade Policy - 29 August 2021Akanksha GuptaNo ratings yet

- International Trade - 29 August 2021Document8 pagesInternational Trade - 29 August 2021Akanksha GuptaNo ratings yet

- Security and Encryption Part 3 - 2Document29 pagesSecurity and Encryption Part 3 - 2Akanksha GuptaNo ratings yet

- Time - Table - MBA - 3rd Semester - 2021Document2 pagesTime - Table - MBA - 3rd Semester - 2021Akanksha GuptaNo ratings yet

- C Rama Gopal Export - Import - ProceduresDocument243 pagesC Rama Gopal Export - Import - Proceduresrabinosss83% (12)

- Major Project Guide List MBA (W) 3rd & 4th SemDocument4 pagesMajor Project Guide List MBA (W) 3rd & 4th SemAkanksha GuptaNo ratings yet

- Date Sheet Aug-Dec 2021Document1 pageDate Sheet Aug-Dec 2021Akanksha GuptaNo ratings yet

- Managerial Economics TutorialDocument82 pagesManagerial Economics TutorialBreej100% (1)

- Academic Calenderaug 2021 (Iiisem)Document1 pageAcademic Calenderaug 2021 (Iiisem)Akanksha GuptaNo ratings yet

- ValueChain in EC-2Document13 pagesValueChain in EC-2Akanksha GuptaNo ratings yet

- A. Where Exactly Is This Dreamy Place?Document3 pagesA. Where Exactly Is This Dreamy Place?Akanksha GuptaNo ratings yet

- Security and Encryption Part 2 - 2Document13 pagesSecurity and Encryption Part 2 - 2Akanksha GuptaNo ratings yet

- Security and Encryption Part 2 - 2Document13 pagesSecurity and Encryption Part 2 - 2Akanksha GuptaNo ratings yet

- 00916688520-Rohit Sivanand-Operation MGT AssignmentDocument17 pages00916688520-Rohit Sivanand-Operation MGT AssignmentAkanksha GuptaNo ratings yet

- Adam SmithDocument3 pagesAdam SmithAkanksha GuptaNo ratings yet

- AssignmentDocument1 pageAssignmentAkanksha GuptaNo ratings yet

- Notes 8Document21 pagesNotes 8Akanksha GuptaNo ratings yet

- Managerial Economics NotesDocument47 pagesManagerial Economics NotesAkanksha GuptaNo ratings yet

- Behavioral Asset Allocation Revised Victoria 100921Document38 pagesBehavioral Asset Allocation Revised Victoria 100921Akanksha GuptaNo ratings yet

- Management of Technology: Chapter 1: IntroductionDocument202 pagesManagement of Technology: Chapter 1: IntroductionAkanksha GuptaNo ratings yet

- Introduction To Macroeconomics-MBA WKDocument56 pagesIntroduction To Macroeconomics-MBA WKAkanksha GuptaNo ratings yet

- 101 Managerial Economics MBA 2020Document393 pages101 Managerial Economics MBA 2020Akanksha GuptaNo ratings yet

- AFM-1Document16 pagesAFM-1Akanksha GuptaNo ratings yet

- AFM-1Document16 pagesAFM-1Akanksha GuptaNo ratings yet

- AFM-1Document16 pagesAFM-1Akanksha GuptaNo ratings yet

- CFO Macro12 PPT 19Document45 pagesCFO Macro12 PPT 19Pedro ValdiviaNo ratings yet

- 2021.10 - Asset Class Returns Forecast - Q4 2021 - ENDocument4 pages2021.10 - Asset Class Returns Forecast - Q4 2021 - ENStephane MysonaNo ratings yet

- Ratio Analysis Formula Excel TemplateDocument5 pagesRatio Analysis Formula Excel TemplateRaavan MaharajNo ratings yet

- A Study On The Performance of Large Cap Equity Mutual Funds in India PDFDocument16 pagesA Study On The Performance of Large Cap Equity Mutual Funds in India PDFAbhinav AgrawalNo ratings yet

- FIN 542 Assigmt 30%-OCT2023Document1 pageFIN 542 Assigmt 30%-OCT2023BalqisNo ratings yet

- Dividend DecisionDocument20 pagesDividend DecisionRiya_Biswas_8955No ratings yet

- EXINITY Client Agreement V5Document29 pagesEXINITY Client Agreement V5Pedro PerezNo ratings yet

- Own Summary On Crypto-Currency and BlockchainDocument4 pagesOwn Summary On Crypto-Currency and BlockchainZacharias Kuoh HaotengNo ratings yet

- Stormgain Public Api: Coingecko StandardsDocument11 pagesStormgain Public Api: Coingecko StandardsCarlos Alejandro PerdomoNo ratings yet

- You Have Recently Been Hired by Layton Motors Inc LmiDocument1 pageYou Have Recently Been Hired by Layton Motors Inc LmiAmit PandeyNo ratings yet

- Auditing Investments 1Document2 pagesAuditing Investments 1Sabel FordNo ratings yet

- BNP Paribas. The Challenge of OTC Derivarives ClearingDocument56 pagesBNP Paribas. The Challenge of OTC Derivarives ClearingGest DavidNo ratings yet

- IAPM I IntroductionDocument23 pagesIAPM I IntroductionSuresh Vadde100% (2)

- TC110214 HS001Document1 pageTC110214 HS001Andoko AzzaNo ratings yet

- 15 Strength 7 ElevenDocument3 pages15 Strength 7 ElevenPavitra ThinakaranNo ratings yet

- Financial ManagementDocument7 pagesFinancial Managementsakshisharma17164No ratings yet

- Indian Debt MarketDocument32 pagesIndian Debt MarketProfessorAsim Kumar Mishra0% (1)

- Food Production & Distribution Newsletter Q3'23Document19 pagesFood Production & Distribution Newsletter Q3'23Kevin ParkerNo ratings yet

- Questions and AnswersDocument8 pagesQuestions and Answersnehasingh1992100% (1)

- C - 22 - Retained Earnings (Dividends, Appropriation, and Quasi-Reorganization) (PDocument14 pagesC - 22 - Retained Earnings (Dividends, Appropriation, and Quasi-Reorganization) (PJoyluxxiNo ratings yet

- Financial Markets: Hot Topic of The EconomyDocument8 pagesFinancial Markets: Hot Topic of The EconomyOtmane Senhadji El RhaziNo ratings yet

- Alex Sharp's PortfolioDocument6 pagesAlex Sharp's PortfolioFurqanTariqNo ratings yet

- Bonos 19-06-18Document7 pagesBonos 19-06-18Maximiliano A. SireraNo ratings yet

- IDX Statistic 2021Q3Document228 pagesIDX Statistic 2021Q3LisaNo ratings yet

- Ipm 2Document62 pagesIpm 2Anna Lyssa BatasNo ratings yet

- Level III Mock Exam Questions 2017ADocument24 pagesLevel III Mock Exam Questions 2017AElie Yabroudi0% (1)

- Fin 332 HW 3 Fall 2021Document5 pagesFin 332 HW 3 Fall 2021Alena ChauNo ratings yet

- To Islamic Finance: DR Masahina SarabdeenDocument20 pagesTo Islamic Finance: DR Masahina SarabdeenNouf ANo ratings yet