You might also like

- Indian Mortgage Finance Market PDFDocument61 pagesIndian Mortgage Finance Market PDFmikecoreleonNo ratings yet

- AXIS BANK NDocument20 pagesAXIS BANK Nankit5849733% (3)

- 2019 Asia Insurance Market ReportDocument44 pages2019 Asia Insurance Market ReportFarraz RadityaNo ratings yet

- Business Startup Costs TemplateDocument10 pagesBusiness Startup Costs TemplateRandoNo ratings yet

- Top 100 MarchDocument39 pagesTop 100 MarchPratik ShandilyaNo ratings yet

- List of MSCSsDocument62 pagesList of MSCSsAbhijit SamantNo ratings yet

- Software Account ManagementDocument114 pagesSoftware Account ManagementamiteshnegiNo ratings yet

- Making Diversity Work: Key Trends and Practices in The Indian IT-BPM IndustryDocument24 pagesMaking Diversity Work: Key Trends and Practices in The Indian IT-BPM IndustryAfzal MohammedNo ratings yet

- India 2030 PDFDocument188 pagesIndia 2030 PDFGray HouserNo ratings yet

- SBI Business LoanDocument12 pagesSBI Business LoanAjit SamalNo ratings yet

- VP Director Global Sales in San Diego CA Resume David SilvaDocument2 pagesVP Director Global Sales in San Diego CA Resume David SilvaDavidSilva2No ratings yet

- Presentation On Indian EntrepreneursDocument8 pagesPresentation On Indian Entrepreneursarvind100% (1)

- Financial Services: January 2021Document33 pagesFinancial Services: January 2021Money HavenNo ratings yet

- Varanium 11042019Document25 pagesVaranium 11042019Rahul JainNo ratings yet

- India Digital Payments ReportDocument22 pagesIndia Digital Payments ReportMeet Mukesh PaswanNo ratings yet

- US GTM LentraDocument6 pagesUS GTM LentraNabeel MohammadNo ratings yet

- Agri Clinics & Agribusiness Centers ReportDocument36 pagesAgri Clinics & Agribusiness Centers Reportveenaa somashekar0% (1)

- Debt Collection Recovery Management Sea BankDocument4 pagesDebt Collection Recovery Management Sea BankPranav KhannaNo ratings yet

- Jkbank Phone NoDocument6 pagesJkbank Phone NoVarun KundalNo ratings yet

- AI Automation Shopping GuideDocument10 pagesAI Automation Shopping GuideAnik ChakrabortyNo ratings yet

- Collections Technical ReferenceDocument234 pagesCollections Technical Referencesrusda994No ratings yet

- WNS BFS Capabilities Presentation - Jan - 2013Document30 pagesWNS BFS Capabilities Presentation - Jan - 2013VikasNo ratings yet

- Icici BankDocument33 pagesIcici BankpRiNcE DuDhAtRaNo ratings yet

- List of BanksDocument5 pagesList of Banksramu3131No ratings yet

- Anand RathiDocument3 pagesAnand RathiShilpa EdarNo ratings yet

- BRM Pet InsuranceDocument10 pagesBRM Pet InsuranceVaishnaviNo ratings yet

- Cerulli Report - Targeting The Affluent and The Emerging AffluentDocument25 pagesCerulli Report - Targeting The Affluent and The Emerging AffluentJoin RiotNo ratings yet

- The Topic of Confluence With Fibonacci RetracementsDocument6 pagesThe Topic of Confluence With Fibonacci RetracementsVeljko KerčevićNo ratings yet

- Fashion Online FashinZaDocument4 pagesFashion Online FashinZaArdheta NatalegawaNo ratings yet

- Oracle Developer CV PDFDocument2 pagesOracle Developer CV PDFPar NawNo ratings yet

- EMIS Insights - India Insurance Sector Report 2020 - 2024Document79 pagesEMIS Insights - India Insurance Sector Report 2020 - 2024Kathiravan Rajendran100% (1)

- Automated System in BankingDocument60 pagesAutomated System in BankingMewati GaneshNo ratings yet

- FGST0015 - UX Theme Presentation TemplateDocument34 pagesFGST0015 - UX Theme Presentation TemplateSeguNo ratings yet

- KRASHAK Mobile App-InfoDocument13 pagesKRASHAK Mobile App-InfobandhuNo ratings yet

- How To Find Available Domain NamesDocument47 pagesHow To Find Available Domain NamesManoranjan SahooNo ratings yet

- Gat No Name of Bachat Gat Area of Bachat Gat No of Members Bachat Gat Leader Name Mobile NoDocument23 pagesGat No Name of Bachat Gat Area of Bachat Gat No of Members Bachat Gat Leader Name Mobile NoSajid Bhai ShaikhNo ratings yet

- Prof.. Anju Dusseja: Name Roll - NoDocument18 pagesProf.. Anju Dusseja: Name Roll - NoOmkar PandeyNo ratings yet

- Small Finance Indian Book PDFDocument84 pagesSmall Finance Indian Book PDFrajeshraj0112No ratings yet

- TMT Predictions 202 - Deloitte IndiaDocument150 pagesTMT Predictions 202 - Deloitte IndiaAakash MalhotraNo ratings yet

- Comparative Analysis of HDFCDocument18 pagesComparative Analysis of HDFCgagandeepsingh86No ratings yet

- CA Focused AttachmentsDocument8 pagesCA Focused AttachmentssatishNo ratings yet

- PS - Tails of CitiesDocument13 pagesPS - Tails of CitiesRachit VarshneyNo ratings yet

- Packaged Drinking WaterDocument7 pagesPackaged Drinking WaterSudhanshu KulshresthaNo ratings yet

- Attachment Banking Important Terms Part 1 and 3 Lyst3289Document25 pagesAttachment Banking Important Terms Part 1 and 3 Lyst3289Vaishali SinghNo ratings yet

- Employability Skills in Management StudentsDocument9 pagesEmployability Skills in Management Studentskingsing44No ratings yet

- Alibaba SWOT AnalysisDocument2 pagesAlibaba SWOT AnalysisShahzod TulanovNo ratings yet

- Know The Top 10 Benefits of TravellingDocument1 pageKnow The Top 10 Benefits of TravellingDetained EngineersNo ratings yet

- CRED Business Model 1624002930Document1 pageCRED Business Model 1624002930Jasleen Kaur AllaghNo ratings yet

- By Akshay Tyagi: NBFC PlaybookDocument13 pagesBy Akshay Tyagi: NBFC PlaybookAkshay TyagiNo ratings yet

- SME Financing: Submitted To Mr. S. Clement September 17,2010Document29 pagesSME Financing: Submitted To Mr. S. Clement September 17,2010scribddddddddddddNo ratings yet

- Fs - Financial InclusionDocument7 pagesFs - Financial InclusionWasim SNo ratings yet

- ABHIJEET PAWAR - Final SIP ReportDocument82 pagesABHIJEET PAWAR - Final SIP ReportAbhijeet PawarNo ratings yet

- Role of Payments BankDocument16 pagesRole of Payments BankAstik TripathiNo ratings yet

- Growing Need For Modest STP in Trade Finance OperationsDocument25 pagesGrowing Need For Modest STP in Trade Finance OperationsGIRINo ratings yet

- Development BanksDocument17 pagesDevelopment BanksAsim jawedNo ratings yet

- Paryant Agarwal SIP ReportDocument59 pagesParyant Agarwal SIP ReportjatinNo ratings yet

- (Hotel Reservation) Business Plan: RadissonDocument4 pages(Hotel Reservation) Business Plan: Radissoniqra khanNo ratings yet

- Analysis of FII Data 2013 & 2018 - MA EconomicsDocument27 pagesAnalysis of FII Data 2013 & 2018 - MA EconomicsSaloni SomNo ratings yet

- The Progress of Global Financial Inclusion and Challenges Toward Universal Financial Assess AbstractDocument13 pagesThe Progress of Global Financial Inclusion and Challenges Toward Universal Financial Assess AbstractLena PhanNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-WeworkDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-WeworkTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-Robert Kiyosaki 2019Document3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-Robert Kiyosaki 2019Tanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-No Sex Please We're JapaneseDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-No Sex Please We're JapaneseTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-How Can Engineer Built His Small TV Component ShopDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-How Can Engineer Built His Small TV Component ShopTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-The Secrets of SugarTanmay SawantNo ratings yet

- Tanmay Anandrao Sawant Sasmira Business School: Topic:-How Can Engineer Built His Small TV Component ShopDocument3 pagesTanmay Anandrao Sawant Sasmira Business School: Topic:-How Can Engineer Built His Small TV Component ShopTanmay SawantNo ratings yet

- Hull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 9: Xvas Multiple Choice Test BankDocument4 pagesHull: Options, Futures, and Other Derivatives, Tenth Edition Chapter 9: Xvas Multiple Choice Test BankKevin Molly KamrathNo ratings yet

- Internal Control Over CashDocument8 pagesInternal Control Over CashAbraham BizualemNo ratings yet

- Acupressure NotesDocument20 pagesAcupressure NotesIsmail MamodeNo ratings yet

- Account 2023-2024 1Document2 pagesAccount 2023-2024 1nurulislam.seipNo ratings yet

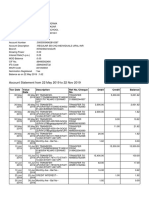

- Estmt - 2022 01 31Document4 pagesEstmt - 2022 01 31Luiza PaveiNo ratings yet

- SBI Nov PDFDocument5 pagesSBI Nov PDFbinduNo ratings yet

- Bank Book of XXXX Bank For The Month of January, 2020Document3 pagesBank Book of XXXX Bank For The Month of January, 2020CacptCoachingNo ratings yet

- Liquidity Risk ManagementDocument28 pagesLiquidity Risk ManagementAngelica B. PatagNo ratings yet

- Bank Mandate Form For Electronic Payment 1. Vendor's/Contractor'sDocument1 pageBank Mandate Form For Electronic Payment 1. Vendor's/Contractor'sBHUVI GROUPNo ratings yet

- Overview of Regular Savings Key Policies and Fees: Bank of America Clarity StatementDocument2 pagesOverview of Regular Savings Key Policies and Fees: Bank of America Clarity StatementJacob DaleNo ratings yet

- Cash AssignmentsDocument21 pagesCash AssignmentsSushil RiyarNo ratings yet

- HDFC Bank StatementDocument7 pagesHDFC Bank Statementketan_savajiyaniNo ratings yet

- Samiksha Ingle TYBMSDocument19 pagesSamiksha Ingle TYBMSKrishna YadavNo ratings yet

- 3.BANKING SECTOR - Nishtha ChhabraDocument83 pages3.BANKING SECTOR - Nishtha ChhabraHarshal FuseNo ratings yet

- ACCCOB2 Chapter 2 CASH AND CASH EQUIVALENT EXERCISESDocument15 pagesACCCOB2 Chapter 2 CASH AND CASH EQUIVALENT EXERCISESAyanna CameroNo ratings yet

- Impact of Interest Rate Spread On Profitability of Commercial Banks in NepalDocument44 pagesImpact of Interest Rate Spread On Profitability of Commercial Banks in NepalSujan pokhrelNo ratings yet

- Account Statement 2012 August RONDocument5 pagesAccount Statement 2012 August RONAna-Maria DincaNo ratings yet

- BoG On Revision On The Suspension of DividendsDocument2 pagesBoG On Revision On The Suspension of DividendsJoseph Appiah-DolphyneNo ratings yet

- Finmar Q2Document18 pagesFinmar Q2Tatyanna KaliahNo ratings yet

- Secrets in Order To Apply For Credit CardsDocument2 pagesSecrets in Order To Apply For Credit CardsKnightOverby3No ratings yet

- Cu Profile 24299Document11 pagesCu Profile 24299Odel KabristanteNo ratings yet

- Risk Management in ForexDocument88 pagesRisk Management in ForexIshfaqMalik100% (1)

- SWIFT Codes & BIC Codes For All The Banks in TheDocument1 pageSWIFT Codes & BIC Codes For All The Banks in TheGhanem AlamroNo ratings yet

- SBI Life Cerificate PDFDocument1 pageSBI Life Cerificate PDFsachin sawantNo ratings yet

- Micro Finance Banks in IndiaDocument9 pagesMicro Finance Banks in IndiaRajat SinghNo ratings yet

- Sahara Credit Co-Oprative Society LimitedDocument29 pagesSahara Credit Co-Oprative Society LimitedJagabandhu PradhanNo ratings yet

- Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation For Their Prevention in Europe and SpainDocument20 pagesCryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation For Their Prevention in Europe and Spaindaniella maliwatNo ratings yet

- Accounting For Notes PayableDocument10 pagesAccounting For Notes PayableLiza Mae MirandaNo ratings yet

- Investing in Germany 101Document28 pagesInvesting in Germany 101Ernesto Diaz HernandezNo ratings yet

- Account Statement: Merck Animal Health 21401 West Center Road Elkhorn, NE 68022 United StatesDocument1 pageAccount Statement: Merck Animal Health 21401 West Center Road Elkhorn, NE 68022 United StatesAJay MJ100% (1)