You might also like

- Return On Invested CapitalDocument3 pagesReturn On Invested CapitalZohairNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument44 pagesFinancial Statements, Cash Flow, and TaxesMahmoud Abdullah100% (1)

- Financial Statements, Cash Flow, and TaxesDocument45 pagesFinancial Statements, Cash Flow, and TaxesFridolin Belnovando Abditomo PrakosoNo ratings yet

- Ch02 ShowDocument44 pagesCh02 ShowardiNo ratings yet

- Principles of Corporate ValuationDocument14 pagesPrinciples of Corporate ValuationSubhrodeep DasNo ratings yet

- CH 02 - Financial Stmts Cash Flow and TaxesDocument32 pagesCH 02 - Financial Stmts Cash Flow and TaxesSyed Mohib Hassan100% (1)

- Practice Solution 2Document4 pagesPractice Solution 2Luigi NocitaNo ratings yet

- Analyze Cash FlowsDocument5 pagesAnalyze Cash FlowsAmit VarmaNo ratings yet

- Chapter 4Document18 pagesChapter 4Amjad J AliNo ratings yet

- Others 1667194749455Document17 pagesOthers 1667194749455Techboy RahulNo ratings yet

- Chapter 2: Financial Statements and Cash Flow AnalysisDocument43 pagesChapter 2: Financial Statements and Cash Flow AnalysisshimulNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument44 pagesFinancial Statements, Cash Flow, and TaxesreNo ratings yet

- Financial Accounting & AnalysisDocument10 pagesFinancial Accounting & Analysisdeval mahajanNo ratings yet

- Course: Financial Accounting and Analysis: Answer 1: Introduction: Cash Flow StatementDocument3 pagesCourse: Financial Accounting and Analysis: Answer 1: Introduction: Cash Flow StatementJobin BabuNo ratings yet

- Financial Accounting & AnalysisDocument16 pagesFinancial Accounting & AnalysisMohit ChaudharyNo ratings yet

- SEx 9Document24 pagesSEx 9Amir Madani100% (1)

- Ummary of Study Objectives: 198 Financial StatementsDocument5 pagesUmmary of Study Objectives: 198 Financial StatementsYun ChandoraNo ratings yet

- Financial Statements, Cash Flow and TaxesDocument44 pagesFinancial Statements, Cash Flow and TaxesAli JumaniNo ratings yet

- Financial Modeling FundamentalsDocument49 pagesFinancial Modeling FundamentalsАндрій ХмиренкоNo ratings yet

- Financial Analysis Final (Autosaved)Document159 pagesFinancial Analysis Final (Autosaved)sourav khandelwalNo ratings yet

- Chapter 3 - Understanding The Income StatementDocument68 pagesChapter 3 - Understanding The Income StatementNguyễn Yến NhiNo ratings yet

- Financial Ratio AnalysisDocument31 pagesFinancial Ratio AnalysisKeisha Kaye SaleraNo ratings yet

- Enterp7a Financial MGMTDocument17 pagesEnterp7a Financial MGMTVanessa Tattao IsagaNo ratings yet

- Statement of Cash Flow - Ias 7Document5 pagesStatement of Cash Flow - Ias 7Benjamin JohnNo ratings yet

- Responsibility Accounting, Segment Evaluation, and Transfer PricingDocument4 pagesResponsibility Accounting, Segment Evaluation, and Transfer PricingAlliahData100% (1)

- Cash Flow - InvestopediaDocument4 pagesCash Flow - InvestopediaBob KaneNo ratings yet

- Topic 3.5 Ratio AnalysisDocument22 pagesTopic 3.5 Ratio AnalysisSevarakhon UmarovaNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakpurnamaNo ratings yet

- Answers: Operating Income Changes in Net Operating AssetsDocument6 pagesAnswers: Operating Income Changes in Net Operating AssetsNawarathna KumariNo ratings yet

- Discounted Cash Flow ValuationDocument14 pagesDiscounted Cash Flow ValuationKristene Romarate DaelNo ratings yet

- Valuation Cash Flow A Teaching NoteDocument5 pagesValuation Cash Flow A Teaching NotesarahmohanNo ratings yet

- Topic 3 5 Ratio AnalysisDocument16 pagesTopic 3 5 Ratio AnalysisEren BarlasNo ratings yet

- Financial Analysis: Cross-sectional and time-series analysisDocument15 pagesFinancial Analysis: Cross-sectional and time-series analysisPooja MehraNo ratings yet

- Case 2 Ford MotorDocument4 pagesCase 2 Ford MotorNikki LabialNo ratings yet

- Valuation: Aswath DamodaranDocument100 pagesValuation: Aswath DamodaranhsurampudiNo ratings yet

- Financial Statements Based On Philippine Accounting Standards (Pas)Document34 pagesFinancial Statements Based On Philippine Accounting Standards (Pas)eli broquezaNo ratings yet

- Chapter 4. Financial Ratio Analyses and Their Implications To Management Learning ObjectivesDocument29 pagesChapter 4. Financial Ratio Analyses and Their Implications To Management Learning ObjectivesChieMae Benson QuintoNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakFerry JohNo ratings yet

- FCFF and FCFE ApproachesDocument22 pagesFCFF and FCFE Approachesd ddNo ratings yet

- Cash Flow Statements and Warf Computers Mini CaseDocument6 pagesCash Flow Statements and Warf Computers Mini CaseAshekin MahadiNo ratings yet

- CPG Annual Report 2014Document56 pagesCPG Annual Report 2014Anonymous 2vtxh4No ratings yet

- Cash flows for replacement project analysisDocument28 pagesCash flows for replacement project analysisNandhini NallasamyNo ratings yet

- Chap 2Document5 pagesChap 2Cẩm ChiNo ratings yet

- Chapter Four Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationDocument22 pagesChapter Four Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationmelissaNo ratings yet

- Statement of Cash Flow Chapter 2Document10 pagesStatement of Cash Flow Chapter 2Mary Ann PacilanNo ratings yet

- What Is A Profit and Loss (P&L) Statement - InvestopediaDocument16 pagesWhat Is A Profit and Loss (P&L) Statement - InvestopediaFrancisco Del PuertoNo ratings yet

- Course: Financial Accounting & Analysis A1Document10 pagesCourse: Financial Accounting & Analysis A1Pallavi PandeyNo ratings yet

- Chapter 6 (CF)Document51 pagesChapter 6 (CF)Hossain BelalNo ratings yet

- Slides s2 PDFDocument43 pagesSlides s2 PDFWellington DanielNo ratings yet

- Financial Accounting AnalysisDocument13 pagesFinancial Accounting AnalysisNikhil Agrawal88% (8)

- Définition Du Mot EBITDocument32 pagesDéfinition Du Mot EBITpaterson djedoNo ratings yet

- Mrs. Bella LlegoDocument182 pagesMrs. Bella Llegototo titiNo ratings yet

- Mod Financial Accounting Analysis 6Document14 pagesMod Financial Accounting Analysis 6aman ranaNo ratings yet

- Financial PlanningDocument22 pagesFinancial Planningangshu002085% (13)

- How Financial Statements Help Evaluate Business Performance and Increase ValueDocument61 pagesHow Financial Statements Help Evaluate Business Performance and Increase ValueNelson Ivan Acosta100% (1)

- Financial Accounting and Analysis AssignmentDocument13 pagesFinancial Accounting and Analysis Assignmentbhaskar paliwalNo ratings yet

- BU7300 - Corporate Finance Capital Budgeting Week 1Document21 pagesBU7300 - Corporate Finance Capital Budgeting Week 1Moony TamimiNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

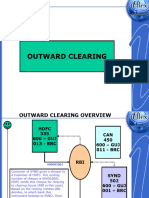

- 5-SETTLEMENT-Outward Clearing 1Document21 pages5-SETTLEMENT-Outward Clearing 1ola.cloudsNo ratings yet

- Case Study 1 p.35Document2 pagesCase Study 1 p.35Sherisse' Danielle WoodleyNo ratings yet

- Evaluating The Impact of Facebook As A Marketing Platform On The Behavior of Student Sellers and Young Entrepreneurs Among ABM Students.Document6 pagesEvaluating The Impact of Facebook As A Marketing Platform On The Behavior of Student Sellers and Young Entrepreneurs Among ABM Students.Fatima Faith PascoNo ratings yet

- BC2301B Assay SheetDocument4 pagesBC2301B Assay SheetMarcel SalasNo ratings yet

- O"5 Aodco.:of1 d"5, RL) Oos: - 6.oorpa6 G"iu O&od C56i) CD Bro5Document5 pagesO"5 Aodco.:of1 d"5, RL) Oos: - 6.oorpa6 G"iu O&od C56i) CD Bro5Prakash KumarNo ratings yet

- SM Manpower AustraliaDocument37 pagesSM Manpower Australiadhwani malde100% (1)

- Chapter Production and Costs MCQ-1Document8 pagesChapter Production and Costs MCQ-1licab58347No ratings yet

- c4 Operation PlanDocument10 pagesc4 Operation Planapi-567446365No ratings yet

- Economics - 1.1 The Market System - Igcse EdexcelDocument10 pagesEconomics - 1.1 The Market System - Igcse EdexcelWateen JaberNo ratings yet

- Valve Market Report ESADocument53 pagesValve Market Report ESAAshwin KumarNo ratings yet

- Chapter 2 The Business Vision and Mission: Strategic Management: A Competitive Advantage Approach, 14e (David)Document1 pageChapter 2 The Business Vision and Mission: Strategic Management: A Competitive Advantage Approach, 14e (David)Juna Majistad CrismundoNo ratings yet

- SW One DXP Cost Sheet (4.5BHK+Utility) Phase 1Document1 pageSW One DXP Cost Sheet (4.5BHK+Utility) Phase 1assetcafe7No ratings yet

- C-O-S-T: Cost Optimization System and TechniqueDocument37 pagesC-O-S-T: Cost Optimization System and TechniqueCharlene KronstedtNo ratings yet

- PR 2023 Batch - 19 - 04 - 2023 - FinallllDocument2 pagesPR 2023 Batch - 19 - 04 - 2023 - FinallllasdNo ratings yet

- Plant GM with 15+ Years Operations ExperienceDocument6 pagesPlant GM with 15+ Years Operations ExperiencemohammedNo ratings yet

- Payment advice from Coastal Gujarat Power to Centre Tap EngineeringDocument2 pagesPayment advice from Coastal Gujarat Power to Centre Tap EngineeringNanu PatelNo ratings yet

- Distribution Network For BritanniaDocument5 pagesDistribution Network For BritanniaSaba Dabir100% (3)

- Abdul Rauf Alias CV 2023Document4 pagesAbdul Rauf Alias CV 2023Rauf AliasNo ratings yet

- Sap Product Costing Configuration DocumentDocument16 pagesSap Product Costing Configuration Documentguru_vkg75% (4)

- AFOMA To Enable Social Impact With Decentralized E-CommerceDocument4 pagesAFOMA To Enable Social Impact With Decentralized E-CommercePR.comNo ratings yet

- Xiaomi Case StudyDocument4 pagesXiaomi Case StudyAyushi KumawatNo ratings yet

- Case 2 Compress PDFDocument17 pagesCase 2 Compress PDFAbhinav KumarNo ratings yet

- Agm Compliance ChecklistDocument3 pagesAgm Compliance ChecklistAkshay kumar Mishra100% (1)

- EPGP-11 Sec B - LCA - Marriott - EPGP-11-153Document8 pagesEPGP-11 Sec B - LCA - Marriott - EPGP-11-153Chaitanya RavankarNo ratings yet

- Wessal Karim's Rs. 91,000 Conveyor Project NPV AnalysisDocument5 pagesWessal Karim's Rs. 91,000 Conveyor Project NPV AnalysisHumair UddinNo ratings yet

- Assignment: Financial Management Unit 1Document2 pagesAssignment: Financial Management Unit 1sachinNo ratings yet

- Advertising and Integrated Brand Promotion 6th Edition OGuinn Solution ManualDocument15 pagesAdvertising and Integrated Brand Promotion 6th Edition OGuinn Solution Manualzaraazahid_950888410No ratings yet

- Operations and services strategy assignmentDocument7 pagesOperations and services strategy assignmentShivam JadhavNo ratings yet

- GrameenphoneDocument26 pagesGrameenphoneMOHAMMAD SAIFUL ISLAM100% (2)

- Britinnia Cheese: A Class Assignment ReportDocument15 pagesBritinnia Cheese: A Class Assignment ReportAshwani RaiNo ratings yet