You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Invoice ExampleDocument1 pageInvoice ExampleRohit VermaNo ratings yet

- The Bridge Project Report 2009Document19 pagesThe Bridge Project Report 2009Kent State University Cleveland Urban Design Collaborative100% (1)

- Indian Express Industry 2018Document72 pagesIndian Express Industry 2018Daniel SaslavskyNo ratings yet

- Ricover Air Transport Sector Review TJDocument54 pagesRicover Air Transport Sector Review TJDaniel SaslavskyNo ratings yet

- Regional Cooperation in Transport: Myanmar Perspective on BIMSTECDocument33 pagesRegional Cooperation in Transport: Myanmar Perspective on BIMSTECDaniel SaslavskyNo ratings yet

- Working Paper 378Document42 pagesWorking Paper 378Daniel SaslavskyNo ratings yet

- MOC - 636045268163813180 - Final Enhancing - India - Myanmar - Border - Trade - Report PDFDocument110 pagesMOC - 636045268163813180 - Final Enhancing - India - Myanmar - Border - Trade - Report PDFVek MNo ratings yet

- Biography For William Swan: © Scott AdamsDocument101 pagesBiography For William Swan: © Scott AdamsDaniel SaslavskyNo ratings yet

- Africa Ports and Harbour June 4 2008 Keynote Address Ram Mahidhara Ifc FinalDocument15 pagesAfrica Ports and Harbour June 4 2008 Keynote Address Ram Mahidhara Ifc FinalDaniel SaslavskyNo ratings yet

- MYA-IND Eximbank Trade InvestmentDocument63 pagesMYA-IND Eximbank Trade InvestmentDaniel SaslavskyNo ratings yet

- Biography For William Swan: © Scott AdamsDocument32 pagesBiography For William Swan: © Scott AdamsDaniel SaslavskyNo ratings yet

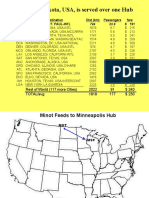

- Minot, N. Dakota, USA, Is Served Over One Hub: Airport Destination Dist (KM) Passengers FareDocument19 pagesMinot, N. Dakota, USA, Is Served Over One Hub: Airport Destination Dist (KM) Passengers FareDaniel SaslavskyNo ratings yet

- Proposal For The Gardens Mardan (Detailed Supervision)Document22 pagesProposal For The Gardens Mardan (Detailed Supervision)Umer KhanNo ratings yet

- Formal Proposal - FairmontDocument12 pagesFormal Proposal - FairmontrajpriyasolankiNo ratings yet

- Healthcare Business Monthly June Issue PDFDocument68 pagesHealthcare Business Monthly June Issue PDFvrushgangNo ratings yet

- Sexual Exploitation of Children in Africa - A Silent EmergencyDocument147 pagesSexual Exploitation of Children in Africa - A Silent EmergencyEZ ChannelNo ratings yet

- Strengthscope Applications and Case StudiesDocument5 pagesStrengthscope Applications and Case Studiessaurs24231No ratings yet

- JD 018 Food Safety ManagerDocument1 pageJD 018 Food Safety ManagerJohnson Gitonga NderiNo ratings yet

- Entry Test - IELTS Four SkillsDocument16 pagesEntry Test - IELTS Four SkillsQuynh DoNo ratings yet

- Case Study 2016 v3Document16 pagesCase Study 2016 v3Sheraz KhanNo ratings yet

- Editorial: New Trends in Nonlinear Control Systems and ApplicationsDocument3 pagesEditorial: New Trends in Nonlinear Control Systems and ApplicationsJonny MejiaNo ratings yet

- Counselling AssignmentDocument4 pagesCounselling AssignmentMegha BansalNo ratings yet

- Perform Testing DocumentationDocument5 pagesPerform Testing DocumentationGerald E Baculna100% (1)

- Martial Law in the Philippines DocumentaryDocument6 pagesMartial Law in the Philippines DocumentaryJessica BataclitNo ratings yet

- 65 Speaking Speaking Consumerism Dan Financial AwarenessDocument2 pages65 Speaking Speaking Consumerism Dan Financial AwarenessJamunaCinyora100% (1)

- FedexDocument24 pagesFedexgagan969994% (16)

- Backup of AS2 SCIE 1 (Teaching Science For Primary Grades) SYLLABUSDocument10 pagesBackup of AS2 SCIE 1 (Teaching Science For Primary Grades) SYLLABUSShar Nur Jean100% (2)

- Behavior in Groups: Aj - Nuannut Khieowan Faculty of International StudiesDocument21 pagesBehavior in Groups: Aj - Nuannut Khieowan Faculty of International StudiestakatocoyaNo ratings yet

- IFAS and EFAS TemplateDocument14 pagesIFAS and EFAS TemplateA.M A.NNo ratings yet

- Ladlad PartylistDocument10 pagesLadlad PartylistLennom EspirituNo ratings yet

- National Environmental Management: Air Quality Act 39 of 2004Document5 pagesNational Environmental Management: Air Quality Act 39 of 2004teboviNo ratings yet

- Biblical HermeneuticsDocument6 pagesBiblical HermeneuticsCriselda P. GasparNo ratings yet

- How To File Goods Declaration (GD) in Weboc - Weboc GD Filing ProcessDocument26 pagesHow To File Goods Declaration (GD) in Weboc - Weboc GD Filing Processzohaib nasirNo ratings yet

- Module 1 Personal Development - PH Learner's Handbook - FINALDocument21 pagesModule 1 Personal Development - PH Learner's Handbook - FINALLJames Sacueza100% (1)

- A. Explain The Following Statement," Without EI Outstanding Training, Highly Analytical Mind, Long Term Vision, Terrific Ideas Will Not Make A Leader". 5 B. What Is Moral Leadership?Document1 pageA. Explain The Following Statement," Without EI Outstanding Training, Highly Analytical Mind, Long Term Vision, Terrific Ideas Will Not Make A Leader". 5 B. What Is Moral Leadership?Sabiha ShantaNo ratings yet

- Trends, Networks, and Critical Thinking in The 21 Century CultureDocument2 pagesTrends, Networks, and Critical Thinking in The 21 Century CultureYhel LantionNo ratings yet

- Project On Internet MarketingDocument38 pagesProject On Internet Marketinggourav100% (1)

- TLE6 Module7 Marketing Fruits and SeedlingsDocument24 pagesTLE6 Module7 Marketing Fruits and SeedlingsLorranne Maice D. Morano83% (6)

- I Dedicate My Victory To Palestine' Afaf Raed Sharif, 17, From PalestineDocument2 pagesI Dedicate My Victory To Palestine' Afaf Raed Sharif, 17, From Palestine130660LYC OMAR BENABDELAZIZ NEDROMANo ratings yet

- 210311081143rays New Curriculum VitaeDocument3 pages210311081143rays New Curriculum VitaeHamis Rabiam MagundaNo ratings yet