You might also like

- Chap017-Financial Statement AnalysisDocument21 pagesChap017-Financial Statement AnalysismarseliaNo ratings yet

- Accounting and Finance: Fundamentals of Corporate FinanceDocument21 pagesAccounting and Finance: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Estee LauderDocument116 pagesEstee LauderHa DaoNo ratings yet

- Final Cheat Sheet FA ML X MM UpdatedDocument8 pagesFinal Cheat Sheet FA ML X MM UpdatedIrina StrizhkovaNo ratings yet

- ch01 Fundamental of Financial Accounting by Edmonds (4th Edition)Document57 pagesch01 Fundamental of Financial Accounting by Edmonds (4th Edition)Awais Azeemi100% (2)

- TIFA CheatSheet MM X MLDocument10 pagesTIFA CheatSheet MM X MLCorina Ioana BurceaNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- ACT. 1 FINANCIAL RATIOS - EllorimoDocument3 pagesACT. 1 FINANCIAL RATIOS - EllorimoEra EllorimoNo ratings yet

- Business Is FUN! - Financial RatioDocument2 pagesBusiness Is FUN! - Financial RatioHardina AliNo ratings yet

- Chapter Six: Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsDocument32 pagesChapter Six: Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsLeenNo ratings yet

- Ratio AnalysisDocument20 pagesRatio AnalysisErit AhmedNo ratings yet

- Business Finance 1st TermDocument2 pagesBusiness Finance 1st TermBrendon BaguilatNo ratings yet

- Venture Capital, Ipos, and Seasoned Offerings: Fundamentals of Corporate FinanceDocument14 pagesVenture Capital, Ipos, and Seasoned Offerings: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Current RatioDocument2 pagesCurrent RatioHafiz UllahNo ratings yet

- Level 1 Assessment Financial Analysis ProdegreeDocument4 pagesLevel 1 Assessment Financial Analysis ProdegreePrá ChîNo ratings yet

- Chapter Six: Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsDocument32 pagesChapter Six: Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsAbdelnasir HaiderNo ratings yet

- The Value of Common Stocks: Principles of Corporate FinanceDocument31 pagesThe Value of Common Stocks: Principles of Corporate FinanceGodson AkwoviahNo ratings yet

- Valuing Stocks: Fundamentals of Corporate FinanceDocument32 pagesValuing Stocks: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Intro 22Document23 pagesIntro 22Asad HaiderNo ratings yet

- Introduction To Corporate Finance and GovernanceDocument18 pagesIntroduction To Corporate Finance and GovernanceMuh BilalNo ratings yet

- Current Assets Current Liabilities Ca CL: Tratio Analysis FormulaeDocument3 pagesCurrent Assets Current Liabilities Ca CL: Tratio Analysis FormulaealshaNo ratings yet

- Financial Health RatiosDocument29 pagesFinancial Health Ratiosmushiechan888No ratings yet

- FM Formulae SheetDocument4 pagesFM Formulae Sheetatishayjjj123No ratings yet

- Ratio_FormulasDocument3 pagesRatio_Formulasakk59No ratings yet

- Financial Ratios at A Glance PDFDocument8 pagesFinancial Ratios at A Glance PDFmohit PathakNo ratings yet

- Financial AnalysisDocument2 pagesFinancial AnalysisdavewagNo ratings yet

- Ratio Analysis ch-6Document11 pagesRatio Analysis ch-6IP MAXNo ratings yet

- Financial Management FormulasDocument5 pagesFinancial Management FormulasDaniel Kahn GillamacNo ratings yet

- Financial Ratios at A GlanceDocument8 pagesFinancial Ratios at A Glance365 Financial AnalystNo ratings yet

- Valuing BondsDocument26 pagesValuing BondsMohammad Taqiyuddin RahmanNo ratings yet

- Analysis and Interpretation of Financial StatementsDocument6 pagesAnalysis and Interpretation of Financial StatementsPaulo Amposta CarpioNo ratings yet

- Financial Statement Analysis and Performance MeasurementDocument6 pagesFinancial Statement Analysis and Performance MeasurementBijaya DhakalNo ratings yet

- Financial Ratio FormulasDocument3 pagesFinancial Ratio FormulasWan ShakwanahNo ratings yet

- Current RatioDocument2 pagesCurrent RatioRujean Salar AltejarNo ratings yet

- The Accounting Cycle: Accruals and Deferrals: Mcgraw-Hill/IrwinDocument42 pagesThe Accounting Cycle: Accruals and Deferrals: Mcgraw-Hill/IrwinDuae ZahraNo ratings yet

- Valuing Bonds: Fundamentals of Corporate FinanceDocument26 pagesValuing Bonds: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- FS Analysis FormulasDocument3 pagesFS Analysis FormulasCzarhiena SantiagoNo ratings yet

- Stracos Notes 1Document1 pageStracos Notes 1bangtan sonyeondanNo ratings yet

- Taepren (.: A (J:SWSR ($) Re)Document3 pagesTaepren (.: A (J:SWSR ($) Re)Beatrice AquinoNo ratings yet

- Financial Ratios TableDocument2 pagesFinancial Ratios TableWiSeVirGoNo ratings yet

- The Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio AnalysisDocument19 pagesThe Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio AnalysispureabbasiNo ratings yet

- Measuring and Evaluating The Performance of Banks and Their Principal CompetitorsDocument28 pagesMeasuring and Evaluating The Performance of Banks and Their Principal CompetitorsMoinul IslamNo ratings yet

- The Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio AnalysisDocument19 pagesThe Use of Financial Ratios Analyzing Liquidity Analyzing Activity Analyzing Debt Analyzing Profitability A Complete Ratio Analysiskowsalya18No ratings yet

- Financial Ratios ExplainedDocument2 pagesFinancial Ratios ExplainedSyed Shariq AliNo ratings yet

- Commonsize Analysis - Horizontal Commonsize Analysis - Vertical Dupont Analysis (Roe)Document4 pagesCommonsize Analysis - Horizontal Commonsize Analysis - Vertical Dupont Analysis (Roe)Sufiana TanNo ratings yet

- Commonsize Analysis - Horizontal Commonsize Analysis - Vertical Dupont Analysis (Roe)Document4 pagesCommonsize Analysis - Horizontal Commonsize Analysis - Vertical Dupont Analysis (Roe)Sufiana TanNo ratings yet

- Formula Sheet - Finance - VTDocument11 pagesFormula Sheet - Finance - VTmariaajudamariaNo ratings yet

- 0.3-Financial Statement AnalysisDocument26 pages0.3-Financial Statement AnalysisMatsuno ChifuyuNo ratings yet

- Managerial Accounting: Cost Volume Profit (CVP) AnalysisDocument19 pagesManagerial Accounting: Cost Volume Profit (CVP) AnalysisRina MartinaNo ratings yet

- Ratios FormulaDocument2 pagesRatios FormulaMURSYIDAH ABD RASIDNo ratings yet

- What Drives Your Return On EquityDocument1 pageWhat Drives Your Return On Equitysilverjade03No ratings yet

- Financial Ratios ExplainedDocument1 pageFinancial Ratios ExplainedMAURICIO CONTRERAS CABALLERONo ratings yet

- Chap 014Document36 pagesChap 014fmj6687No ratings yet

- FINN 117 Ch. 6 - Financial Ratios Formula GuideDocument3 pagesFINN 117 Ch. 6 - Financial Ratios Formula GuidePatrick MendozaNo ratings yet

- The Accounting Cycle: Accruals and Deferrals: Mcgraw-Hill/IrwinDocument45 pagesThe Accounting Cycle: Accruals and Deferrals: Mcgraw-Hill/Irwinazee inmix100% (1)

- 9960 FinancialratiosDocument2 pages9960 FinancialratiosGhelyn GimenezNo ratings yet

- Operating and Financial Leverage: Block, Hirt, and DanielsenDocument31 pagesOperating and Financial Leverage: Block, Hirt, and DanielsenOona NiallNo ratings yet

- The Time Value of Money: Fundamentals of Corporate FinanceDocument36 pagesThe Time Value of Money: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- AccHor 7e CH 03Document36 pagesAccHor 7e CH 03Muh BilalNo ratings yet

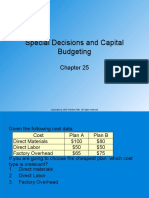

- AccHor 7e CH 25Document24 pagesAccHor 7e CH 25Muh BilalNo ratings yet

- AccHor 7e CH 22Document28 pagesAccHor 7e CH 22Muh BilalNo ratings yet

- AccHor 7e CH 01Document32 pagesAccHor 7e CH 01Muh BilalNo ratings yet

- AccHor 7e CH 02Document28 pagesAccHor 7e CH 02Muh BilalNo ratings yet

- AccHor 7e CH 23Document24 pagesAccHor 7e CH 23Muh BilalNo ratings yet

- AccHor 7e CH 24Document28 pagesAccHor 7e CH 24Muh BilalNo ratings yet

- AccHor 7e CH 20Document22 pagesAccHor 7e CH 20Muh BilalNo ratings yet

- AccHor 7e CH 16Document22 pagesAccHor 7e CH 16Muh BilalNo ratings yet

- AccHor 7e CH 18Document22 pagesAccHor 7e CH 18Muh BilalNo ratings yet

- AccHor 7e CH 15Document22 pagesAccHor 7e CH 15Muh BilalNo ratings yet

- AccHor 7e CH 17Document24 pagesAccHor 7e CH 17Muh BilalNo ratings yet

- AccHor 7e CH 23Document24 pagesAccHor 7e CH 23Muh BilalNo ratings yet

- AccHor 7e CH 21Document25 pagesAccHor 7e CH 21Muh BilalNo ratings yet

- Ch09 Harrison 8e GE SMDocument92 pagesCh09 Harrison 8e GE SMMuh BilalNo ratings yet

- AccHor 7e CH 14Document22 pagesAccHor 7e CH 14Muh BilalNo ratings yet

- AccHor 7e CH 19Document28 pagesAccHor 7e CH 19Muh BilalNo ratings yet

- Ch10 Harrison 8e GE SMDocument73 pagesCh10 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch07 Harrison 8e GE SMDocument87 pagesCh07 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch12 Harrison 8e GE SMDocument87 pagesCh12 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch08 Harrison 8e GE SM (Revised)Document102 pagesCh08 Harrison 8e GE SM (Revised)Muh BilalNo ratings yet

- Ch05 Harrison 8e GE SMDocument73 pagesCh05 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch04 Harrison 8e GE SMDocument73 pagesCh04 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch02 Harrison 8e GE SMDocument96 pagesCh02 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch01 Harrison 8e GE SMDocument63 pagesCh01 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch03 Harrison 8e GE SMDocument113 pagesCh03 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch06 Harrison 8e GE SMDocument87 pagesCh06 Harrison 8e GE SMMuh BilalNo ratings yet

- What We Do and Do Not Know About Finance: Fundamentals of Corporate FinanceDocument3 pagesWhat We Do and Do Not Know About Finance: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Chap 023Document19 pagesChap 023Muh BilalNo ratings yet

- Risk Management: Fundamentals of Corporate FinanceDocument24 pagesRisk Management: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- 50 MCQ SETS on JOB ANALYSISDocument14 pages50 MCQ SETS on JOB ANALYSISChaudhary AdeelNo ratings yet

- Statement of Cash FlowsDocument6 pagesStatement of Cash FlowsJustine VeralloNo ratings yet

- RBI's Vital Role in Regulating India's Economy and Financial SystemDocument2 pagesRBI's Vital Role in Regulating India's Economy and Financial SystemSimran hreraNo ratings yet

- Software Developement Life CycleDocument21 pagesSoftware Developement Life CycleJAI THAPANo ratings yet

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- Information and Resources For Starting A Home-Based Food BusinessDocument2 pagesInformation and Resources For Starting A Home-Based Food BusinessJeff BeckNo ratings yet

- Building Contruction Workers Regulation of Employment and Working Conditions Act 1996Document14 pagesBuilding Contruction Workers Regulation of Employment and Working Conditions Act 1996omarmhusainNo ratings yet

- Optional: Service BulletinDocument8 pagesOptional: Service BulletinDaniil SerovNo ratings yet

- BioPharma Case StudyDocument4 pagesBioPharma Case StudyNaman Chhaya100% (3)

- C&I JSA 09 GeneralDocument1 pageC&I JSA 09 Generalamit kumarNo ratings yet

- Real-Estate Investor's Psychology: Heuristics and Prospect FactorsDocument6 pagesReal-Estate Investor's Psychology: Heuristics and Prospect Factors03217925346No ratings yet

- Export Oriented UnitsDocument10 pagesExport Oriented UnitsMansi GuptaNo ratings yet

- Implementing RBI and RCM to Improve Asset ReliabilityDocument56 pagesImplementing RBI and RCM to Improve Asset ReliabilityKareem RasmyNo ratings yet

- Nike PresentationsDocument54 pagesNike PresentationsSubhan AhmedNo ratings yet

- Target Market AnalysisDocument6 pagesTarget Market AnalysisAllyssa LaquindanumNo ratings yet

- Capital BudgetingDocument87 pagesCapital BudgetingCBSE UGC NET EXAMNo ratings yet

- MBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23Document2 pagesMBA Akshay Arora: SAP ID:80511020627 - : Akshay - Arora27@nmims - Edu.in - Age: 23gautam keswaniNo ratings yet

- Eks 9 en 2015 01 14Document157 pagesEks 9 en 2015 01 14aykutNo ratings yet

- Power Purchase AgreementDocument22 pagesPower Purchase Agreementdark webNo ratings yet

- Business Model CanvasDocument1 pageBusiness Model CanvasMajed OdahNo ratings yet

- Tapas y Cuellos BericapDocument2 pagesTapas y Cuellos BericapMelvin Mateo Rodriguez100% (1)

- The Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasDocument24 pagesThe Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasTitan HerdiantoNo ratings yet

- Asset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutDocument10 pagesAsset-V1 MITx+14.100x+2T2020+Type@Asset+Block@Lecture 9 HandoutcamirandamNo ratings yet

- Ijcs 127281Document34 pagesIjcs 127281Faten bakloutiNo ratings yet

- 30 Free Leed Ap BD+C Sample QuestionsDocument23 pages30 Free Leed Ap BD+C Sample QuestionsSubhranshu PandaNo ratings yet

- Commercial Space Lease LetterDocument1 pageCommercial Space Lease LetterBplo Caloocan100% (3)

- Quiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Document5 pagesQuiz Manajemen Pengadaan - Nisrina Zalfa Farida - 21B505041003Kuro DitNo ratings yet

- Implied JoinDocument4 pagesImplied JoinramyasidNo ratings yet

- 05 Chapter2Document30 pages05 Chapter2Motiram paudelNo ratings yet

- Nepal Health Service Act 2053 BSDocument72 pagesNepal Health Service Act 2053 BSDinesh YadavNo ratings yet