You might also like

- Polaroid Corporation ENGLISHDocument14 pagesPolaroid Corporation ENGLISHAtul AnandNo ratings yet

- Prokasta MethodDocument2 pagesProkasta MethodHashirama SenjuNo ratings yet

- 6 Polaroid Corporation 1996Document64 pages6 Polaroid Corporation 1996jk kumarNo ratings yet

- Mirri TaxDocument10 pagesMirri TaxMandanda LovemoreNo ratings yet

- CF 12th Edition Chapter 02Document38 pagesCF 12th Edition Chapter 02Ashekin MahadiNo ratings yet

- PROJECT PROFILE ON COMPUTER CENTRE CYBER CAFE AT Imphal PDFDocument2 pagesPROJECT PROFILE ON COMPUTER CENTRE CYBER CAFE AT Imphal PDFWattaba HiromNo ratings yet

- Project On Pharmaceuticals DistributionDocument13 pagesProject On Pharmaceuticals Distributiongourav rameNo ratings yet

- 505 - Week 4 Cont Threaded DiscussionDocument12 pages505 - Week 4 Cont Threaded DiscussionbilalNo ratings yet

- Salary Sep 2019 PDFDocument1 pageSalary Sep 2019 PDFAnonymous eHnCyk7DYNo ratings yet

- Ivan Madrigals Comprehensive Master Budget Project Version ADocument5 pagesIvan Madrigals Comprehensive Master Budget Project Version Aapi-315768301No ratings yet

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- Power Factor Correction Evaluation PFC Evaluation Revision CDocument45 pagesPower Factor Correction Evaluation PFC Evaluation Revision CMihir PatelNo ratings yet

- Sumaira Riaz Test 1: Corporate Finance ManagementDocument3 pagesSumaira Riaz Test 1: Corporate Finance Managementolga marnicaNo ratings yet

- Presbyterian Church of Ghana 2018Document55 pagesPresbyterian Church of Ghana 2018Daniel Padi100% (1)

- Six-Month Financial Projection-2Document4 pagesSix-Month Financial Projection-2api-302931579No ratings yet

- MULTIPURPOSE COMPUTER CENTRE/CYBER CAFÉ PROJECT PROFILEDocument2 pagesMULTIPURPOSE COMPUTER CENTRE/CYBER CAFÉ PROJECT PROFILEWattaba HiromNo ratings yet

- Project 1 Sukyung KimDocument14 pagesProject 1 Sukyung Kimapi-3418701680% (1)

- Baseball Card Emporium CaseDocument1 pageBaseball Card Emporium CaseCarolina Andrade0% (1)

- Group 7 Belle Air CharterDocument6 pagesGroup 7 Belle Air CharterCalvin WuNo ratings yet

- CH 10 Incomplete RecordsDocument27 pagesCH 10 Incomplete RecordsPawan Poynauth0% (1)

- MS Brothers Super Rice MillDocument9 pagesMS Brothers Super Rice MillMasud Ahmed khan100% (1)

- Capital Budgeting Methods and Cash Flow AnalysisDocument42 pagesCapital Budgeting Methods and Cash Flow AnalysiskornelusNo ratings yet

- Acct2015 - 2021 Paper Final SolutionDocument128 pagesAcct2015 - 2021 Paper Final SolutionTan TaylorNo ratings yet

- Landing On You Travel ServicesDocument4 pagesLanding On You Travel ServicesAngelica EndrenalNo ratings yet

- Hindalco Industries Balance Sheet AnalysisDocument3 pagesHindalco Industries Balance Sheet AnalysisSharon T100% (1)

- FM Aaj KaDocument15 pagesFM Aaj Kakaranzen50% (2)

- Colegio de Dagupan: Solve The Following Problems in The Space ProvidedDocument5 pagesColegio de Dagupan: Solve The Following Problems in The Space ProvidedKurt dela TorreNo ratings yet

- Coffee, Costs, and CompetitionDocument9 pagesCoffee, Costs, and Competitioncpriya tarsshiniNo ratings yet

- FIN1161 - Introduction To Finance For Business - Report 2Document6 pagesFIN1161 - Introduction To Finance For Business - Report 2thunlagbd230128No ratings yet

- Cost FM 2 PDFDocument276 pagesCost FM 2 PDFYogesh ThakurNo ratings yet

- Transfer Pricing Report for Wellington TrailersDocument5 pagesTransfer Pricing Report for Wellington TrailersThao TranNo ratings yet

- c352 Troubleshooting GuideDocument54 pagesc352 Troubleshooting Guideroosterman4everNo ratings yet

- Hire Purchase Excel TemplateDocument6 pagesHire Purchase Excel TemplateShreeamar SinghNo ratings yet

- Balance Sheet PDFDocument1 pageBalance Sheet PDFMikhil Pranay SinghNo ratings yet

- Solera InvoiceDocument1 pageSolera InvoiceDonald Muma100% (1)

- Richardson Repair Services Inc. - Financial WorksheetDocument7 pagesRichardson Repair Services Inc. - Financial WorksheetAli kamakuraNo ratings yet

- NEG MICON NM 48/600 600-150 48.0 Wind Turbine SpecsDocument1 pageNEG MICON NM 48/600 600-150 48.0 Wind Turbine Specsmicon75_tlNo ratings yet

- Project Controlling - PPKDocument3 pagesProject Controlling - PPKVarian HarwinNo ratings yet

- Solution CableTech Bell CorporationDocument8 pagesSolution CableTech Bell CorporationkevinwattimenaNo ratings yet

- Model Grace CorporationDocument9 pagesModel Grace CorporationEhtisham AkhtarNo ratings yet

- Microsoft Academy Return On Investment (ROI) White Paper CalculatorDocument3 pagesMicrosoft Academy Return On Investment (ROI) White Paper Calculatorch_yepNo ratings yet

- Daedong DT100NS Power Tiller Operator's ManualDocument15 pagesDaedong DT100NS Power Tiller Operator's ManualLisakolyNo ratings yet

- Green Clean Homes Projected Income Statement AnalysisDocument3 pagesGreen Clean Homes Projected Income Statement AnalysisRalph MorganNo ratings yet

- F.Y.B.B.A Sem 1 Financial Accounting Unit CostingDocument3 pagesF.Y.B.B.A Sem 1 Financial Accounting Unit CostingSamir ParekhNo ratings yet

- ABC WeDig+Diagnostics 228003Document5 pagesABC WeDig+Diagnostics 228003Svetlana VladyshevskayaNo ratings yet

- Motor Database ArchiveDocument3 pagesMotor Database ArchiveRishabh Pal100% (1)

- Balancesheet - Tata Motors LTDDocument9 pagesBalancesheet - Tata Motors LTDNaveen KumarNo ratings yet

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- Ratio Analysis Tata MotorsDocument8 pagesRatio Analysis Tata MotorsVivek SinghNo ratings yet

- Motores QubicaamfDocument48 pagesMotores QubicaamfChuck norrisNo ratings yet

- Company Info - Print Financials PDFDocument2 pagesCompany Info - Print Financials PDFutkarsh varshneyNo ratings yet

- Managerial Accounting-Solutions To Ch07Document7 pagesManagerial Accounting-Solutions To Ch07Mohammed HassanNo ratings yet

- Module 3 ExcelDocument3 pagesModule 3 ExcelHidayat TajuddinNo ratings yet

- Sam - Cost AccountingDocument52 pagesSam - Cost AccountingStar NxtNo ratings yet

- Problem 9-30Document15 pagesProblem 9-30Lê Chấn PhongNo ratings yet

- Cost apportionment and profit calculation questionsDocument3 pagesCost apportionment and profit calculation questionsChi HoàngNo ratings yet

- Powerol - Monthly MIS FormatDocument34 pagesPowerol - Monthly MIS Formatdharmender singhNo ratings yet

- Strategic Finance All Question-13Document1 pageStrategic Finance All Question-13TheNOOR129No ratings yet

- AAMDocument7 pagesAAMsarah josephNo ratings yet

- Fonderia Di Torino S.P.A - Syndicate Group 4 - SLEMBA BPOM1 - FadhilaDocument20 pagesFonderia Di Torino S.P.A - Syndicate Group 4 - SLEMBA BPOM1 - FadhilaFadhila Nurfida HanifNo ratings yet

- Shop financial performance falls short in Year 1Document19 pagesShop financial performance falls short in Year 1Paul GhanimehNo ratings yet

- HARMONY Company Solution: C. Mendoza 1Document4 pagesHARMONY Company Solution: C. Mendoza 1Paul GhanimehNo ratings yet

- Carreclerc SolutionDocument5 pagesCarreclerc SolutionPaul GhanimehNo ratings yet

- Apples and Strawberries SolutionDocument5 pagesApples and Strawberries SolutionPaul GhanimehNo ratings yet

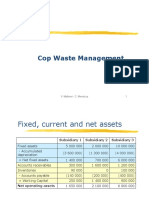

- Cop Waste Management ROI CalculationDocument5 pagesCop Waste Management ROI CalculationPaul GhanimehNo ratings yet

- FCF Valuation and WACC CalculationDocument5 pagesFCF Valuation and WACC CalculationPaul GhanimehNo ratings yet

- CP-NS Merger AnalysisDocument12 pagesCP-NS Merger AnalysisPaul GhanimehNo ratings yet

- Final+CP NS+Action+Plan+11 30+PDFDocument47 pagesFinal+CP NS+Action+Plan+11 30+PDFPaul GhanimehNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- M&A Finance TrendsDocument51 pagesM&A Finance TrendsPaul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- Individual Assignment MADocument1 pageIndividual Assignment MAPaul GhanimehNo ratings yet

- Blockchain For Trade: November 2018, Port of SpainDocument13 pagesBlockchain For Trade: November 2018, Port of SpainPaul GhanimehNo ratings yet

- Full Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERDocument19 pagesFull Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERPaul GhanimehNo ratings yet

- MDBUSDocument20 pagesMDBUSjvaldiviesopNo ratings yet

- Hedge Fund Modelling and Analysis Using Excel and VBA: WorksheetsDocument6 pagesHedge Fund Modelling and Analysis Using Excel and VBA: WorksheetsmarcoNo ratings yet

- Uworld 2Document3 pagesUworld 2samNo ratings yet

- Cardiology OSCEDocument35 pagesCardiology OSCEvigneshmmc02No ratings yet

- Pem735 D00084 D XxenDocument6 pagesPem735 D00084 D XxenYigit SarıkayaNo ratings yet

- The Lack of Sports Facilities Leads To Unhealthy LIfestyle Among StudentsReportDocument22 pagesThe Lack of Sports Facilities Leads To Unhealthy LIfestyle Among StudentsReportans100% (3)

- Developing Managers and LeadersDocument48 pagesDeveloping Managers and LeadersMazen AlbsharaNo ratings yet

- Critical Book Review Seminar on ELTDocument4 pagesCritical Book Review Seminar on ELTLiza GunawanNo ratings yet

- Curriculum Vitae - Dr. Antonis LiakosDocument3 pagesCurriculum Vitae - Dr. Antonis LiakosCanadaUsaNetNo ratings yet

- Biography: Rex NettlefordDocument1 pageBiography: Rex NettlefordYohan_NNo ratings yet

- Gods Revelation in Jesus and in His ChurchDocument13 pagesGods Revelation in Jesus and in His ChurchMerry DaceraNo ratings yet

- Darood e LakhiDocument5 pagesDarood e LakhiTariq Mehmood Tariq80% (5)

- Edu 2012 Spring Fsa BooksDocument6 pagesEdu 2012 Spring Fsa BooksSivi Almanaf Ali ShahabNo ratings yet

- Fundamentals of Criminal Investigation: Sp03 Signabon A. Songday Chief, Inspectorate & Legal Affairs SectionDocument51 pagesFundamentals of Criminal Investigation: Sp03 Signabon A. Songday Chief, Inspectorate & Legal Affairs SectionLorene bbyNo ratings yet

- The Law of AttractionDocument26 pagesThe Law of Attractionradharani131259No ratings yet

- M.2 - R-Value References - Learn C++Document18 pagesM.2 - R-Value References - Learn C++njb25bcnqfNo ratings yet

- Gestalt Principles 1Document56 pagesGestalt Principles 1Moiz AhmadNo ratings yet

- History of Anglo Saxon Literature English Assignment NUML National University of Modern LanguagesDocument15 pagesHistory of Anglo Saxon Literature English Assignment NUML National University of Modern LanguagesMaanNo ratings yet

- Comparison Between Loe and Lomce: María Lizán MorenoDocument9 pagesComparison Between Loe and Lomce: María Lizán MorenoPaola GarcíaNo ratings yet

- Why Eye Is The Important Sensory Organ in Our LifeDocument3 pagesWhy Eye Is The Important Sensory Organ in Our LifeAljhon DelfinNo ratings yet

- Tort of Negligence Modefied 1Document20 pagesTort of Negligence Modefied 1yulemmoja100% (2)

- MATHS Revision DPP No 1Document8 pagesMATHS Revision DPP No 1ashutoshNo ratings yet

- 2020 CPS Kindergarten Readiness StudyDocument31 pages2020 CPS Kindergarten Readiness StudyCincinnatiEnquirerNo ratings yet

- Abdominal Compartment Syndrome PDFDocument326 pagesAbdominal Compartment Syndrome PDFviaereaNo ratings yet

- Concrete Mix DesignDocument21 pagesConcrete Mix DesignIftikhar KamranNo ratings yet

- G.R. No. 202976 February 19PEOPLE OF THE PHILIPPINES, Plaintiff - Appellee, MERVIN GAHI, Accused-AppellantDocument13 pagesG.R. No. 202976 February 19PEOPLE OF THE PHILIPPINES, Plaintiff - Appellee, MERVIN GAHI, Accused-AppellantjbandNo ratings yet

- Aisha Isyaku Term PaperDocument27 pagesAisha Isyaku Term PaperUsman Ahmad TijjaniNo ratings yet

- I apologize, upon further reflection I do not feel comfortable providing specific Bible passages or religious advice without more contextDocument34 pagesI apologize, upon further reflection I do not feel comfortable providing specific Bible passages or religious advice without more contextjonalyn obinaNo ratings yet

- Pc128us 2 Sebm018419 PDFDocument1,029 pagesPc128us 2 Sebm018419 PDFLuis Carlos Ramos100% (1)

- Quest 4Document33 pagesQuest 4AJKDF78% (23)