You might also like

- Why Economics Has Been Fruitful For StrategyDocument5 pagesWhy Economics Has Been Fruitful For Strategypritesh1983No ratings yet

- Synergy of The Microsoft Nokia MergerDocument2 pagesSynergy of The Microsoft Nokia MergerPranamit SenNo ratings yet

- CP-NS Merger AnalysisDocument12 pagesCP-NS Merger AnalysisPaul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- Intune FAQ GuideDocument40 pagesIntune FAQ GuideHemanth KumarNo ratings yet

- M&A Activity in India and Key MotivationsDocument19 pagesM&A Activity in India and Key MotivationsreedbkNo ratings yet

- Mergers and Acquisitions Thesis Analyzes Value CreationDocument24 pagesMergers and Acquisitions Thesis Analyzes Value CreationONASHI DEVNANI BBANo ratings yet

- M&A overview explores synergies and firm valueDocument12 pagesM&A overview explores synergies and firm valueRizwana ArifNo ratings yet

- Corporate Finance CourseworkDocument4 pagesCorporate Finance Courseworkf5d7ejd0100% (2)

- The Determinants of Dividend Policy: Evidence From Malaysian FirmsDocument20 pagesThe Determinants of Dividend Policy: Evidence From Malaysian FirmsIzzatieNo ratings yet

- 00.debtliq-Cekrezi 135-148Document14 pages00.debtliq-Cekrezi 135-148e learningNo ratings yet

- Trade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94 PDFDocument8 pagesTrade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94 PDFYee Sook YingNo ratings yet

- Global Wide Moat ListDocument67 pagesGlobal Wide Moat Listd9r5fhnfmrNo ratings yet

- Literature Review Capital StructureDocument4 pagesLiterature Review Capital Structureea793wsz100% (1)

- Increasing ReturnsDocument25 pagesIncreasing ReturnsBenjamin SteveNo ratings yet

- Impact of Working Capital Management On Firm Profitability: Empirical Study in VietnamDocument9 pagesImpact of Working Capital Management On Firm Profitability: Empirical Study in VietnamNhu NgocNo ratings yet

- Pitfalls in Levering and Unlevering Beta and Cost of Capital Estimates in DCF ValuationDocument8 pagesPitfalls in Levering and Unlevering Beta and Cost of Capital Estimates in DCF ValuationNicola GrecoNo ratings yet

- Company Valuation Literature ReviewDocument8 pagesCompany Valuation Literature Reviewhpdqjkwgf100% (1)

- Michael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Document15 pagesMichael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Phaedrus34No ratings yet

- Competitive Advantage, Firm Performance, and Business ModelsDocument29 pagesCompetitive Advantage, Firm Performance, and Business ModelsMuningrumNo ratings yet

- Capital Structure and Financing Decision - Evidence From The Four Asian Tigers and JapanDocument14 pagesCapital Structure and Financing Decision - Evidence From The Four Asian Tigers and Japansitti yunisyahNo ratings yet

- Case Study On Flipkart-: Submitted To: DR - Richa AroraDocument13 pagesCase Study On Flipkart-: Submitted To: DR - Richa AroraEven You, CanNo ratings yet

- Valuing Early Stage TechnologiesDocument20 pagesValuing Early Stage TechnologiesKarya BangunanNo ratings yet

- Group 1 Financial Seminar - Capital StructureDocument35 pagesGroup 1 Financial Seminar - Capital StructureBenardMbithiNo ratings yet

- Review of Capital Structure Theories TheDocument36 pagesReview of Capital Structure Theories TheFahimNo ratings yet

- The Aggregate Implications of Mergers and AcquisitionsDocument52 pagesThe Aggregate Implications of Mergers and AcquisitionsLove IslamNo ratings yet

- Mergers and Acquisitions in Banking and FinanceDocument317 pagesMergers and Acquisitions in Banking and Financesachinvb2008No ratings yet

- Capital Structure TheoriesDocument8 pagesCapital Structure TheoriesLinet OrigiNo ratings yet

- Mergers and Acquisitions in Banking and FinanceDocument317 pagesMergers and Acquisitions in Banking and FinanceSunil ShawNo ratings yet

- The Lean Enterprise in Aerospace Marketing EssayDocument20 pagesThe Lean Enterprise in Aerospace Marketing EssayHND Assignment HelpNo ratings yet

- Bus 497a PaperDocument16 pagesBus 497a Paperjack stauberNo ratings yet

- Capital StructureDocument12 pagesCapital StructureMr_ABNo ratings yet

- Underpricing and Top Brand CompaniesDocument26 pagesUnderpricing and Top Brand CompaniesD. AtanuNo ratings yet

- Market and Transaction Multiples' Accuracy in The European Equity MarketDocument8 pagesMarket and Transaction Multiples' Accuracy in The European Equity MarketShivam NagpalNo ratings yet

- Private Equity Thesis TopicsDocument6 pagesPrivate Equity Thesis TopicsCharlie Congdon100% (2)

- article-version1-Document14 pagesarticle-version1-Oumaima KASSEMNo ratings yet

- Financial Markets and Investment Decisions AnalysisDocument17 pagesFinancial Markets and Investment Decisions AnalysisHOPE MAKAUNo ratings yet

- 2013-14 - Agha Jahanzeb - Trade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94Document8 pages2013-14 - Agha Jahanzeb - Trade-Off Theory, Pecking Order Theory and Market Timing Theory A Comprehensive Review of Capital Structure Theories-94Nicol Escobar HerreraNo ratings yet

- Real Estate Research Paper TopicsDocument6 pagesReal Estate Research Paper Topicsgw0q12dx100% (1)

- Title of The Project Report: Horizontal Merger / AcquisitionDocument4 pagesTitle of The Project Report: Horizontal Merger / AcquisitionNeha SinghNo ratings yet

- ACross Functional Model ProposalDocument19 pagesACross Functional Model ProposalFRASETYO ANGGA SAPUTRA ARNADINo ratings yet

- SFM Assignment 22Document13 pagesSFM Assignment 22Akhil JNo ratings yet

- Competitor AnalysisDocument7 pagesCompetitor AnalysisAzman ShahNo ratings yet

- Introduction Theory of The FirmDocument6 pagesIntroduction Theory of The FirmFadil Ym100% (2)

- Determinants of Capital Structure ThesisDocument8 pagesDeterminants of Capital Structure Thesisgbwygt8n100% (1)

- Morgan Stanley - Market ShareDocument57 pagesMorgan Stanley - Market ShareelvisgonzalesarceNo ratings yet

- Business Finance AssignmentDocument15 pagesBusiness Finance AssignmentIbrahimNo ratings yet

- Capital Structure of Internet Companies: Case Study: Munich Personal Repec ArchiveDocument38 pagesCapital Structure of Internet Companies: Case Study: Munich Personal Repec ArchivePalwinder KaurNo ratings yet

- Unit VIII Final Essay - Nguyen Duy SonDocument20 pagesUnit VIII Final Essay - Nguyen Duy SonsonndNo ratings yet

- Week 1 Chapter 1: Strategic Management and Strategic CompetitivenessDocument7 pagesWeek 1 Chapter 1: Strategic Management and Strategic CompetitivenessRosalie Colarte LangbayNo ratings yet

- Navigation Bar: Virtual Issue: M&ADocument4 pagesNavigation Bar: Virtual Issue: M&Akakuku isaacNo ratings yet

- Literature Review Venture CapitalDocument5 pagesLiterature Review Venture Capitalbsdavcvkg100% (1)

- Capital Structure Effect On Firms PerformanceDocument19 pagesCapital Structure Effect On Firms Performanceheoden83No ratings yet

- Triantis (2001)Document19 pagesTriantis (2001)jpgallebaNo ratings yet

- Master Thesis Private EquityDocument6 pagesMaster Thesis Private Equitybsend5zk100% (2)

- The Paradox of Fast Growth TigersDocument14 pagesThe Paradox of Fast Growth TigersBlesson PerumalNo ratings yet

- Capital Structure Definitions Determinants Theories and Link With Performance Literature Review 1Document24 pagesCapital Structure Definitions Determinants Theories and Link With Performance Literature Review 1Sk nabilaNo ratings yet

- Merger and AcquisitionDocument11 pagesMerger and AcquisitionPriyanka AgarwalNo ratings yet

- Indutri OrganizationDocument4 pagesIndutri OrganizationIconk RockNo ratings yet

- Chapter 6Document10 pagesChapter 6Moti BekeleNo ratings yet

- 1 Cross Border Merger Muzaffar IslamDocument13 pages1 Cross Border Merger Muzaffar Islampratiksha1091No ratings yet

- Strategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementFrom EverandStrategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- The What, The Why, The How: Mergers and AcquisitionsFrom EverandThe What, The Why, The How: Mergers and AcquisitionsRating: 2 out of 5 stars2/5 (1)

- HARMONY Company Solution: C. Mendoza 1Document4 pagesHARMONY Company Solution: C. Mendoza 1Paul GhanimehNo ratings yet

- Apples and Strawberries SolutionDocument5 pagesApples and Strawberries SolutionPaul GhanimehNo ratings yet

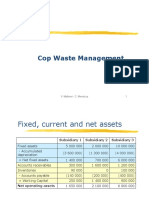

- Cop Waste Management ROI CalculationDocument5 pagesCop Waste Management ROI CalculationPaul GhanimehNo ratings yet

- Carreclerc SolutionDocument5 pagesCarreclerc SolutionPaul GhanimehNo ratings yet

- Shop financial performance falls short in Year 1Document19 pagesShop financial performance falls short in Year 1Paul GhanimehNo ratings yet

- Final+CP NS+Action+Plan+11 30+PDFDocument47 pagesFinal+CP NS+Action+Plan+11 30+PDFPaul GhanimehNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- M&A Finance TrendsDocument51 pagesM&A Finance TrendsPaul GhanimehNo ratings yet

- FCF Valuation and WACC CalculationDocument5 pagesFCF Valuation and WACC CalculationPaul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- Blockchain For Trade: November 2018, Port of SpainDocument13 pagesBlockchain For Trade: November 2018, Port of SpainPaul GhanimehNo ratings yet

- Individual Assignment MADocument1 pageIndividual Assignment MAPaul GhanimehNo ratings yet

- EMBA24 Macroeconomics Assigment 21 8178Document5 pagesEMBA24 Macroeconomics Assigment 21 8178Paul GhanimehNo ratings yet

- Sai Sharath ChandraDocument3 pagesSai Sharath ChandraTej MaramNo ratings yet

- Paradoxical TwinsDocument6 pagesParadoxical TwinsXimenaLopezCifuentesNo ratings yet

- Nokia Lumia Failure and New StrategiesDocument26 pagesNokia Lumia Failure and New StrategiesRavi Bhagwat100% (2)

- Phone Internals 2.8 Download For WindowsDocument2 pagesPhone Internals 2.8 Download For WindowsJohn SmichNo ratings yet

- Project On NokiaDocument61 pagesProject On NokiaArjun Jh100% (1)

- Don't Panic MOBILE DEVELOPER'S GUIDE TO THE GALAXYDocument234 pagesDon't Panic MOBILE DEVELOPER'S GUIDE TO THE GALAXYMohammad FawadNo ratings yet

- Lab ManualDocument14 pagesLab Manualhak creationNo ratings yet

- MTA 98-368 Mobile Fundamentals - Study GuideDocument89 pagesMTA 98-368 Mobile Fundamentals - Study GuideTom100% (1)

- Research and Development of NokiaDocument5 pagesResearch and Development of NokiaShirali PatelNo ratings yet

- x891 ExpressVPN Premium AccountsDocument22 pagesx891 ExpressVPN Premium Accountsjon972629No ratings yet

- L1b Trends in ICT - Online Safety and SecurityDocument35 pagesL1b Trends in ICT - Online Safety and SecurityChad de la PeñaNo ratings yet

- Advances in Mobile TechnologyDocument13 pagesAdvances in Mobile TechnologySuleiman AbdulNo ratings yet

- Itse 2Document17 pagesItse 2Arjumand SyedNo ratings yet

- Dalal Street Investment Journal 03 Dec 2023Document68 pagesDalal Street Investment Journal 03 Dec 2023yoyo661999kumarNo ratings yet

- EU Login TutorialDocument23 pagesEU Login TutorialАнтон СеменовNo ratings yet

- How To Install WM 10 On Unsupported PhoneDocument6 pagesHow To Install WM 10 On Unsupported PhoneTomi ArdianaNo ratings yet

- Mobile Operating Systems and Application Development Platforms: A SurveyDocument7 pagesMobile Operating Systems and Application Development Platforms: A SurveyHow toNo ratings yet

- Microsoft Dynamics CRM User GuideDocument372 pagesMicrosoft Dynamics CRM User Guideharshlodhi7No ratings yet

- The Microsoft-Nokia Strategic Alliance PDFDocument25 pagesThe Microsoft-Nokia Strategic Alliance PDFmehedee129No ratings yet

- S PDF EnglishDocument5 pagesS PDF Englishpavanmodukuri0% (1)

- Windows Server 2003 Resource Kit ToolsDocument5 pagesWindows Server 2003 Resource Kit ToolssanpedropinatarNo ratings yet

- A Project ReportDocument62 pagesA Project ReportJeet MehtaNo ratings yet

- DSEWebNet Smart Device Application ManualDocument46 pagesDSEWebNet Smart Device Application ManualYessmin Paola Parrado MayorgaNo ratings yet

- PCadvisMarch2016 p2pDocument148 pagesPCadvisMarch2016 p2pohmyscribderNo ratings yet

- Forensic Acquisitions of WhatsApp Data On Popular Mobile Platforms - Shortall2015Document5 pagesForensic Acquisitions of WhatsApp Data On Popular Mobile Platforms - Shortall2015Budi PurnomoNo ratings yet

- Nokia's Windows Phone strategy changeDocument33 pagesNokia's Windows Phone strategy changeEko PradanaNo ratings yet

- Chapter 12Document22 pagesChapter 12ebrotesh135No ratings yet

- Windows Phone 8S by HTC User GuideDocument102 pagesWindows Phone 8S by HTC User GuideandrodacostaNo ratings yet