You might also like

- Gross MarginDocument2 pagesGross MarginEDxColdBloodedNo ratings yet

- 21.08.2020 L11-12Document10 pages21.08.2020 L11-12sajedulNo ratings yet

- 21.08.2020 L11-12Document10 pages21.08.2020 L11-12sajedulNo ratings yet

- Average Payable 365 Average Payable Period Annual Purchase Average Inventory 365 Inventory Holding Period Cogs Average Receivable 365 Receivable Collection Period Annual SalesDocument10 pagesAverage Payable 365 Average Payable Period Annual Purchase Average Inventory 365 Inventory Holding Period Cogs Average Receivable 365 Receivable Collection Period Annual SalessajedulNo ratings yet

- I. ANALYSIS. Assess The Current Status of The Company by Referring To The Given Problem andDocument3 pagesI. ANALYSIS. Assess The Current Status of The Company by Referring To The Given Problem andTRISHA NICOLE NISPEROSNo ratings yet

- Chapter 5Document15 pagesChapter 5khodorNo ratings yet

- Assignment 1Document42 pagesAssignment 1Second FloorNo ratings yet

- Horizontal and Vertical AnalysisDocument5 pagesHorizontal and Vertical AnalysisAshley Rouge Capati QuirozNo ratings yet

- Table 1 Seven Flags Manufacturing Sales Information Large Medium Small TotalDocument9 pagesTable 1 Seven Flags Manufacturing Sales Information Large Medium Small TotalAliza RizviNo ratings yet

- Accounting For Manager - Module 9Document7 pagesAccounting For Manager - Module 9Godz gAMERNo ratings yet

- Assumptions - : Amazon Cashflow & Profit ForecastDocument22 pagesAssumptions - : Amazon Cashflow & Profit Forecastlengyianchua206No ratings yet

- ManAc Midterms Chuckie ChukieDocument2 pagesManAc Midterms Chuckie ChukieVAUGHN MARTINEZNo ratings yet

- Fixed Assets Amount Depreciation (Years) Notes: You Are Fully Funded (Balanced)Document4 pagesFixed Assets Amount Depreciation (Years) Notes: You Are Fully Funded (Balanced)Paulo TorresNo ratings yet

- ANALYSISDocument1 pageANALYSISLilacNo ratings yet

- Practice Problem 2Document5 pagesPractice Problem 2panda 1No ratings yet

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgNo ratings yet

- Problem 16-27 Joint-Cost Allocation, Sales Value, Physical Measure, and NRV MethodsDocument8 pagesProblem 16-27 Joint-Cost Allocation, Sales Value, Physical Measure, and NRV MethodsVon Andrei MedinaNo ratings yet

- Sothin and SonsDocument16 pagesSothin and SonsDicksonNo ratings yet

- Moodle 3 Group 14Document6 pagesMoodle 3 Group 14Thơ TrầnNo ratings yet

- Enterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13Document20 pagesEnterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13KabeerMalikNo ratings yet

- WOODDocument12 pagesWOODJayson ReyesNo ratings yet

- Aurora TextileDocument17 pagesAurora Textilexinz1313100% (1)

- Muhammad Luthfi Mahendra - 2001036085 - Tugas 5Document5 pagesMuhammad Luthfi Mahendra - 2001036085 - Tugas 5luthfi mahendraNo ratings yet

- Hotel Financial StatementsDocument27 pagesHotel Financial StatementsVera Yuk86% (7)

- Forecast Ets ExampleDocument12 pagesForecast Ets ExampleAbhinav PrakashNo ratings yet

- FABM2 - QuizDocument4 pagesFABM2 - QuizlabayanjoshuaNo ratings yet

- Hafiz Muhammad Maaz MBL (64287) AFS ProjectDocument13 pagesHafiz Muhammad Maaz MBL (64287) AFS ProjectMaaz MahmoodNo ratings yet

- Exerciese of Chapter Three (Solution)Document15 pagesExerciese of Chapter Three (Solution)Mohammad Al AkoumNo ratings yet

- Style IncDocument8 pagesStyle IncShahzaib MaharNo ratings yet

- ASYNCHRONOUS ACTIVITY 4 WorksheetsDocument12 pagesASYNCHRONOUS ACTIVITY 4 WorksheetsAbejero Trisha Nicole A.No ratings yet

- Feasib IS - 25022018Document56 pagesFeasib IS - 25022018Llyod Francis LaylayNo ratings yet

- CH 15Document56 pagesCH 15Quỳnh Anh Bùi ThịNo ratings yet

- Week 8 (Unit 7) - Tutorial Solutions: Review QuestionDocument10 pagesWeek 8 (Unit 7) - Tutorial Solutions: Review QuestionSheenam SinghNo ratings yet

- Macrs Depreciation: New Smart Phone Calculation AnalysisDocument4 pagesMacrs Depreciation: New Smart Phone Calculation AnalysisErro Jaya RosadyNo ratings yet

- Case StudyDocument3 pagesCase StudyJamshidbek OdiljonovNo ratings yet

- Scenario A Sales Price Profit Margin Target Cost Actual Cost Cost Gap Expected Sales VolDocument12 pagesScenario A Sales Price Profit Margin Target Cost Actual Cost Cost Gap Expected Sales VolunveiledtopicsNo ratings yet

- 02 WMT 2010 FiveYear SummaryDocument1 page02 WMT 2010 FiveYear SummaryNeha ChoudharyNo ratings yet

- Aw 2021 2023Document3 pagesAw 2021 2023abdul.elgoharyNo ratings yet

- RBS Case StudyDocument2 pagesRBS Case StudyVanshika Srivastava 17IFT017100% (1)

- Garcia Jerico 04labDocument2 pagesGarcia Jerico 04labgarciajerico42No ratings yet

- BEP - Breakeven Point ، نقطة تعادلDocument4 pagesBEP - Breakeven Point ، نقطة تعادلSalah HusseinNo ratings yet

- Sharing Sheet Hallstead JewelersDocument11 pagesSharing Sheet Hallstead JewelersHarpreet SinghNo ratings yet

- Week 2 (3chapter3financeDocument9 pagesWeek 2 (3chapter3financeEllen Joy PenieroNo ratings yet

- Ss 3Document32 pagesSs 3Trần Nguyễn Quỳnh GiaoNo ratings yet

- PERMALINO - Learning Activity 9 - Composite BEP AnalysisDocument2 pagesPERMALINO - Learning Activity 9 - Composite BEP AnalysisAra Joyce PermalinoNo ratings yet

- Tetley Brand Valuation Spreadsheets Blank 2022 23Document2 pagesTetley Brand Valuation Spreadsheets Blank 2022 23Kanika SubbaNo ratings yet

- Prestige Telephone CompanyDocument8 pagesPrestige Telephone CompanyRiandy Ar RasyidNo ratings yet

- Budgeting ProblemDocument7 pagesBudgeting ProblemBest Girl RobinNo ratings yet

- Sugggested Solution To Wk5 TuteDocument3 pagesSugggested Solution To Wk5 TuteArwa AhmedNo ratings yet

- Suggested Solution To Week 5 Tutorial Questions 3.1Document3 pagesSuggested Solution To Week 5 Tutorial Questions 3.1A RNo ratings yet

- Bill FrenchDocument4 pagesBill Frenchabigail franciscoNo ratings yet

- Inventory and Recievables FormulasDocument7 pagesInventory and Recievables FormulasJoshua CabinasNo ratings yet

- Customer Profitability AnalysisDocument1 pageCustomer Profitability AnalysisAdrianaNo ratings yet

- Entrep - 3Document2 pagesEntrep - 3Kyle josonNo ratings yet

- Manage Finance - 2Document4 pagesManage Finance - 2Aileen KhorNo ratings yet

- Dietrich Farms - Worksheet 2Document39 pagesDietrich Farms - Worksheet 2spam.ml2023No ratings yet

- Financial Model of Infosys: Revenue Ebitda Net IncomeDocument32 pagesFinancial Model of Infosys: Revenue Ebitda Net IncomePrabhdeep Dadyal100% (1)

- I. Operating Statement: (To Be Filled by The Dealing Group From Balance Sheet / Projections)Document18 pagesI. Operating Statement: (To Be Filled by The Dealing Group From Balance Sheet / Projections)CA DïvYã PrÁkàsh JäîswãlNo ratings yet

- Strategic Management and AccountingDocument10 pagesStrategic Management and AccountingHassaan HunaidNo ratings yet

- Carreclerc SolutionDocument5 pagesCarreclerc SolutionPaul GhanimehNo ratings yet

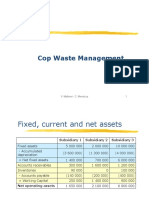

- Cop Waste Management SolutionDocument5 pagesCop Waste Management SolutionPaul GhanimehNo ratings yet

- CP & NS Merger Case - GRP 1Document12 pagesCP & NS Merger Case - GRP 1Paul GhanimehNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- Ebit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Document5 pagesEbit Capex Change in WC FCF: Risk Free Rate 1.67% Market Return (S&P 500) 9.30% Beta 1.13Paul GhanimehNo ratings yet

- MA Material Oct 2021Document51 pagesMA Material Oct 2021Paul GhanimehNo ratings yet

- Space Star CaseDocument8 pagesSpace Star CasePaul GhanimehNo ratings yet

- Full Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERDocument19 pagesFull Paper VALUATION OF TARGET FIRMS IN MERGERS AND ACQUISITIONS A CASE STUDY ON MERGERPaul GhanimehNo ratings yet

- Blockchain For Trade: November 2018, Port of SpainDocument13 pagesBlockchain For Trade: November 2018, Port of SpainPaul GhanimehNo ratings yet

- Invoice Ce 2019 12 IVDocument8 pagesInvoice Ce 2019 12 IVMoussa NdourNo ratings yet

- BattleRope Ebook FinalDocument38 pagesBattleRope Ebook FinalAnthony Dinicolantonio100% (1)

- G12 PR1 AsDocument34 pagesG12 PR1 Asjaina rose yambao-panerNo ratings yet

- Chapter 23 AP World History NotesDocument6 pagesChapter 23 AP World History NotesWesley KoerberNo ratings yet

- Far 1 - Activity 1 - Sept. 09, 2020 - Answer SheetDocument4 pagesFar 1 - Activity 1 - Sept. 09, 2020 - Answer SheetAnonn100% (1)

- Overall Structure and Stock Phrase TemplateDocument16 pagesOverall Structure and Stock Phrase Templatesangeetha Bajanthri C100% (1)

- Cluster University of Jammu: Title: English Anthology and GrammarDocument2 pagesCluster University of Jammu: Title: English Anthology and GrammarDÁRK GAMINGNo ratings yet

- Ocr Graphics Gcse CourseworkDocument6 pagesOcr Graphics Gcse Courseworkzys0vemap0m3100% (2)

- Educational Metamorphosis Journal Vol 2 No 1Document150 pagesEducational Metamorphosis Journal Vol 2 No 1Nau RichoNo ratings yet

- Linear Arrangement 3rdDocument30 pagesLinear Arrangement 3rdSonu BishtNo ratings yet

- Voucher-Zona Wifi-@@2000 - 3jam-Up-764-04.24.24Document10 pagesVoucher-Zona Wifi-@@2000 - 3jam-Up-764-04.24.24AminudinNo ratings yet

- Theoretical Foundations of NursingDocument22 pagesTheoretical Foundations of Nursingattilaabiidn100% (3)

- Jain Gayatri MantraDocument3 pagesJain Gayatri MantraShil9No ratings yet

- D78846GC20 sg2Document356 pagesD78846GC20 sg2hilordNo ratings yet

- Week 4 CasesDocument38 pagesWeek 4 CasesJANNNo ratings yet

- CH 2 & CH 3 John R. Schermerhorn - Management-Wiley (2020)Document9 pagesCH 2 & CH 3 John R. Schermerhorn - Management-Wiley (2020)Muhammad Fariz IbrahimNo ratings yet

- The Christian Life ProgramDocument28 pagesThe Christian Life ProgramRalph Christer MaderazoNo ratings yet

- Ais Activiy Chapter 5 PDFDocument4 pagesAis Activiy Chapter 5 PDFAB CloydNo ratings yet

- What Is Innovation A ReviewDocument33 pagesWhat Is Innovation A ReviewAnonymous EnIdJONo ratings yet

- NursesExperiencesofGriefFollowing28 8 2017thepublishedDocument14 pagesNursesExperiencesofGriefFollowing28 8 2017thepublishedkathleen PerezNo ratings yet

- Avatar Legends The Roleplaying Game 1 12Document12 pagesAvatar Legends The Roleplaying Game 1 12azeaze0% (1)

- Waterfront Development Goals and ObjectivesDocument2 pagesWaterfront Development Goals and ObjectivesShruthi Thakkar100% (1)

- List of Festivals in India - WikipediaDocument13 pagesList of Festivals in India - WikipediaRashmi RaviNo ratings yet

- Nurse Implemented Goal Directed Strategy To.97972Document7 pagesNurse Implemented Goal Directed Strategy To.97972haslinaNo ratings yet

- Compare and Contrast Two Cultures Celebrate Between Bali and JavaDocument1 pageCompare and Contrast Two Cultures Celebrate Between Bali and JavaqonitazmiNo ratings yet

- Second ConditionalDocument1 pageSecond ConditionalSilvana MiñoNo ratings yet

- K 46 Compact Spinning Machine Brochure 2530-V3 75220 Original English 75220Document28 pagesK 46 Compact Spinning Machine Brochure 2530-V3 75220 Original English 75220Pradeep JainNo ratings yet

- AMU BALLB (Hons.) 2018 SyllabusDocument13 pagesAMU BALLB (Hons.) 2018 SyllabusA y u s hNo ratings yet

- ABC of Effective WritingDocument4 pagesABC of Effective Writingprada85No ratings yet

- 2009FallCatalog PDFDocument57 pages2009FallCatalog PDFMarta LugarovNo ratings yet