You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- BI1001268978 - 1800792430MHC12023 - 06062023 - 1421 (1) MaxicareDocument1 pageBI1001268978 - 1800792430MHC12023 - 06062023 - 1421 (1) MaxicareJanet CafrancaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 1.3.1. Problems - Hoba - General Transactions IllustrationDocument15 pages1.3.1. Problems - Hoba - General Transactions IllustrationJane DizonNo ratings yet

- 1.1.2. Hoba - General TransactionsDocument26 pages1.1.2. Hoba - General TransactionsJane DizonNo ratings yet

- Task 1 Stratbusana Holy Angel UniversityDocument3 pagesTask 1 Stratbusana Holy Angel UniversityJane DizonNo ratings yet

- Accounting FinanceDocument2 pagesAccounting FinanceJane DizonNo ratings yet

- 1.1.1. Hoba - General TransactionsDocument29 pages1.1.1. Hoba - General TransactionsJane DizonNo ratings yet

- Dividends Act 1Document1 pageDividends Act 1Jane DizonNo ratings yet

- 4 AreasDocument3 pages4 AreasJane DizonNo ratings yet

- Aaconapps2 00-C91pb2aDocument21 pagesAaconapps2 00-C91pb2aJane DizonNo ratings yet

- Aaconapps2 00-C92pb2aDocument17 pagesAaconapps2 00-C92pb2aJane DizonNo ratings yet

- Auditing ProblemsDocument25 pagesAuditing ProblemsJane DizonNo ratings yet

- AP - A05 Audit of LiabilitiesDocument7 pagesAP - A05 Audit of LiabilitiesJane DizonNo ratings yet

- Aaconapps2 00-C91pb1aDocument17 pagesAaconapps2 00-C91pb1aJane DizonNo ratings yet

- Elements PR 1 2 3 4 5 6Document6 pagesElements PR 1 2 3 4 5 6Jane DizonNo ratings yet

- Solutions To Problems AFAR2 Chap3Document39 pagesSolutions To Problems AFAR2 Chap3Jane DizonNo ratings yet

- Aaconapps2 00-C92pb1aDocument14 pagesAaconapps2 00-C92pb1aJane DizonNo ratings yet

- Buscheto Di Giovanni: Cathedral Complex of PisaDocument3 pagesBuscheto Di Giovanni: Cathedral Complex of PisaJane DizonNo ratings yet

- What Do You SEE? What Details Stand Out?: (At This Stage, Elicit Observations, Not Interpretations.)Document2 pagesWhat Do You SEE? What Details Stand Out?: (At This Stage, Elicit Observations, Not Interpretations.)Jane DizonNo ratings yet

- 8 Buslawreg Foreign Week 14-15Document13 pages8 Buslawreg Foreign Week 14-15Jane DizonNo ratings yet

- Solutions To Problems AFAR2 Chapter 13Document18 pagesSolutions To Problems AFAR2 Chapter 13Jane DizonNo ratings yet

- Lesson 11 - If You Forget MeDocument7 pagesLesson 11 - If You Forget MeJane DizonNo ratings yet

- Yht Realty Corporation, Erlinda Lainez and Anicia Payam, Petitioners, vs. The Court of Appeals and Maurice Mcloughlin, RespondentsDocument1 pageYht Realty Corporation, Erlinda Lainez and Anicia Payam, Petitioners, vs. The Court of Appeals and Maurice Mcloughlin, RespondentsJane DizonNo ratings yet

- Technical Clarification Sheet For Valves PaintingDocument6 pagesTechnical Clarification Sheet For Valves Paintingnishant singhNo ratings yet

- Chyna's Dreamland Chase SeptDocument5 pagesChyna's Dreamland Chase SeptJonathan Seagull Livingston100% (1)

- Esami Consultant Strategic Tables For WorkingsDocument52 pagesEsami Consultant Strategic Tables For WorkingsPatrick MaulidiNo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Unit 2: Supply, Demand, and Consumer Choice: Do You See The Cow?Document26 pagesUnit 2: Supply, Demand, and Consumer Choice: Do You See The Cow?ARINNo ratings yet

- Green Design: An Introduction To Issues and Challenges: Werner JDocument6 pagesGreen Design: An Introduction To Issues and Challenges: Werner Jjulio perezNo ratings yet

- Zig Ziglars Secrets of Closing The Sale PDFDocument10 pagesZig Ziglars Secrets of Closing The Sale PDFhuguesNo ratings yet

- Program Conducted by Institute Related To IPR, Entrepreneurship / Start-Ups & InnovationDocument26 pagesProgram Conducted by Institute Related To IPR, Entrepreneurship / Start-Ups & InnovationDaisy Arora KhuranaNo ratings yet

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Operations Management in The Supply Chain Decisions and Cases Schroeder 6th Edition Test BankDocument15 pagesOperations Management in The Supply Chain Decisions and Cases Schroeder 6th Edition Test BankBrent Theiler100% (35)

- Introduction To Strategic ManagementDocument16 pagesIntroduction To Strategic ManagementNelsie PinedaNo ratings yet

- Old Bazaar Kiosk Monthly Basis: Aeon Mall Kuching CentralDocument5 pagesOld Bazaar Kiosk Monthly Basis: Aeon Mall Kuching CentralM Florence IstemNo ratings yet

- Tindak Lanjut DiklatDocument15 pagesTindak Lanjut Diklatdian kNo ratings yet

- Group 6Document4 pagesGroup 6999660% (3)

- RPF Contract 2024 FormDocument9 pagesRPF Contract 2024 Formmatimaintenance.npci2024No ratings yet

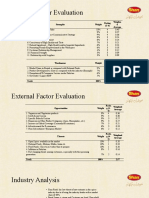

- Internal Factor Evaluation: Strengths Weight Rating (3-4) Weighte D AverageDocument3 pagesInternal Factor Evaluation: Strengths Weight Rating (3-4) Weighte D AverageHira NazNo ratings yet

- Tle - Afaacp9-12Pebc-Iiia-E Perform Estimation: Erickson S. AmandyDocument18 pagesTle - Afaacp9-12Pebc-Iiia-E Perform Estimation: Erickson S. AmandyErickson Saban Amandy100% (1)

- Lesson 3 Cost Volume Profit AnalysisDocument7 pagesLesson 3 Cost Volume Profit AnalysisklipordNo ratings yet

- French Telecom Group Altice Is On A PrecipiceDocument2 pagesFrench Telecom Group Altice Is On A PrecipiceRazvan TeleanuNo ratings yet

- Factors Affecting IHRMDocument2 pagesFactors Affecting IHRMSamish ChoudharyNo ratings yet

- Affidavit PACDocument3 pagesAffidavit PACadm developersNo ratings yet

- DM Salas Fiscal Admin 9Document2 pagesDM Salas Fiscal Admin 9Jomar's Place SalasNo ratings yet

- Hopfloor: Mandate Trade UnionDocument36 pagesHopfloor: Mandate Trade UnionGugutza DoiNo ratings yet

- Engl 6Document2 pagesEngl 6JJ JaumNo ratings yet

- Chapter 3Document19 pagesChapter 3Shan P FamularNo ratings yet

- UNIT-II-Problems On Capital BudgetingDocument2 pagesUNIT-II-Problems On Capital BudgetingGlyding FlyerNo ratings yet

- What Is ChangeDocument3 pagesWhat Is ChangeCalonneFrNo ratings yet

- Kasus BorealisDocument3 pagesKasus BorealisChairiah UlfahNo ratings yet

- JomPAY GuideDocument6 pagesJomPAY GuideSai Arein KiruvanantharNo ratings yet