You might also like

- Financial Statement Analysis: Business Strategy & Competitive AdvantageFrom EverandFinancial Statement Analysis: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Harsh Vardhan - Project Submission - Change ManagementDocument14 pagesHarsh Vardhan - Project Submission - Change ManagementHarsh Vardhan33% (3)

- RFBT ExamsDocument42 pagesRFBT ExamsJoyce LunaNo ratings yet

- Financial Statement Analysis and Ratio CalculationsDocument33 pagesFinancial Statement Analysis and Ratio CalculationsKamrul HasanNo ratings yet

- Sri Lanka Ceramic Sector Ratio AnalysisDocument16 pagesSri Lanka Ceramic Sector Ratio Analysischinthaka gayan40% (5)

- Ratio Analysis - HeroDocument25 pagesRatio Analysis - HeroGOURAV SHRIVASTAVA Student, Jaipuria IndoreNo ratings yet

- What Is Venture Capital?Document9 pagesWhat Is Venture Capital?Stephane LabrosseNo ratings yet

- Fin420 Ratio FinanceDocument27 pagesFin420 Ratio FinanceHulababoo KeChikNo ratings yet

- P9 RevDocument540 pagesP9 Revayyanar7100% (1)

- SS 620Document20 pagesSS 620jennalyn miraflor100% (1)

- HKTVmall Proposal - S001 ProposalDocument37 pagesHKTVmall Proposal - S001 Proposalas7No ratings yet

- Dabur Financial Ratio AnalysisDocument16 pagesDabur Financial Ratio AnalysisLakshmi Srinivasan100% (1)

- Accounts PPT 12Document16 pagesAccounts PPT 12Sudhanshu PurandareNo ratings yet

- RatioanalyasisDocument20 pagesRatioanalyasiscknowledge10No ratings yet

- Financial RatiosDocument8 pagesFinancial Ratios21AD01 - ABISHEK JNo ratings yet

- Analyze Company Performance with Financial RatiosDocument5 pagesAnalyze Company Performance with Financial RatiosAvinash SinhaNo ratings yet

- TCS Introduction: Key Facts and Financial AnalysisDocument11 pagesTCS Introduction: Key Facts and Financial AnalysispriyaNo ratings yet

- Financial Management (1) (8818)Document22 pagesFinancial Management (1) (8818)georgeNo ratings yet

- Cherry 1896 EditedDocument13 pagesCherry 1896 EditedsanalNo ratings yet

- Tata Motors Overview: Sales, Market Share, FinancialsDocument6 pagesTata Motors Overview: Sales, Market Share, FinancialsGaryNo ratings yet

- RuchikaDocument21 pagesRuchikaRajneesh Chandra BhattNo ratings yet

- Triple-A Office Mart Ratio AnalysisDocument8 pagesTriple-A Office Mart Ratio Analysissahil karmaliNo ratings yet

- Topic 1Document18 pagesTopic 1Nivaashene SaravananNo ratings yet

- Financial Statement Analysis of Exide Batteries LtdDocument14 pagesFinancial Statement Analysis of Exide Batteries LtdSHUBHAM PAWARNo ratings yet

- Financial Reporting ProjectDocument11 pagesFinancial Reporting Projecttech& GamingNo ratings yet

- Profitability Analysis of A Non Banking Financial Institution of BangladeshDocument27 pagesProfitability Analysis of A Non Banking Financial Institution of Bangladeshnusrat islamNo ratings yet

- Accounting Prenciple: AssignmentDocument19 pagesAccounting Prenciple: AssignmentIbrahim Khailil 1915216660No ratings yet

- Individual Assignment - Ratio AnalysisDocument9 pagesIndividual Assignment - Ratio Analysisyash rathodNo ratings yet

- An Analysis of The Financial Statement of Godrej India LTDDocument8 pagesAn Analysis of The Financial Statement of Godrej India LTDSachit MalikNo ratings yet

- 905pm - 10.EPRA JOURNALS 13145Document3 pages905pm - 10.EPRA JOURNALS 13145Mohammed YASEENNo ratings yet

- Financial Management Ratio Analysis Chapter3Document33 pagesFinancial Management Ratio Analysis Chapter3Bir kişiNo ratings yet

- Financial Statements Ratio Analysis of InfosysDocument15 pagesFinancial Statements Ratio Analysis of InfosysVishal KushwahaNo ratings yet

- Accounts Ail Activity: Nam E: Yas Hvi Rana Class: Xii-C Roll No.:34Document19 pagesAccounts Ail Activity: Nam E: Yas Hvi Rana Class: Xii-C Roll No.:341464Yashvi RanaNo ratings yet

- Marico: Current Ratio: This Ratio Explains The Relationship Between The Current Assets and The CurrentDocument4 pagesMarico: Current Ratio: This Ratio Explains The Relationship Between The Current Assets and The CurrentkpilNo ratings yet

- Ratio Analysis of Silva PharmaceuticalsDocument10 pagesRatio Analysis of Silva PharmaceuticalsShamim IqbalNo ratings yet

- Financial Analysis Serves The Following Purposes: 1. Measuring The ProfitabilityDocument7 pagesFinancial Analysis Serves The Following Purposes: 1. Measuring The ProfitabilityMariya TomsNo ratings yet

- Name: Hammad Ali (180811) Class: BSAF 4A Submitted To: Sir Khalid Subject: Financial Reporting 2Document14 pagesName: Hammad Ali (180811) Class: BSAF 4A Submitted To: Sir Khalid Subject: Financial Reporting 2tech& GamingNo ratings yet

- Bus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationDocument5 pagesBus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationCharles IrikefeNo ratings yet

- Analysis of Financial Statements 1-10-19Document28 pagesAnalysis of Financial Statements 1-10-19Shehzad QureshiNo ratings yet

- Template FM ProjectDocument32 pagesTemplate FM Projectsana shahidNo ratings yet

- Introduction of Ratio Analysis:-: MeaningDocument11 pagesIntroduction of Ratio Analysis:-: MeaningShawn RodriguezNo ratings yet

- Financial Analysis Report of Raymond FinalDocument14 pagesFinancial Analysis Report of Raymond FinalAnkit prakashNo ratings yet

- Financial Ratio Analysis Infosys PresentationDocument44 pagesFinancial Ratio Analysis Infosys PresentationSushanth VarmaNo ratings yet

- Financial Statement Analysis - Pantaloon Retail IndiaDocument7 pagesFinancial Statement Analysis - Pantaloon Retail IndiaSupriyaThengdiNo ratings yet

- Ratio Analysis of Coca-ColaDocument11 pagesRatio Analysis of Coca-ColaAshutosh SrivastavaNo ratings yet

- Attock Petroleum Limited: By: Iteqa Hameed Sidra NadeemDocument27 pagesAttock Petroleum Limited: By: Iteqa Hameed Sidra NadeemIbtisam RaiNo ratings yet

- Samsung Financial Ratios AnalysisDocument9 pagesSamsung Financial Ratios AnalysisRidho RakhmanNo ratings yet

- Leading Saudi Dairy Company SADAFCO's History, Operations and Financial AnalysisDocument6 pagesLeading Saudi Dairy Company SADAFCO's History, Operations and Financial AnalysisQusai BassamNo ratings yet

- Other Analysis Techniques NotesDocument23 pagesOther Analysis Techniques Noteskgaseitsiwe0952No ratings yet

- FS Services PDFDocument38 pagesFS Services PDFwajihu9618No ratings yet

- Unit 5 MANAGEMENT ACCOUNTINGDocument25 pagesUnit 5 MANAGEMENT ACCOUNTINGSANDFORD MALULUNo ratings yet

- Banking Handbook Ratios ExplainedDocument5 pagesBanking Handbook Ratios ExplainedSidharth Sankar RathNo ratings yet

- Financial Management - Mid Term MBADocument111 pagesFinancial Management - Mid Term MBAnaing sanNo ratings yet

- CF K C ChandanDocument10 pagesCF K C ChandanChandan K CNo ratings yet

- Ratio Analysis - Montex PensDocument28 pagesRatio Analysis - Montex Penss_sannit2k9No ratings yet

- Bba 1Document23 pagesBba 1SittaraNo ratings yet

- FM 2Document22 pagesFM 2Kajal singhNo ratings yet

- Learning Activities: Activity 1: Financial & Ratio AnalysisDocument2 pagesLearning Activities: Activity 1: Financial & Ratio AnalysisTurno ConnieNo ratings yet

- Comparative Analysis of Prism Cement LTD With JK Cement LTDDocument57 pagesComparative Analysis of Prism Cement LTD With JK Cement LTDRajudimple100% (1)

- Financial Ratio Analysis Infosys PresentationDocument43 pagesFinancial Ratio Analysis Infosys PresentationSaurabh SharmaNo ratings yet

- Financial Management: Session - 2: Financial Statement AnalysisDocument22 pagesFinancial Management: Session - 2: Financial Statement AnalysisShantanu SinhaNo ratings yet

- FM.-Financial-analysis-bookDocument31 pagesFM.-Financial-analysis-bookahmedsoobi73No ratings yet

- Working Capital Management atDocument29 pagesWorking Capital Management atNavkesh GautamNo ratings yet

- WACDocument2 pagesWACabhi vermaNo ratings yet

- Calculate WACC for Asian Paints and Kansai NerolacDocument10 pagesCalculate WACC for Asian Paints and Kansai Nerolacabhi vermaNo ratings yet

- SWOT and 5 ForcesDocument5 pagesSWOT and 5 Forcesabhi vermaNo ratings yet

- Financial Analysis - HotstarDocument5 pagesFinancial Analysis - Hotstarabhi vermaNo ratings yet

- Financial Research and Analysis: Submitted ToDocument3 pagesFinancial Research and Analysis: Submitted TokartikNo ratings yet

- LMP South Cotabato Chapter Meeting MinutesDocument2 pagesLMP South Cotabato Chapter Meeting MinutesDilg SurallahNo ratings yet

- Strength: Cultural Dimension of IndiaDocument3 pagesStrength: Cultural Dimension of IndiaRashmi PahariNo ratings yet

- Business Implications of Sustainability Practices in Supply ChainsDocument25 pagesBusiness Implications of Sustainability Practices in Supply ChainsBizNo ratings yet

- Medina Foundation College: Sapang Dalaga, Misamis OccidentalDocument18 pagesMedina Foundation College: Sapang Dalaga, Misamis OccidentalDELPGENMAR FRAYNANo ratings yet

- UBO - Lecture 03 - Mechanistic and Organic Forms of Organisational StructureDocument24 pagesUBO - Lecture 03 - Mechanistic and Organic Forms of Organisational StructureSerena AboNo ratings yet

- Industrial Disputes ResolutionDocument9 pagesIndustrial Disputes ResolutionNitinNo ratings yet

- BuxlyDocument13 pagesBuxlyAimen KhatanaNo ratings yet

- Contract AgreementDocument4 pagesContract AgreementkhanNo ratings yet

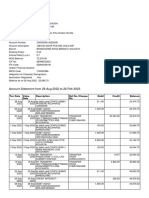

- Bank StatementDocument5 pagesBank StatementSANJIB GHOSHNo ratings yet

- Barclays Case Study.Document2 pagesBarclays Case Study.ReemaNo ratings yet

- MAS BackgroundDocument2 pagesMAS BackgroundJie FifieNo ratings yet

- Conceptual Framework and Accounting Standards OverviewDocument170 pagesConceptual Framework and Accounting Standards OverviewJ LagardeNo ratings yet

- Chap021newDocument36 pagesChap021newNguyễn Cẩm HươngNo ratings yet

- Q RV 57 W Vjed KW RRBM 2 ZCCDocument66 pagesQ RV 57 W Vjed KW RRBM 2 ZCCsaroj rajavariNo ratings yet

- Hypothesis-Driven DevelopmentDocument2 pagesHypothesis-Driven DevelopmentMuhammad El-FahamNo ratings yet

- Measuring HSE Awareness Using AHPDocument23 pagesMeasuring HSE Awareness Using AHPYounes OULMANENo ratings yet

- Sales Order FormDocument1 pageSales Order FormDeepthireddyNo ratings yet

- Final Propsal 3Document63 pagesFinal Propsal 3hinsene begna100% (1)

- Module 2: Assignment: PROBLEM 9 - Treasury SharesDocument8 pagesModule 2: Assignment: PROBLEM 9 - Treasury SharesYvonne DuyaoNo ratings yet

- Trends in Ethics in Computing Assignment # 05 Sap Ids of Group MembersDocument2 pagesTrends in Ethics in Computing Assignment # 05 Sap Ids of Group Memberswardah mukhtarNo ratings yet

- Property Assessed Clean EnerDocument41 pagesProperty Assessed Clean Enermd shoebNo ratings yet

- Nigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Document11 pagesNigeria, Ghana, Kenya, Egypt and South Africa - Software Engineer (1 - 5)Ajiboye JosephNo ratings yet

- Power Fill Business PrimerDocument20 pagesPower Fill Business Primerskynyrd75No ratings yet

- Job Application Letter Internal Vacancy SampleDocument8 pagesJob Application Letter Internal Vacancy Sampleafdlxeqbk100% (1)

- Mkm05 ReviewerDocument8 pagesMkm05 ReviewerSamantha PaceosNo ratings yet