You might also like

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Performance Review Template (Self, Manager, Peers)Document10 pagesPerformance Review Template (Self, Manager, Peers)Marko IllustrisimoNo ratings yet

- Retail MathDocument7 pagesRetail MathApaar Arora50% (2)

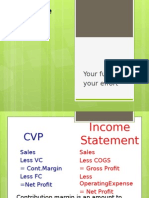

- CVP NotesDocument7 pagesCVP NotesKerrice RobinsonNo ratings yet

- BEP N CVP AnalysisDocument49 pagesBEP N CVP AnalysisJamaeca Ann MalsiNo ratings yet

- Business Mathematics Module 6.1 Margin and Mark UpDocument15 pagesBusiness Mathematics Module 6.1 Margin and Mark UpDavid DueNo ratings yet

- Acid-Test Ratio: Average InventoryDocument8 pagesAcid-Test Ratio: Average InventorymohsinnaveesNo ratings yet

- Retail Math Made Simple Pres.Document37 pagesRetail Math Made Simple Pres.Odiris N Odiris N100% (2)

- Buying and SellingDocument36 pagesBuying and SellingJocelyn D. Descartin LptNo ratings yet

- Definition of Break Even Point:: ExampleDocument4 pagesDefinition of Break Even Point:: ExampleAnonymous mzF3JvyTJsNo ratings yet

- CAP760 - Hazard & RiskDocument88 pagesCAP760 - Hazard & Riskngmo34No ratings yet

- Break Even Point AnalysisDocument11 pagesBreak Even Point AnalysisRose Munyasia100% (2)

- Retail Buying Math PracticeDocument25 pagesRetail Buying Math PracticeAndrea VargasNo ratings yet

- Retail Costing-F&tDocument31 pagesRetail Costing-F&tKaushal YadavNo ratings yet

- Determine ending inventory using retail methodDocument9 pagesDetermine ending inventory using retail methodfreshneuroNo ratings yet

- Retail FormulasDocument5 pagesRetail FormulasAnil Kumar KashyapNo ratings yet

- MG FNSACC517 Provide Management Accounting InformationDocument11 pagesMG FNSACC517 Provide Management Accounting InformationGurpreet KaurNo ratings yet

- Calculate profit margins and understand markupDocument23 pagesCalculate profit margins and understand markupNikhil SurveNo ratings yet

- 93% Score on Managerial Accounting QuizDocument6 pages93% Score on Managerial Accounting Quizgelsk50% (2)

- Audit Process PDFDocument30 pagesAudit Process PDFŘõmęõ Ji100% (2)

- Activate Project ManagerDocument13 pagesActivate Project ManagerSurya Yadav100% (4)

- Agile Software DevelopmentDocument6 pagesAgile Software DevelopmentPavan KumarNo ratings yet

- Case Study - Management Control - Texas Instruments and Hewlett - PackardDocument20 pagesCase Study - Management Control - Texas Instruments and Hewlett - PackardJed Estanislao80% (10)

- Supply Chain Manager ResponsibilitiesDocument8 pagesSupply Chain Manager ResponsibilitiesvbadsNo ratings yet

- TQM Class NotesDocument12 pagesTQM Class NotesMOHAMMED ALI CHOWDHURY100% (4)

- Markup As A Merchandising ToolDocument45 pagesMarkup As A Merchandising Toolapi-3705996100% (2)

- MarkdownsDocument28 pagesMarkdownsapi-3705996100% (3)

- Mark Up Mark DownDocument22 pagesMark Up Mark DownAnonymous rWn3ZVARLgNo ratings yet

- Mark Up and Mark DownDocument7 pagesMark Up and Mark DownPankaj100% (1)

- Topic: Buying and Selling Learning TargetsDocument7 pagesTopic: Buying and Selling Learning TargetsJohniel MartinNo ratings yet

- Differentiate Mark-Up From MarginsDocument20 pagesDifferentiate Mark-Up From MarginsAndrea GalangNo ratings yet

- Cost Volume Profit (CVP) Analysis and Break Even Point AnalysisDocument22 pagesCost Volume Profit (CVP) Analysis and Break Even Point Analysisimelda100% (1)

- ResearchDocument2 pagesResearchallendrosaliseNo ratings yet

- Final Exam BMGT 350Document16 pagesFinal Exam BMGT 350johnnyscansNo ratings yet

- Retail PricingDocument16 pagesRetail PricingRony MathewNo ratings yet

- Definition of Break Even PointDocument4 pagesDefinition of Break Even PointNishant RaoNo ratings yet

- Pricing Strategies and CalculationsDocument17 pagesPricing Strategies and Calculationsagus joharudinNo ratings yet

- Factors Considered in Pricing Policies and Markup StrategiesDocument9 pagesFactors Considered in Pricing Policies and Markup StrategiesXandra LeeNo ratings yet

- Retail Pricing Strategies and Markup ConceptsDocument45 pagesRetail Pricing Strategies and Markup ConceptsAnkit KumarNo ratings yet

- END3972 Week4 v2Document20 pagesEND3972 Week4 v2Enes TürksalNo ratings yet

- Ecommerce - MetriceDocument3 pagesEcommerce - MetriceGrigore Silviu AlexandruNo ratings yet

- Buying and SellingDocument6 pagesBuying and SellingEnrique RiñosNo ratings yet

- Markup, Markdown, Inventory ManagementDocument42 pagesMarkup, Markdown, Inventory ManagementhaslizanurNo ratings yet

- Business Mathematics Module 5 Mark on Mark Up and MarkdownDocument4 pagesBusiness Mathematics Module 5 Mark on Mark Up and Markdowngabezarate071No ratings yet

- Lec 19 MARGIN AND MARKUP NUMERICALSDocument3 pagesLec 19 MARGIN AND MARKUP NUMERICALShaiqa malikNo ratings yet

- Definition of Break Even Point:: ExampleDocument4 pagesDefinition of Break Even Point:: ExampleAnonymous mzF3JvyTJsNo ratings yet

- 03-04-2012Document62 pages03-04-2012Adeel AliNo ratings yet

- Calculating Maintained Markup PercentageDocument4 pagesCalculating Maintained Markup PercentageAmisha SinghNo ratings yet

- Chapter 9 Cost Volume Profit AnalysisDocument47 pagesChapter 9 Cost Volume Profit AnalysisAtif Saeed100% (2)

- Sample Case BriefDocument4 pagesSample Case Briefacoustic7850% (2)

- 2 CVP Analysis Final PDFDocument44 pages2 CVP Analysis Final PDFmoss roffattNo ratings yet

- Generate Profits with CVP Graphs and Target SalesDocument6 pagesGenerate Profits with CVP Graphs and Target SalesAlawi Maliha TribhuNo ratings yet

- CVP New + LastDocument19 pagesCVP New + LastDawit AmahaNo ratings yet

- Cost-Volume-Profit (CVP) Analysis: Understanding Break-Even Point, Margin of Safety and Operating LeverageDocument40 pagesCost-Volume-Profit (CVP) Analysis: Understanding Break-Even Point, Margin of Safety and Operating LeverageJeejohn Sodusta0% (1)

- Reviewer Cvp-Strategic Cost-MowenDocument10 pagesReviewer Cvp-Strategic Cost-MowenSaeym SegoviaNo ratings yet

- Financial Aspects of Marketing ManagementDocument10 pagesFinancial Aspects of Marketing ManagementMohd ImtiazNo ratings yet

- Buying and SellingDocument21 pagesBuying and SellingJannette RamosNo ratings yet

- Example Margin of SafetyDocument3 pagesExample Margin of SafetyNeenaNo ratings yet

- Financial Aspects of Marketing Management: by Subbu Sivaramakrishnan University of ManitobaDocument36 pagesFinancial Aspects of Marketing Management: by Subbu Sivaramakrishnan University of ManitobaChunnuriNo ratings yet

- E-Portfolio Assignment By: Sean Bindra 100170563Document30 pagesE-Portfolio Assignment By: Sean Bindra 100170563seanbindraNo ratings yet

- Chapter-One Cost-Volume-Profit (CVP) Analysis: 1.1 Variable and Fixed Cost Behavior and PatternDocument43 pagesChapter-One Cost-Volume-Profit (CVP) Analysis: 1.1 Variable and Fixed Cost Behavior and PatternHayelom Tadesse GebreNo ratings yet

- 3.2 PM Target Costing 260622Document18 pages3.2 PM Target Costing 260622abhijit tikekarNo ratings yet

- Buying and SellingDocument19 pagesBuying and SellingNeri SangalangNo ratings yet

- Chapter 3Document35 pagesChapter 3Chaltu DabiNo ratings yet

- Cost Behavior and Cost-Volume RelationshipsDocument97 pagesCost Behavior and Cost-Volume RelationshipsUtsav DubeyNo ratings yet

- 12b.standard Costing XDocument18 pages12b.standard Costing XAbhinav AshishNo ratings yet

- Costing Methods for Apparel ProductsDocument14 pagesCosting Methods for Apparel ProductsAbhinav AshishNo ratings yet

- Types of Costing: Export MerchandisingDocument11 pagesTypes of Costing: Export MerchandisingAbhinav AshishNo ratings yet

- 12c .Standard Costs & Variance-AnalysisDocument33 pages12c .Standard Costs & Variance-AnalysisAbhinav AshishNo ratings yet

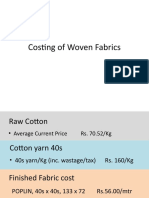

- 14-15 Costing of Woven FabricsDocument9 pages14-15 Costing of Woven FabricsAbhinav AshishNo ratings yet

- 1.intruduction To Cost AccountingDocument13 pages1.intruduction To Cost AccountingAbhinav AshishNo ratings yet

- 10c.retail PricingDocument10 pages10c.retail PricingAbhinav AshishNo ratings yet

- All English Editorial 16.07.2022Document37 pagesAll English Editorial 16.07.2022Abhinav AshishNo ratings yet

- Semester VI Management Control System Flexible BudgetDocument5 pagesSemester VI Management Control System Flexible BudgetbhavyaNo ratings yet

- The Impact of Warehouse Relocation On The Supply Chain DepartmentDocument16 pagesThe Impact of Warehouse Relocation On The Supply Chain DepartmentInternational Journal of Business Marketing and ManagementNo ratings yet

- What Is CompetencyDocument3 pagesWhat Is Competencysureshdwivedi2482No ratings yet

- Economics g7-9Document3 pagesEconomics g7-9Dea MeilitaNo ratings yet

- Advanced Accounting Multiple Choice ProblemsDocument15 pagesAdvanced Accounting Multiple Choice ProblemsKryscel ManansalaNo ratings yet

- Supply Chain Management Scenario in India: Prof. Gagandeep A HosmaniDocument5 pagesSupply Chain Management Scenario in India: Prof. Gagandeep A HosmaniRavi SatyapalNo ratings yet

- Developing An Incentive Scheme For A ProjectDocument14 pagesDeveloping An Incentive Scheme For A ProjectMansoor KhanaliNo ratings yet

- Laura Ann Rauen ResumeDocument3 pagesLaura Ann Rauen ResumeLauraNo ratings yet

- Internal auditing multiple choice questionsDocument4 pagesInternal auditing multiple choice questionsSantos Gigantoca Jr.No ratings yet

- Training Program English Alphabet PronunciationDocument3 pagesTraining Program English Alphabet PronunciationClavijo LordsDannyNo ratings yet

- SCM NissanDocument11 pagesSCM NissangodsonzachariahNo ratings yet

- CISM Application FRM Eng 1115Document10 pagesCISM Application FRM Eng 1115dhanoj6522No ratings yet

- Chap 10Document45 pagesChap 10Sawan AcharyNo ratings yet

- StrategyDocument2 pagesStrategyChandan BharambeNo ratings yet

- Chapter 1Document49 pagesChapter 1Guntur Pramana Edy PutraNo ratings yet

- Measuring Supply Chain Performance Using Financial DataDocument6 pagesMeasuring Supply Chain Performance Using Financial DatatalithaNo ratings yet

- 10Document20 pages10Mohammed LubNo ratings yet

- Formal Planning ProcessDocument10 pagesFormal Planning Processislam elnassagNo ratings yet

- Sombrero Case AnalysisDocument2 pagesSombrero Case AnalysisManaswini SharmaNo ratings yet

- Tổng hợp câu hỏi trắc nghiệm Logistics - Tiếng AnhDocument11 pagesTổng hợp câu hỏi trắc nghiệm Logistics - Tiếng AnhKim TuyếnNo ratings yet

- Fuction of HSE Committee PDFDocument6 pagesFuction of HSE Committee PDFYan FerizalNo ratings yet