You might also like

- Interest Rate Models Lecture Note SummaryDocument87 pagesInterest Rate Models Lecture Note Summaryben tenNo ratings yet

- Lecture Note 02 - Bond Valuation and Yield MeasuresDocument75 pagesLecture Note 02 - Bond Valuation and Yield Measuresben tenNo ratings yet

- Lecture Note 07 - Fixed Income Options and Credit DerivativesDocument64 pagesLecture Note 07 - Fixed Income Options and Credit Derivativesben tenNo ratings yet

- Forward and Futures ContractsDocument55 pagesForward and Futures Contractsben tenNo ratings yet

- Lecture Note 03 - Bond Price VolatilityDocument53 pagesLecture Note 03 - Bond Price Volatilityben tenNo ratings yet

- Lecture Note 04 - Bond Yield and Interest Rate StructureDocument54 pagesLecture Note 04 - Bond Yield and Interest Rate Structureben tenNo ratings yet

- Introduction to Fixed Income Securities LectureDocument45 pagesIntroduction to Fixed Income Securities Lectureben tenNo ratings yet

- ISLAMIC FINANCE ASSIGNMENTDocument10 pagesISLAMIC FINANCE ASSIGNMENTAina SaffiyahNo ratings yet

- The Stochastic Growth Model: Download Free Books atDocument32 pagesThe Stochastic Growth Model: Download Free Books atZaky MuhammadNo ratings yet

- VontDocument128 pagesVontch tcNo ratings yet

- We WorkDocument18 pagesWe WorkCarinda AdistiaraNo ratings yet

- GS Modeling S - P 500 Returns Using Investment Flows and Liquidity DataDocument12 pagesGS Modeling S - P 500 Returns Using Investment Flows and Liquidity DatawangyhNo ratings yet

- V2 Exam 2 PM PDFDocument30 pagesV2 Exam 2 PM PDFMaharishi VaidyaNo ratings yet

- 2.2 - Swaps - NotesDocument10 pages2.2 - Swaps - NotesTGCNo ratings yet

- Kotak International REIT FOF PresentationDocument32 pagesKotak International REIT FOF PresentationRohan RautelaNo ratings yet

- Capital Market - Thematic Report - 28 Nov 22Document123 pagesCapital Market - Thematic Report - 28 Nov 22bharat.divineNo ratings yet

- S L I A L: Ecuritization of IFE Nsurance Ssets AND IabilitiesDocument34 pagesS L I A L: Ecuritization of IFE Nsurance Ssets AND IabilitiesTejaswiniNo ratings yet

- UntitledDocument52 pagesUntitledYEN YEN CHONGNo ratings yet

- Measuring Corporate PerformanceDocument39 pagesMeasuring Corporate PerformanceAbdullah BugshanNo ratings yet

- Moody's Certificate in Commercail CreditDocument8 pagesMoody's Certificate in Commercail CreditExplore with TejuNo ratings yet

- Lecture Note 10 - Mortgage and Mortgage-Backed SecuritiesDocument58 pagesLecture Note 10 - Mortgage and Mortgage-Backed Securitiesben tenNo ratings yet

- Invest Aug 2022 ReportDocument733 pagesInvest Aug 2022 Reportthe kingfishNo ratings yet

- J2 Retail Markets in AsiaDocument17 pagesJ2 Retail Markets in AsiaKhusen NizomiddinovNo ratings yet

- MBA 8 Year 2 Managerial Finance January 2020Document269 pagesMBA 8 Year 2 Managerial Finance January 2020weedforlifeNo ratings yet

- Bootstrapping Business 1. DefinitionDocument5 pagesBootstrapping Business 1. DefinitionÁnh NguyệtNo ratings yet

- Introduction to Money and Financial SystemsDocument9 pagesIntroduction to Money and Financial SystemsRABICCA FAISALNo ratings yet

- Wealthcon India Issue 7 Highlights Financial TopicsDocument112 pagesWealthcon India Issue 7 Highlights Financial TopicsAmol WaghmareNo ratings yet

- Dividend QuestionDocument43 pagesDividend QuestionRehaan ShahNo ratings yet

- Risk Management and ALMDocument93 pagesRisk Management and ALMThe Cultural CommitteeNo ratings yet

- Ethiopia, 6.625% 11dec2024, USDDocument1 pageEthiopia, 6.625% 11dec2024, USDLloyd Ki'sNo ratings yet

- Farmers Bank foreign exchange operationsDocument77 pagesFarmers Bank foreign exchange operationsMrinal Kanti DasNo ratings yet

- Commodity Trade FinanceDocument19 pagesCommodity Trade FinanceRichard LiaoNo ratings yet

- Crest Slb&Repo SettlementsDocument41 pagesCrest Slb&Repo SettlementsGroucho32No ratings yet

- Investment Decision RulesDocument62 pagesInvestment Decision RulesMarcos EspindolaNo ratings yet

- SEFAM AJMC-RatiosDocument26 pagesSEFAM AJMC-RatiosShanzeh WaheedNo ratings yet

- Risk Management and Financial Institutions: by John C. HullDocument31 pagesRisk Management and Financial Institutions: by John C. HullValentina MariNo ratings yet

- Accenture Capital Markets Vision 2022Document36 pagesAccenture Capital Markets Vision 2022manugeorgeNo ratings yet

- Excellent Present at On On Financial Management of Structured ProductsDocument18 pagesExcellent Present at On On Financial Management of Structured ProductsForeclosure Fraud100% (1)

- 363 Sales-Goodwin ProcterDocument4 pages363 Sales-Goodwin ProctergbsneddonNo ratings yet

- 15 Stocks Oct15th2018Document4 pages15 Stocks Oct15th2018ShanmugamNo ratings yet

- 2.CFA一级基础段另类 Tom 打印版Document30 pages2.CFA一级基础段另类 Tom 打印版Evelyn YangNo ratings yet

- R22 Capital Structue IFT NotesDocument11 pagesR22 Capital Structue IFT NotesAdnan MasoodNo ratings yet

- Financial Management Group AssignmentDocument30 pagesFinancial Management Group Assignmenteyob yohannesNo ratings yet

- Private Equity Firms, Funds, and Transactions AnalyzedDocument47 pagesPrivate Equity Firms, Funds, and Transactions AnalyzedLeonardo SimonciniNo ratings yet

- Kuliah Ke-5 #Cost of CapitalDocument45 pagesKuliah Ke-5 #Cost of CapitalHASNA PUTRINo ratings yet

- MVAA 2021 Annual Report: Lean On UsDocument20 pagesMVAA 2021 Annual Report: Lean On UsDevon Louise KesslerNo ratings yet

- Primer in B2B Brand-Building Strategies With A Reader PracticumDocument10 pagesPrimer in B2B Brand-Building Strategies With A Reader PracticumkhanNo ratings yet

- Blume Investment Report 16 Q3 2015 PDFDocument3 pagesBlume Investment Report 16 Q3 2015 PDFAbcd123411No ratings yet

- RBC - ARCC - Initiation - Research at A Glance - 17 PagesDocument17 pagesRBC - ARCC - Initiation - Research at A Glance - 17 PagesSagar PatelNo ratings yet

- 4 P'S of Marketing Mix: Ms. Padge Sanjana SunilDocument51 pages4 P'S of Marketing Mix: Ms. Padge Sanjana SunilShraddha MokalNo ratings yet

- FR17 - Employee Benefits (Stud) .Document45 pagesFR17 - Employee Benefits (Stud) .duong duongNo ratings yet

- Chapter - I: PageDocument56 pagesChapter - I: PageJanani ShanmugamNo ratings yet

- Majestic opportunity in the US$9.25bn P&C insurance software marketDocument25 pagesMajestic opportunity in the US$9.25bn P&C insurance software marketJatin SoniNo ratings yet

- Capital Planning 2Document87 pagesCapital Planning 2kudasanyahNo ratings yet

- QF ProjectDocument27 pagesQF Projectmhod omranNo ratings yet

- Assignment - Chapter 5 (Due 10.11.20)Document4 pagesAssignment - Chapter 5 (Due 10.11.20)Tenaj KramNo ratings yet

- Buy Now, Pay Later: Market Trends and Consumer Impacts: Consumer Financial Protection Bureau - September 2022Document83 pagesBuy Now, Pay Later: Market Trends and Consumer Impacts: Consumer Financial Protection Bureau - September 2022Mohamed AdelNo ratings yet

- Moodys HF GovernanceDocument8 pagesMoodys HF GovernanceGennady NeymanNo ratings yet

- 8 FullDocument13 pages8 FullAnh TranNo ratings yet

- Finance - Bond StrategiesDocument26 pagesFinance - Bond StrategiesBarkha SharmaNo ratings yet

- Introduction to Fixed Income Securities LectureDocument45 pagesIntroduction to Fixed Income Securities Lectureben tenNo ratings yet

- Lecture Note 05 - Bonds With Other FeaturesDocument62 pagesLecture Note 05 - Bonds With Other Featuresben tenNo ratings yet

- Lecture Note 04 - Bond Yield and Interest Rate StructureDocument54 pagesLecture Note 04 - Bond Yield and Interest Rate Structureben tenNo ratings yet

- Buddhism in Central Asia LectureDocument27 pagesBuddhism in Central Asia Lectureben tenNo ratings yet

- Introduction To Buddhism 7Document15 pagesIntroduction To Buddhism 7ben tenNo ratings yet

- Introduction To Buddhism 10Document12 pagesIntroduction To Buddhism 10ben tenNo ratings yet

- BSTC 2003 Dr. Tony Chui Centre of Buddhist Studies Tonychui@hku - HKDocument62 pagesBSTC 2003 Dr. Tony Chui Centre of Buddhist Studies Tonychui@hku - HKben tenNo ratings yet

- Introduction To Buddhism 9Document17 pagesIntroduction To Buddhism 9ben tenNo ratings yet

- Lecture Note 10 - Mortgage and Mortgage-Backed SecuritiesDocument58 pagesLecture Note 10 - Mortgage and Mortgage-Backed Securitiesben tenNo ratings yet

- Japoool)Document1 pageJapoool)ben tenNo ratings yet

- CH 02Document69 pagesCH 02ben tenNo ratings yet

- BSTC2003 Lecture 3Document73 pagesBSTC2003 Lecture 3ben tenNo ratings yet

- VaR Analysis of Single Asset Market RiskDocument59 pagesVaR Analysis of Single Asset Market Riskben tenNo ratings yet

- c60311384247263795d41dafcc64ec54Document1 pagec60311384247263795d41dafcc64ec54ben tenNo ratings yet

- STAT4608 Market Risk Analysis: Tutorial 2 Normality and EMHDocument11 pagesSTAT4608 Market Risk Analysis: Tutorial 2 Normality and EMHben tenNo ratings yet

- 053907602f7e10872707a6440eda4cf6Document2 pages053907602f7e10872707a6440eda4cf6ben tenNo ratings yet

- Unlve: T I L eDocument1 pageUnlve: T I L eben tenNo ratings yet

- 60af499605d8c480e1f095f0b03a661aDocument2 pages60af499605d8c480e1f095f0b03a661aben tenNo ratings yet

- Acct Statement - XX6419 - 08112022Document26 pagesAcct Statement - XX6419 - 08112022AartiNo ratings yet

- Rule 1: Survival is the Only Road to RichesDocument4 pagesRule 1: Survival is the Only Road to RichesManish GargNo ratings yet

- Cash-and-Cash-Equivalents-PCF-Bank-Recon-and-Proof-of-Cash ReviewerDocument10 pagesCash-and-Cash-Equivalents-PCF-Bank-Recon-and-Proof-of-Cash ReviewerNelson AbaigarNo ratings yet

- Islamic Credit Card Fees Guide: Annual, Replacement, Late Payment & MoreDocument4 pagesIslamic Credit Card Fees Guide: Annual, Replacement, Late Payment & Moreengg.aliNo ratings yet

- BaaccenDocument4 pagesBaaccenshylabaguio15No ratings yet

- ADD QuestionDocument8 pagesADD Questionomkolhe0007No ratings yet

- Mission 200Document80 pagesMission 200HITESH PurohitNo ratings yet

- Biniyam Yitbarek Article Review On Financial AnalysisDocument6 pagesBiniyam Yitbarek Article Review On Financial AnalysisBiniyam Yitbarek100% (1)

- Fin358 Chapter 3Document4 pagesFin358 Chapter 3syaiera aqilahNo ratings yet

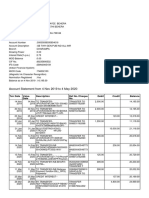

- Account Statement From 4 Nov 2019 To 4 May 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 4 Nov 2019 To 4 May 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChiranjibi Behera ChiruNo ratings yet

- Direct Access Non-Continuous UDC Consolidated BillDocument5 pagesDirect Access Non-Continuous UDC Consolidated BillAmina chahalNo ratings yet

- FM II Assignment 6 W22Document1 pageFM II Assignment 6 W22Farah ImamiNo ratings yet

- AP BUILDING PHONE BILL Oct 23Document1 pageAP BUILDING PHONE BILL Oct 23jfallon1969No ratings yet

- Amortization and Sinking FundDocument27 pagesAmortization and Sinking FundKelvin BarceLonNo ratings yet

- Sensitivity AnalysisDocument5 pagesSensitivity AnalysisMohsin QayyumNo ratings yet

- Applied EconomicsDocument3 pagesApplied EconomicsDel RosarioNo ratings yet

- SBI Annual Report 10 11Document58 pagesSBI Annual Report 10 11AayushmaanDhirNo ratings yet

- Tugas Akm Ii Pertemuan 13Document5 pagesTugas Akm Ii Pertemuan 13Alisya UmariNo ratings yet

- Intro to financial accounting: Double-entry bookkeepingDocument2 pagesIntro to financial accounting: Double-entry bookkeepingKhaled Abo YousefNo ratings yet

- Partnership Formation and Firm AmalgamationDocument22 pagesPartnership Formation and Firm AmalgamationShridhar Kaligotla75% (4)

- Green REIT PLC Annual Report 2016Document176 pagesGreen REIT PLC Annual Report 2016Mihir JoshiNo ratings yet

- BRI Monthly Oct 2022Document5 pagesBRI Monthly Oct 2022Andri MirzalNo ratings yet

- Fin 202 S1 2016Document29 pagesFin 202 S1 2016herueuxNo ratings yet

- Solved Nick S Enterprises Has Purchased A New Machine Tool That WillDocument1 pageSolved Nick S Enterprises Has Purchased A New Machine Tool That WillAnbu jaromiaNo ratings yet

- Sapm - 2 MarksDocument17 pagesSapm - 2 MarksA Senthilkumar100% (3)

- Calculating RAROC For The Corporate Accounts in Bank of BarodaDocument20 pagesCalculating RAROC For The Corporate Accounts in Bank of Barodajagjeetkumar178% (9)

- IUJ Math Aptitude Test - Sample 4Document7 pagesIUJ Math Aptitude Test - Sample 4Tigist TayeNo ratings yet

- Green Finance: Actors, Challenges and Policy RecommendationsDocument4 pagesGreen Finance: Actors, Challenges and Policy RecommendationschinkiNo ratings yet

- Forecasting: Prospective Analysis: ALK Week 10Document18 pagesForecasting: Prospective Analysis: ALK Week 10Rayhan AlfansaNo ratings yet

- Syllabus Money and Capital Markets - EditDocument18 pagesSyllabus Money and Capital Markets - EditẢo Tung ChảoNo ratings yet