You might also like

- Audit Example Questionnaire 2017Document26 pagesAudit Example Questionnaire 2017Grace UnayNo ratings yet

- 2016 Audit Management Letter Final PDFDocument21 pages2016 Audit Management Letter Final PDFMeriah NainggolanNo ratings yet

- Returned Checks Audit Work ProgramDocument4 pagesReturned Checks Audit Work ProgramozlemNo ratings yet

- Aaa Study GuideDocument507 pagesAaa Study GuideTiến Thành Nguyễn100% (2)

- Ap Audit DocumentDocument7 pagesAp Audit DocumentAnna Tran100% (1)

- 2017 Model Internal Audit Activity Charter PDFDocument9 pages2017 Model Internal Audit Activity Charter PDFChristen CastilloNo ratings yet

- IIA Code of EthicsDocument3 pagesIIA Code of EthicsachistepNo ratings yet

- Internal Audit StrategyDocument5 pagesInternal Audit StrategyRoberto Vega100% (1)

- Whole Audit NoteDocument34 pagesWhole Audit NoteBijoy SalahuddinNo ratings yet

- PWC Revenue From Contracts With CustomersDocument16 pagesPWC Revenue From Contracts With CustomersJobelyn CasimNo ratings yet

- ELC - Control Environment QuestionnaireDocument3 pagesELC - Control Environment QuestionnaireMeanne Waga SalazarNo ratings yet

- ICQ MatrixDocument8 pagesICQ Matrixapi-3828505No ratings yet

- Audit Strategy for Liverpool City RegionDocument36 pagesAudit Strategy for Liverpool City RegionNajihah Che MatNo ratings yet

- Audit Manual For CMA FirmsDocument123 pagesAudit Manual For CMA FirmsSajid Ali100% (1)

- 171018overview On Internal AuditDocument23 pages171018overview On Internal AuditMourad HACHCHADNo ratings yet

- Global Internal Audit StandardsDocument120 pagesGlobal Internal Audit StandardsMarcos Wilker100% (3)

- Audit PlaningDocument14 pagesAudit PlaningFarraNo ratings yet

- Corporate Treasury Review - Audit ReportDocument18 pagesCorporate Treasury Review - Audit ReportirfanNo ratings yet

- ASU 2201E IP02.SolutionDocument10 pagesASU 2201E IP02.SolutionIuliia Gondarchyna100% (2)

- Commissions Audit Work ProgramDocument15 pagesCommissions Audit Work ProgramJoseph Takunda ChidemboNo ratings yet

- IA ManualDocument76 pagesIA ManualMalav PatelNo ratings yet

- INTERNAL AUDIT Strategic ManagamentDocument8 pagesINTERNAL AUDIT Strategic ManagamentAhtisham Alam GujjarNo ratings yet

- PWC Account ReconDocument8 pagesPWC Account ReconAcca Fia TuitionNo ratings yet

- 14 05 Sa 896a App A Audit Planning Board ReportDocument19 pages14 05 Sa 896a App A Audit Planning Board ReportRikky AdiwijayaNo ratings yet

- Auditing Standards MCQ TestDocument7 pagesAuditing Standards MCQ TestKevin James Sedurifa Oledan100% (1)

- Audit PlanDocument23 pagesAudit PlanUzma AbedinNo ratings yet

- Audit FlashcardDocument12 pagesAudit Flashcardvarghese2007100% (1)

- IIA Principals and StandardsDocument43 pagesIIA Principals and StandardsLeslie FernandezNo ratings yet

- Iia Ig - Standard 1300 Quality Assurance and Improvement ProgramDocument5 pagesIia Ig - Standard 1300 Quality Assurance and Improvement ProgramArtoToroNo ratings yet

- PWC Colonial Liability Order 122817Document92 pagesPWC Colonial Liability Order 122817Daniel Fisher100% (1)

- Audit Risk Register TemplateDocument3 pagesAudit Risk Register TemplateMAHESH SHAW100% (1)

- KPMG Interim Audit Report 201516Document14 pagesKPMG Interim Audit Report 201516Gideon Hilarde100% (1)

- Audit Flashcards for Chapter 6 on Internal ControlsDocument42 pagesAudit Flashcards for Chapter 6 on Internal ControlsdissidentmeNo ratings yet

- Engagement Letter XXXXXXDocument2 pagesEngagement Letter XXXXXXDaryl OtsukaNo ratings yet

- ISA 315 & ISA 240 (Fraud and Risk)Document54 pagesISA 315 & ISA 240 (Fraud and Risk)Joe SmithNo ratings yet

- Information Technology General Controls LeafletDocument2 pagesInformation Technology General Controls LeafletgamallofNo ratings yet

- 2013 Audit Management LetterDocument2 pages2013 Audit Management LetterWKYC.com100% (1)

- Internal Audit Tapestry EY ACLN InSights Apr11Document16 pagesInternal Audit Tapestry EY ACLN InSights Apr11Veena HingarhNo ratings yet

- Project Auditing of A Insurance CompanyDocument42 pagesProject Auditing of A Insurance CompanyJayesh Shirodkar50% (2)

- Financial Audit Manual Vol.02Document360 pagesFinancial Audit Manual Vol.02aqua01100% (1)

- External Auditors' Reliance On Internal Audit in Sri LankaDocument83 pagesExternal Auditors' Reliance On Internal Audit in Sri Lankadilu_0002100% (2)

- Audit Engagement FileDocument19 pagesAudit Engagement FileMujtaba HussainiNo ratings yet

- Print Version Lead Auditor ModuleDocument90 pagesPrint Version Lead Auditor Modulekevinmathew27No ratings yet

- 3 Audit PlanningDocument16 pages3 Audit PlanningHussain MustunNo ratings yet

- ISA Audit Guide 2010-01Document243 pagesISA Audit Guide 2010-01Victor JacintoNo ratings yet

- Summary Book Auditing A Practical Approach Chapter 1 3Document37 pagesSummary Book Auditing A Practical Approach Chapter 1 3AB100% (1)

- Risk and ControlDocument33 pagesRisk and ControlKashaf SegarNo ratings yet

- Plan The Audit - Pre-EngagementDocument26 pagesPlan The Audit - Pre-EngagementDiana GustianaNo ratings yet

- Re SA B42 AUD Final PB Exam Questions Answers Solutions Re SA B42 AUD Final PB Exam Questions Answers SolutionsDocument26 pagesRe SA B42 AUD Final PB Exam Questions Answers Solutions Re SA B42 AUD Final PB Exam Questions Answers SolutionsNamnam KimNo ratings yet

- Working Papers - Top Tips PDFDocument3 pagesWorking Papers - Top Tips PDFYus Ceballos100% (1)

- PG Assessing Organizational Governance in The Public SectorDocument36 pagesPG Assessing Organizational Governance in The Public SectorRobertoNo ratings yet

- Sample of Internal Audit Manual TemplateDocument51 pagesSample of Internal Audit Manual TemplateOlayinka OnimeNo ratings yet

- Assessment of Audit RiskDocument9 pagesAssessment of Audit RiskAli KhanNo ratings yet

- ACCA AAA Paper - Advanced Audit and Assurance Lecture NotesDocument83 pagesACCA AAA Paper - Advanced Audit and Assurance Lecture NotesIddy Mohamed100% (4)

- Internal Auditing-Adding Value Across The BoardDocument7 pagesInternal Auditing-Adding Value Across The BoardSherlyAgustinNo ratings yet

- Entity-Level Controls Fraud Questionnaire AssessmentDocument8 pagesEntity-Level Controls Fraud Questionnaire AssessmentKirby C. LoberizaNo ratings yet

- ISQC-1 Implementation GuideDocument107 pagesISQC-1 Implementation GuideCreanga Georgian100% (1)

- 78 Cosmetics GMP Audit ChecklistDocument3 pages78 Cosmetics GMP Audit Checklistsandeshkuperkar95No ratings yet

- Audit 2 l7 Audit and Business RiskDocument43 pagesAudit 2 l7 Audit and Business RiskGen AbulkhairNo ratings yet

- Audit Calendar Global Site 2018Document14 pagesAudit Calendar Global Site 2018IshikaNo ratings yet

- CHAP 8. Audit Planning and Analytical ProceduresDocument24 pagesCHAP 8. Audit Planning and Analytical ProceduresNoroNo ratings yet

- Auditing ManualTC7Document264 pagesAuditing ManualTC7Alinafe SteshaNo ratings yet

- Commercial Audit ManualDocument404 pagesCommercial Audit ManualMohit SharmaNo ratings yet

- Audit Committee Charter 02.12.2018 PDFDocument9 pagesAudit Committee Charter 02.12.2018 PDFMaribelVelascoVillaverdeNo ratings yet

- Chief Audit Executive Job DescriptionDocument3 pagesChief Audit Executive Job DescriptionozlemNo ratings yet

- Audit Cash Investments TitleDocument7 pagesAudit Cash Investments TitleIulia BurtoiuNo ratings yet

- Audit Questionnaire June 2013Document21 pagesAudit Questionnaire June 2013erine5995No ratings yet

- FAM Points - Ch9Document37 pagesFAM Points - Ch9ALISA ASIFNo ratings yet

- Digital Supply Chain Management An OverviewDocument7 pagesDigital Supply Chain Management An OverviewAdeel AhmadNo ratings yet

- 08 - Process TechnologiesDocument20 pages08 - Process TechnologiesSyed ArslanNo ratings yet

- Internalauditreportwriting 150526070325 Lva1 App6892Document18 pagesInternalauditreportwriting 150526070325 Lva1 App6892Adeel AhmadNo ratings yet

- McDonald's Business Plan in PakistanDocument41 pagesMcDonald's Business Plan in PakistanAdeel AhmadNo ratings yet

- Audit Evidence New SlidesDocument20 pagesAudit Evidence New SlidesAdeel AhmadNo ratings yet

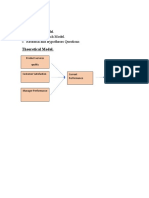

- Steps:: Theoretical Model. Business Research Model. Research and Hypotheses QuestionsDocument7 pagesSteps:: Theoretical Model. Business Research Model. Research and Hypotheses QuestionsAdeel AhmadNo ratings yet

- The Central Evaluation Unit: Case StudyDocument2 pagesThe Central Evaluation Unit: Case StudyAdeel AhmadNo ratings yet

- Process Design - Graded Assignment 1BDocument2 pagesProcess Design - Graded Assignment 1BAdeel AhmadNo ratings yet

- 4.employee Motivation ProjectDocument53 pages4.employee Motivation ProjectAdeel AhmadNo ratings yet

- Metro Cash and Carry Brand Equity Model Analyzes Customer Loyalty & TouchpointsDocument5 pagesMetro Cash and Carry Brand Equity Model Analyzes Customer Loyalty & TouchpointsAdeel AhmadNo ratings yet

- Foundation of Decision MakingDocument34 pagesFoundation of Decision MakingAdeel AhmadNo ratings yet

- English Assignment Cover Page 3Document1 pageEnglish Assignment Cover Page 3Adeel AhmadNo ratings yet

- Section: A Assignment: 1 Principles of Management: Name: Roll No: Section: ProgramDocument5 pagesSection: A Assignment: 1 Principles of Management: Name: Roll No: Section: ProgramAdeel AhmadNo ratings yet

- Name: Adeel Ahmad Roll Numb: BBHM-F19-033 Class: BBA (2A) Submitted To: Mam ShaziaDocument12 pagesName: Adeel Ahmad Roll Numb: BBHM-F19-033 Class: BBA (2A) Submitted To: Mam ShaziaAdeel AhmadNo ratings yet

- What Is A Stakeholder?: Adeel Ahmad BBHM-F19-033Document4 pagesWhat Is A Stakeholder?: Adeel Ahmad BBHM-F19-033Adeel AhmadNo ratings yet

- Business Statistics ProjectDocument4 pagesBusiness Statistics ProjectAdeel AhmadNo ratings yet

- Creative and persuasive writing techniques explored in book reviewsDocument3 pagesCreative and persuasive writing techniques explored in book reviewsAdeel AhmadNo ratings yet

- Identifying Sentence Types in AssignmentsDocument4 pagesIdentifying Sentence Types in AssignmentsAdeel AhmadNo ratings yet

- Brand Audit Report: Final Project Bba MarketingDocument21 pagesBrand Audit Report: Final Project Bba MarketingshamzanNo ratings yet

- Brand Equity Model of Metro: Great Place To Get All The Little Things You NeedDocument5 pagesBrand Equity Model of Metro: Great Place To Get All The Little Things You NeedAdeel AhmadNo ratings yet

- Family Tree Template 15Document1 pageFamily Tree Template 15Adeel AhmadNo ratings yet

- Brand ManagementDocument27 pagesBrand ManagementAdeel AhmadNo ratings yet

- Organization CommunicationDocument27 pagesOrganization CommunicationAdeel AhmadNo ratings yet

- BM PyramidDocument1 pageBM PyramidAdeel AhmadNo ratings yet

- Major Approaches of ManagementDocument30 pagesMajor Approaches of ManagementAdeel AhmadNo ratings yet

- Application of Estimation and Point Estimation in BiostatisticsDocument10 pagesApplication of Estimation and Point Estimation in BiostatisticsAdeel AhmadNo ratings yet

- 4.employee Motivation ProjectDocument53 pages4.employee Motivation ProjectAdeel AhmadNo ratings yet

- Haier A.C Supply Chain Management Mid ProjectDocument12 pagesHaier A.C Supply Chain Management Mid ProjectAdeel AhmadNo ratings yet

- What Is The Legislation Process ?Document2 pagesWhat Is The Legislation Process ?Adeel AhmadNo ratings yet

- Basic Auditing ConceptxxxDocument8 pagesBasic Auditing ConceptxxxMerlyn CaibiganNo ratings yet

- AC17&18:ASSURANCE Principles, Profes Sional Ethics and Good GovernanceDocument36 pagesAC17&18:ASSURANCE Principles, Profes Sional Ethics and Good GovernancecmaeNo ratings yet

- Auditor's Report on Financial StatementsDocument9 pagesAuditor's Report on Financial StatementsEm-em ValNo ratings yet

- Chartered Accountant Gautam Bhutani Personal StatementDocument3 pagesChartered Accountant Gautam Bhutani Personal StatementVed Prakash JaggaNo ratings yet

- Auditing and Assurance PrinciplesDocument4 pagesAuditing and Assurance PrinciplesKarla AlconisNo ratings yet

- Case 2Document2 pagesCase 2api-284102912No ratings yet

- Financial Reporting and Audit Evidence: by Mwamba Ally Jingu: Fcpa PHDDocument20 pagesFinancial Reporting and Audit Evidence: by Mwamba Ally Jingu: Fcpa PHDAdil KhamisNo ratings yet

- Chapter 3 The Internal Audit Function An IntegralDocument24 pagesChapter 3 The Internal Audit Function An IntegralPengkuh Ardi NugrahaNo ratings yet

- Test Bank Chapter 6 - Falak Jan EnayatDocument23 pagesTest Bank Chapter 6 - Falak Jan EnayatFalak EnayatNo ratings yet

- Auditing 2Document47 pagesAuditing 2Sonu Harris GeorgeNo ratings yet

- PPT 01Document36 pagesPPT 01Diaz Hesron Deo SimorangkirNo ratings yet

- Assignment AuditDocument20 pagesAssignment AuditLuqmanul HakimNo ratings yet

- Performing Substantive TestDocument8 pagesPerforming Substantive TestKei TamundongNo ratings yet

- Proficiency Test: I. Part I. Listening Comprehension. (20 Points)Document12 pagesProficiency Test: I. Part I. Listening Comprehension. (20 Points)Rafael FernandezNo ratings yet

- Auditing and Its Objective in NepalDocument10 pagesAuditing and Its Objective in NepalNyimaSherpaNo ratings yet

- Jurnal Akuntansi, Keuangan, Dan Manajemen (Jakman) : Martini@budiluhur - Ac.idDocument14 pagesJurnal Akuntansi, Keuangan, Dan Manajemen (Jakman) : Martini@budiluhur - Ac.idsarah ahmadNo ratings yet

- Chapter 6 Audit Responsibilities and ObjectivesDocument22 pagesChapter 6 Audit Responsibilities and ObjectivesJenne LeeNo ratings yet

- Auditing in A Computer Information Systems (Cis) EnvironmentDocument15 pagesAuditing in A Computer Information Systems (Cis) EnvironmentWinnieNo ratings yet

- (8533) Assignment#01Document15 pages(8533) Assignment#01noorislamkhanNo ratings yet

- Chapter 7 - Accepting The Engagement and Planning The AuditDocument9 pagesChapter 7 - Accepting The Engagement and Planning The Auditsimona_xoNo ratings yet

- PT Paramita Bangun Sarana 2017 Financial ReportDocument71 pagesPT Paramita Bangun Sarana 2017 Financial ReportsitimudaNo ratings yet