You might also like

- Internal Audit - Report Writing PDFDocument27 pagesInternal Audit - Report Writing PDFabhishek_simNo ratings yet

- Internal AuditingDocument19 pagesInternal AuditingOwen GarciaNo ratings yet

- Item 7 - Appendix A 9Document17 pagesItem 7 - Appendix A 9AMIT_AGRAHARI111987100% (1)

- ReportDocument24 pagesReportRamachandra_CNo ratings yet

- Review Questions - Chapter 9 Internal AuditDocument7 pagesReview Questions - Chapter 9 Internal AudithaleedaNo ratings yet

- Tips On Writing Internal Audit ReportsDocument5 pagesTips On Writing Internal Audit ReportsSohail Iftikhar100% (1)

- Audit Report: 1.what Is The Importance of An Audit ReportDocument68 pagesAudit Report: 1.what Is The Importance of An Audit ReportMd Maruf KhanNo ratings yet

- Step 5 Auditing-Report-Writing-ToolkitDocument19 pagesStep 5 Auditing-Report-Writing-ToolkitRhea SimoneNo ratings yet

- Purpose of AuditDocument5 pagesPurpose of Auditannisa radiNo ratings yet

- Report Writin1Document9 pagesReport Writin1Bhatt PawanNo ratings yet

- Resume Purpose and Type Internal Audit ReportDocument4 pagesResume Purpose and Type Internal Audit ReportAnnisa Rahman DhitaNo ratings yet

- Technical Report Writing (Cosc4161) : Chapter Two-Types of ReportsDocument22 pagesTechnical Report Writing (Cosc4161) : Chapter Two-Types of ReportsTamene TekileNo ratings yet

- Training Session On Report WritingDocument28 pagesTraining Session On Report WritingAjaya SahooNo ratings yet

- PG Audit ReportsDocument45 pagesPG Audit ReportsWubneh Alemu100% (2)

- Module 2 in Technical WritingDocument19 pagesModule 2 in Technical WritingSitty NurhafsahNo ratings yet

- AI-X-S10-G3-Raviano Althaf RasyidavaDocument6 pagesAI-X-S10-G3-Raviano Althaf Rasyidavaraviano rasyidavaNo ratings yet

- The Audit Process How We Work With You2Document17 pagesThe Audit Process How We Work With You2Rich R. PontesorNo ratings yet

- How To Write An Audit ReportDocument7 pagesHow To Write An Audit Reportmulabbi brianNo ratings yet

- ACT 3202 Â - PRINCIPLES OF AUDITING Letter of WeaknessDocument16 pagesACT 3202 Â - PRINCIPLES OF AUDITING Letter of WeaknessJasmin BasimNo ratings yet

- 2019 Report WritingDocument9 pages2019 Report WritingRajaram PandaNo ratings yet

- Chapter 11 070804Document8 pagesChapter 11 070804Shahid Nasir MalikNo ratings yet

- Completing AuditDocument20 pagesCompleting AuditmeseleNo ratings yet

- BW Report WritingDocument47 pagesBW Report WritingErickNo ratings yet

- Auditor's Report (AutoRecovered)Document12 pagesAuditor's Report (AutoRecovered)Lovenia M. FerrerNo ratings yet

- Fish Bone DiagramDocument4 pagesFish Bone DiagramPatrice Elaine PillaNo ratings yet

- Flashcards CIA Part 2Document270 pagesFlashcards CIA Part 2daniel geevarghese100% (1)

- Types of Technical ReportsDocument35 pagesTypes of Technical ReportsMs. Joy100% (1)

- Anagement Etter: N UditingDocument11 pagesAnagement Etter: N UditingShafqat BukhariNo ratings yet

- The Audit Observations Update DashboardDocument8 pagesThe Audit Observations Update Dashboardkinz7879No ratings yet

- Audit StrategyDocument5 pagesAudit StrategyPhil SatiaNo ratings yet

- Audit Process: Here Click HereDocument3 pagesAudit Process: Here Click HereShailesh Gosai100% (1)

- Reporting Standards in Government Auditing: ISSAI 400Document6 pagesReporting Standards in Government Auditing: ISSAI 400Ilyes MathlouthiNo ratings yet

- Audit SaadDocument29 pagesAudit SaadsabeehahsanNo ratings yet

- Informational ReportsDocument16 pagesInformational ReportsIlham fairuz MasriNo ratings yet

- Echo Seminar On Report Writing - Day 1Document96 pagesEcho Seminar On Report Writing - Day 1Rona SilvestreNo ratings yet

- Business and Technical Report WritingDocument45 pagesBusiness and Technical Report WritingHumptySharma100% (2)

- Module 2Document11 pagesModule 2Ruthika Sv789No ratings yet

- Mc.5 TH Unit II BBaDocument29 pagesMc.5 TH Unit II BBaABINAYANo ratings yet

- Audit ch-6Document36 pagesAudit ch-6fekadegebretsadik478729No ratings yet

- Chapter 17 ReportsDocument42 pagesChapter 17 ReportsArizal Zul LathiifNo ratings yet

- Chapter 6-Audit ReportDocument14 pagesChapter 6-Audit ReportDawit WorkuNo ratings yet

- External AuditDocument26 pagesExternal Auditjuju1992No ratings yet

- Audit Reports Communicating Assurance enDocument45 pagesAudit Reports Communicating Assurance encyrosemt100% (1)

- Report Writing: Unit IIIDocument25 pagesReport Writing: Unit IIIAmishaNo ratings yet

- Auditing and Internal Control IT Auditing, Hall, 4eDocument32 pagesAuditing and Internal Control IT Auditing, Hall, 4eMarco LamNo ratings yet

- The Internal Audit Process From A To ZDocument5 pagesThe Internal Audit Process From A To Zinnovativies100% (1)

- Report Writing: Meaning and DefinitionDocument24 pagesReport Writing: Meaning and DefinitionSandeep SinghNo ratings yet

- Auditing and Corporate GovernanceDocument7 pagesAuditing and Corporate GovernanceMuskan TyagiNo ratings yet

- Chapter - 5Document11 pagesChapter - 5dejen mengstieNo ratings yet

- Literature Review Internal AuditDocument7 pagesLiterature Review Internal Auditea59a2k5100% (1)

- Internal Audit, Management and Operational AuditDocument14 pagesInternal Audit, Management and Operational AuditNeetu gargNo ratings yet

- Lesson 4Document34 pagesLesson 4Ramon AlpitcheNo ratings yet

- Audit ReportDocument5 pagesAudit ReportMaheswari Ramesh100% (1)

- The Art in Writing Effective Internal Audit ReportsDocument26 pagesThe Art in Writing Effective Internal Audit ReportsMasoom Larka100% (1)

- Chapter 6 - Audit ReportDocument10 pagesChapter 6 - Audit ReportsteveiamidNo ratings yet

- Internal Audit ReportingDocument39 pagesInternal Audit ReportingShaleenPatni100% (3)

- Auditing Principles and Practice I Chapter 6Document28 pagesAuditing Principles and Practice I Chapter 6demsashu21No ratings yet

- Audit I - Chapter 6, Audit Report TDocument30 pagesAudit I - Chapter 6, Audit Report TKalkayeNo ratings yet

- Chapter 2 Aud 2015 DUDocument12 pagesChapter 2 Aud 2015 DUMoti BekeleNo ratings yet

- 08 - Process TechnologiesDocument20 pages08 - Process TechnologiesSyed ArslanNo ratings yet

- Process Design - Graded Assignment 1BDocument2 pagesProcess Design - Graded Assignment 1BAdeel AhmadNo ratings yet

- 4.employee Motivation ProjectDocument53 pages4.employee Motivation ProjectAdeel AhmadNo ratings yet

- The Central Evaluation Unit: Case StudyDocument2 pagesThe Central Evaluation Unit: Case StudyAdeel AhmadNo ratings yet

- Digital Supply Chain Management An OverviewDocument7 pagesDigital Supply Chain Management An OverviewAdeel AhmadNo ratings yet

- Audit Evidence New SlidesDocument20 pagesAudit Evidence New SlidesAdeel AhmadNo ratings yet

- IF Final AssignmentDocument41 pagesIF Final AssignmentAdeel AhmadNo ratings yet

- Audit Planning and Risk Assessment New SlidesDocument38 pagesAudit Planning and Risk Assessment New SlidesAdeel AhmadNo ratings yet

- Foundation of Decision MakingDocument34 pagesFoundation of Decision MakingAdeel AhmadNo ratings yet

- Section: A Assignment: 1 Principles of Management: Name: Roll No: Section: ProgramDocument5 pagesSection: A Assignment: 1 Principles of Management: Name: Roll No: Section: ProgramAdeel AhmadNo ratings yet

- Steps:: Theoretical Model. Business Research Model. Research and Hypotheses QuestionsDocument7 pagesSteps:: Theoretical Model. Business Research Model. Research and Hypotheses QuestionsAdeel AhmadNo ratings yet

- CBBEDocument5 pagesCBBEAdeel AhmadNo ratings yet

- English Assignment Cover Page 3Document1 pageEnglish Assignment Cover Page 3Adeel AhmadNo ratings yet

- Business Statistics ProjectDocument4 pagesBusiness Statistics ProjectAdeel AhmadNo ratings yet

- Name: Adeel Ahmad Roll Numb: BBHM-F19-033 Class: BBA (2A) Submitted To: Mam ShaziaDocument12 pagesName: Adeel Ahmad Roll Numb: BBHM-F19-033 Class: BBA (2A) Submitted To: Mam ShaziaAdeel AhmadNo ratings yet

- What Is A Stakeholder?: Adeel Ahmad BBHM-F19-033Document4 pagesWhat Is A Stakeholder?: Adeel Ahmad BBHM-F19-033Adeel AhmadNo ratings yet

- Family Tree Template 15Document1 pageFamily Tree Template 15Adeel AhmadNo ratings yet

- Brand Equity Model of Metro: Great Place To Get All The Little Things You NeedDocument5 pagesBrand Equity Model of Metro: Great Place To Get All The Little Things You NeedAdeel AhmadNo ratings yet

- Zain EnglishDocument4 pagesZain EnglishAdeel AhmadNo ratings yet

- Brand Audit Report: Final Project Bba MarketingDocument21 pagesBrand Audit Report: Final Project Bba MarketingshamzanNo ratings yet

- Creative and Persuasive Writing: Name: Adeel Ahmad Roll No: BBHM-F19-033 Class: BBA Section: 2ADocument3 pagesCreative and Persuasive Writing: Name: Adeel Ahmad Roll No: BBHM-F19-033 Class: BBA Section: 2AAdeel AhmadNo ratings yet

- Brand AudtingDocument27 pagesBrand AudtingAdeel AhmadNo ratings yet

- BM PyramidDocument1 pageBM PyramidAdeel AhmadNo ratings yet

- History of ManagementDocument30 pagesHistory of ManagementAdeel AhmadNo ratings yet

- What Is The Legislation Process ?Document2 pagesWhat Is The Legislation Process ?Adeel AhmadNo ratings yet

- 4.employee Motivation ProjectDocument53 pages4.employee Motivation ProjectAdeel AhmadNo ratings yet

- Organization CommunicationDocument27 pagesOrganization CommunicationAdeel AhmadNo ratings yet

- Application of Estimation and Point Estimation in BiostatisticsDocument10 pagesApplication of Estimation and Point Estimation in BiostatisticsAdeel AhmadNo ratings yet

- Haier A.C Supply Chain Management Mid ProjectDocument12 pagesHaier A.C Supply Chain Management Mid ProjectAdeel AhmadNo ratings yet

- Financial Statement AnalysisDocument2 pagesFinancial Statement AnalysisVivek SuranaNo ratings yet

- Colorado Community College System Accounting Procedures Manual (SAP)Document40 pagesColorado Community College System Accounting Procedures Manual (SAP)Rakesh DawarNo ratings yet

- Jaguar Land Rover LimitedDocument59 pagesJaguar Land Rover Limitedharsh shahNo ratings yet

- DV and ORSDocument7 pagesDV and ORSAddy GuinalNo ratings yet

- Des 213Document105 pagesDes 213Pastor-Oshatoba Femi JedidiahNo ratings yet

- Gul Ahmed Textile Mills Ltd. Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisDocument13 pagesGul Ahmed Textile Mills Ltd. Fundamental Company Report Including Financial, SWOT, Competitors and Industry AnalysisMuzamil HussainNo ratings yet

- Practical Accounting 1Document3 pagesPractical Accounting 1Angelo Otañes GasatanNo ratings yet

- Quality Control Plan (For Study) PDFDocument10 pagesQuality Control Plan (For Study) PDFRobin GuNo ratings yet

- Chapter 24Document3 pagesChapter 24Trường Nguyễn CôngNo ratings yet

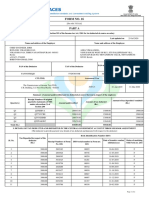

- Afrpv2859q 2020-21 PDFDocument2 pagesAfrpv2859q 2020-21 PDFnidhisasidharanNo ratings yet

- Chapter04 Noting Drafting and Office ProcedureDocument14 pagesChapter04 Noting Drafting and Office ProcedureIggy BopNo ratings yet

- Central Bank of The Philippines v. Citytrust Banking Corporation, G.R. No. 141835Document1 pageCentral Bank of The Philippines v. Citytrust Banking Corporation, G.R. No. 141835xxxaaxxxNo ratings yet

- L - ISO27k - Process - Diag - With - PDCA - 780Document1 pageL - ISO27k - Process - Diag - With - PDCA - 780velibor27No ratings yet

- Financial Management of A NPODocument13 pagesFinancial Management of A NPOLex McGuireNo ratings yet

- Topic 1: Assumptions of CVP AnalysisDocument8 pagesTopic 1: Assumptions of CVP AnalysisZaib NawazNo ratings yet

- IG1230 Continuing Professional DevelopmentDocument4 pagesIG1230 Continuing Professional DevelopmentgdegirolamoNo ratings yet

- Chapter 5 Quality ManagementDocument19 pagesChapter 5 Quality Managementkevin digumberNo ratings yet

- Auditing Canadian 7th Edition Smieliauskas Test Bank DownloadDocument16 pagesAuditing Canadian 7th Edition Smieliauskas Test Bank DownloadMargaret Narcisse100% (21)

- ISO 9001 Product Data SheetDocument2 pagesISO 9001 Product Data SheetAbu KanshaNo ratings yet

- Dela Cruz V COADocument9 pagesDela Cruz V COAgelatin528No ratings yet

- Bangko Sentral NG Pilipinas vs. Commission On Audit 2017Document10 pagesBangko Sentral NG Pilipinas vs. Commission On Audit 2017Mhelle Bhlue YslawNo ratings yet

- Inc Tax Chapter 2Document27 pagesInc Tax Chapter 2Noeme LansangNo ratings yet

- BSP Circular No. 706Document8 pagesBSP Circular No. 706Unis BautistaNo ratings yet

- CFA Magazine July Aug 2013Document60 pagesCFA Magazine July Aug 2013patrickmemeNo ratings yet

- 1 Jul 2015-Master Circular On Customer Service - UCBs PDFDocument56 pages1 Jul 2015-Master Circular On Customer Service - UCBs PDFDisability Rights AllianceNo ratings yet

- LT1 Assurance IntroductionDocument9 pagesLT1 Assurance IntroductionAbs PangaderNo ratings yet

- What Is A Chart of AccountsDocument2 pagesWhat Is A Chart of AccountsJonhmark AniñonNo ratings yet

- How Audit Departments Can Develop An Effective AML Program Thomas AlessandroDocument13 pagesHow Audit Departments Can Develop An Effective AML Program Thomas AlessandroGodsonNo ratings yet

- IFMIS CPA Andrew RoriDocument29 pagesIFMIS CPA Andrew Roriabey.mulugetaNo ratings yet

- Margaret Wilson Review of TDSBDocument34 pagesMargaret Wilson Review of TDSBCityNewsTorontoNo ratings yet