You might also like

- Quizzer - Financial Accounting ProcessDocument8 pagesQuizzer - Financial Accounting ProcessLuisitoNo ratings yet

- Journal Entries Ledger Trial Balance Problem and SolutionDocument7 pagesJournal Entries Ledger Trial Balance Problem and SolutionArgha DuttaNo ratings yet

- Entrepreneurship-1112 Q2 SLM WK7Document8 pagesEntrepreneurship-1112 Q2 SLM WK7April Jean Cahoy56% (9)

- Alyssa C. Del Pilar Bsa-1 Brfabm1 225Document28 pagesAlyssa C. Del Pilar Bsa-1 Brfabm1 225Ken Sann89% (9)

- Basic Accounting Reviewer Step 1 To 3Document12 pagesBasic Accounting Reviewer Step 1 To 3Mary Gleyne100% (1)

- INS2098 Chapter 1 NoteDocument6 pagesINS2098 Chapter 1 NoteVũ Hồng NgânNo ratings yet

- Bookkeeping Assignment JournalizingDocument1 pageBookkeeping Assignment JournalizingPhilpNil8000No ratings yet

- Problems Chapter 11 and 12Document8 pagesProblems Chapter 11 and 12u got no jamsNo ratings yet

- I 04.05studentDocument22 pagesI 04.05studentFaizan Yousuf67% (3)

- Ch02 Analyzing TransactionsDocument55 pagesCh02 Analyzing TransactionsejasignacionNo ratings yet

- BKP 9 Accounting EquationDocument16 pagesBKP 9 Accounting EquationPhilpNil8000No ratings yet

- Lesson 1 - Acctg+Document8 pagesLesson 1 - Acctg+CARLA JAYNE MAGMOYAONo ratings yet

- Assignment No. 1 (Financial Transactions) Answer KeyDocument9 pagesAssignment No. 1 (Financial Transactions) Answer KeyHeasylyn tadeoNo ratings yet

- Kuma's accounting transactions and trial balanceDocument4 pagesKuma's accounting transactions and trial balanceMarls PantinNo ratings yet

- Transaction & Tabular AnalysisDocument18 pagesTransaction & Tabular AnalysisMahmudul Hassan RohidNo ratings yet

- M3A Expanded Accounting EquationDocument20 pagesM3A Expanded Accounting EquationCharles Eli AlejandroNo ratings yet

- ACCO Module 2Document5 pagesACCO Module 2Lala BoraNo ratings yet

- Chapter Accounting EquationDocument24 pagesChapter Accounting Equationpriyam.200409No ratings yet

- Fundamantels of Accounting PresentationDocument24 pagesFundamantels of Accounting PresentationAmy TabaconNo ratings yet

- FRA Class ProblemsDocument4 pagesFRA Class Problemskaisarimam96No ratings yet

- Here are the answers:1. Total Assets = $1,044,5002. Total Liabilities = $237,900 3. Total Owner's Equity = $806,6004. Total Revenues = $350,0005. Total Expenses = $13,4006. Net Income = $336,600Document28 pagesHere are the answers:1. Total Assets = $1,044,5002. Total Liabilities = $237,900 3. Total Owner's Equity = $806,6004. Total Revenues = $350,0005. Total Expenses = $13,4006. Net Income = $336,600Dia Did L. RadNo ratings yet

- Name:John Michael Najarro Course&Year: BSBA 1 Date: 10/7/20: Colegio de Santa Rita de San Carlos, IncDocument3 pagesName:John Michael Najarro Course&Year: BSBA 1 Date: 10/7/20: Colegio de Santa Rita de San Carlos, IncRod Najarro100% (1)

- (ACCTG) Classifying&Recording TransactionsDocument3 pages(ACCTG) Classifying&Recording TransactionsMiranda, Aliana Jasmine M.No ratings yet

- L02 App of Acc Equation Wo ExerciseDocument7 pagesL02 App of Acc Equation Wo ExercisecalebNo ratings yet

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaNo ratings yet

- AE100-2 Accounting EquationDocument33 pagesAE100-2 Accounting EquationRoel Dagdag100% (2)

- FDNACCT Unit 4 - Part 1 - Analyzing Business Transactions - Class Ex - Answer KeyDocument1 pageFDNACCT Unit 4 - Part 1 - Analyzing Business Transactions - Class Ex - Answer Keyrabinoadrian24No ratings yet

- Analyzing Business TransactionsDocument21 pagesAnalyzing Business TransactionsDan Gideon Cariaga100% (1)

- The Accounting EquationDocument24 pagesThe Accounting EquationShaina CalingNo ratings yet

- Journalizing Transactions (Review) - 9.5.17Document13 pagesJournalizing Transactions (Review) - 9.5.17Jessa Beloy100% (1)

- Muftie Abu Zaiem Pranantya - 142200027 - AkuntansiPengantarDocument12 pagesMuftie Abu Zaiem Pranantya - 142200027 - AkuntansiPengantarMuftie Abu Zaiem PNo ratings yet

- Accounting EquationDocument8 pagesAccounting EquationIanah AlvaradoNo ratings yet

- Principles of accounting cycle and financial statementsDocument38 pagesPrinciples of accounting cycle and financial statementsSara Abdelrahim MakkawiNo ratings yet

- Fabm 1 ReviewDocument29 pagesFabm 1 ReviewMelanie Cruz ConventoNo ratings yet

- Module-1 SolutionsDocument6 pagesModule-1 SolutionsARYA GOWDANo ratings yet

- Accounting Non-Accountants Part 2Document37 pagesAccounting Non-Accountants Part 2Vanessa Gapas0% (1)

- Unit - 1 Accounting Equations & Journal & Ledger & TBDocument43 pagesUnit - 1 Accounting Equations & Journal & Ledger & TBShreyash PardeshiNo ratings yet

- An-Najah N. University Faculty of Eng. & IT (MIS Dept.) Final Assignment Principle of Accounting and Finance 17/5/2020 9 - 11 AmDocument4 pagesAn-Najah N. University Faculty of Eng. & IT (MIS Dept.) Final Assignment Principle of Accounting and Finance 17/5/2020 9 - 11 AmHiba ShalbeNo ratings yet

- Principles of Accounting Second Year, Semester 1: Transactions AnalysisDocument38 pagesPrinciples of Accounting Second Year, Semester 1: Transactions AnalysisSara Abdelrahim MakkawiNo ratings yet

- Answers To Act 1 3 Module 3 Account T Account and Part 1 Acctg CycleDocument11 pagesAnswers To Act 1 3 Module 3 Account T Account and Part 1 Acctg CycleRowena ReoloNo ratings yet

- Lesson 2 Accounting Elements Answer KeyDocument17 pagesLesson 2 Accounting Elements Answer KeyJoshua Arjay V. ToveraNo ratings yet

- Flores Computer Shop June Transactions and Financial StatementsDocument12 pagesFlores Computer Shop June Transactions and Financial StatementsGajulin, April JoyNo ratings yet

- Chapter 2 Practice KEYDocument17 pagesChapter 2 Practice KEYmartinmuebejayiNo ratings yet

- Worksheet 1 DR CRDocument5 pagesWorksheet 1 DR CRMc Clent CervantesNo ratings yet

- Chapter 2Document49 pagesChapter 2haiderasim1212No ratings yet

- AfM 0 - Introduction, Transaction Recognition, AccountsDocument30 pagesAfM 0 - Introduction, Transaction Recognition, AccountsjaymursalieNo ratings yet

- Accounting EquationDocument2 pagesAccounting EquationVaibhav GuptaNo ratings yet

- Fundamentals of Accountancy, Business and ManagementDocument84 pagesFundamentals of Accountancy, Business and ManagementgiselleNo ratings yet

- Session 2 Ma (9th May 2012)Document31 pagesSession 2 Ma (9th May 2012)KamauWafulaWanyamaNo ratings yet

- Chapter 1 Accounting in ActionDocument35 pagesChapter 1 Accounting in ActionRuslan AdibNo ratings yet

- Topic 6.Document5 pagesTopic 6.Ernie AbeNo ratings yet

- Fundamentals of Accounting, Business, and ManagementDocument35 pagesFundamentals of Accounting, Business, and ManagementKyla BallesterosNo ratings yet

- Accounting EquationfinalDocument40 pagesAccounting EquationfinalChowdhury Mobarrat Haider AdnanNo ratings yet

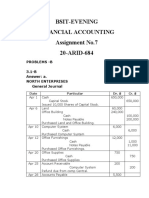

- BSIT-EVENING FINANCIAL ACCOUNTING Assignment No.7 20-ARID-684 PROBLEMS -BDocument7 pagesBSIT-EVENING FINANCIAL ACCOUNTING Assignment No.7 20-ARID-684 PROBLEMS -Bibrar ghaniNo ratings yet

- Accounting Basics Questions AnsweredDocument4 pagesAccounting Basics Questions AnsweredkalmanzaNo ratings yet

- Lesson 6 - The Major Accounts - NotesDocument18 pagesLesson 6 - The Major Accounts - NotesJoanNo ratings yet

- Hospitality QuizDocument3 pagesHospitality QuizWycliffe Luther RosalesNo ratings yet

- Week+1 Accounting+Equation+-+Solutions PDFDocument15 pagesWeek+1 Accounting+Equation+-+Solutions PDFAli Zain ParharNo ratings yet

- Tutorial - Session W1 - SolutionsDocument15 pagesTutorial - Session W1 - SolutionslizaNo ratings yet

- Accounting Equation: Fundamentals of ABM 1Document97 pagesAccounting Equation: Fundamentals of ABM 1ediwowNo ratings yet

- Quiz For Non-AccountantsDocument3 pagesQuiz For Non-AccountantsWycliffe Luther RosalesNo ratings yet

- The Accounting Equation PP TDocument39 pagesThe Accounting Equation PP TMelu Jean MayoresNo ratings yet

- AA015 Chap 2 LectureDocument5 pagesAA015 Chap 2 Lecturenorismah isaNo ratings yet

- How Do Gases BehaveDocument13 pagesHow Do Gases BehavePhilpNil8000No ratings yet

- PHILIPPINE-OPERA-AND-MUSICAL-PLAYDocument21 pagesPHILIPPINE-OPERA-AND-MUSICAL-PLAYPhilpNil8000No ratings yet

- Respiratory Diseases and DisordersDocument2 pagesRespiratory Diseases and DisordersPhilpNil8000No ratings yet

- Untitled DocumentDocument2 pagesUntitled DocumentPhilpNil8000No ratings yet

- Science 9 PointersDocument3 pagesScience 9 PointersPhilpNil8000No ratings yet

- Bookkeeping Introduction 2Document22 pagesBookkeeping Introduction 2PhilpNil8000No ratings yet

- Exercise for Fitness: Understanding Physical Fitness ComponentsDocument23 pagesExercise for Fitness: Understanding Physical Fitness ComponentsJohnne Erika LarosaNo ratings yet

- Heredity and Genetics ExplainedDocument25 pagesHeredity and Genetics ExplainedPhilpNil8000No ratings yet

- Bookeeping Double Entry SystemDocument16 pagesBookeeping Double Entry SystemPhilpNil8000No ratings yet

- Estatement20230706 000233440Document3 pagesEstatement20230706 000233440Mia NahilaNo ratings yet

- Journal General Ledger Mix Ap1234Document25 pagesJournal General Ledger Mix Ap1234api-305077843No ratings yet

- FAR Chapt 10 Answer KeyDocument21 pagesFAR Chapt 10 Answer KeyJerickho JNo ratings yet

- Ch09 WRD25e InstructorDocument62 pagesCh09 WRD25e InstructorMagdalena VindaNo ratings yet

- Gep 12 PDFDocument4 pagesGep 12 PDFAngsuman BhanjdeoNo ratings yet

- Ap 2022Document15 pagesAp 2022John Carlo D. EngayNo ratings yet

- Kimberly ClarkDocument2 pagesKimberly ClarkRanita ChatterjeeNo ratings yet

- 20180918Document4 pages20180918Nor Fauzi IsmailNo ratings yet

- 6 The Trial BalanceDocument4 pages6 The Trial Balanceayshaneasrin08No ratings yet

- Case Study - 2: Operations at WhirlpoolDocument8 pagesCase Study - 2: Operations at WhirlpoolDigvijayKumarNo ratings yet

- Online Accrual - A White PaperDocument50 pagesOnline Accrual - A White PaperManisekaran SeetharamanNo ratings yet

- Extensibility - Novas BadisDocument15 pagesExtensibility - Novas BadisSonia Gonzalez MariñoNo ratings yet

- Sap Accounting EntriesDocument7 pagesSap Accounting Entriesperera_kushan7365No ratings yet

- Accounting ProbsDocument1 pageAccounting ProbsJazzmin Rae BarbaNo ratings yet

- Activity Partnership Formation and OperationDocument8 pagesActivity Partnership Formation and OperationSharon AnchetaNo ratings yet

- CBP - Manual Reorder Point PlanningDocument13 pagesCBP - Manual Reorder Point PlanningVivek KalchuriNo ratings yet

- NadalDocument52 pagesNadalSheidee ValienteNo ratings yet

- Problem 10-10 COSTDocument3 pagesProblem 10-10 COSTElaine Fiona VillafuerteNo ratings yet

- Retail Store Design (Unit IV)Document126 pagesRetail Store Design (Unit IV)Shikhar SrivastavaNo ratings yet

- Midterm CocDocument8 pagesMidterm CocCertified Public AccountantNo ratings yet

- Changing World of Sales Management 1Document14 pagesChanging World of Sales Management 1සුමු ලියනාරච්චිNo ratings yet

- Act101 Journalizing and PostingDocument23 pagesAct101 Journalizing and PostingAMNEERA SHANIA LALANTONo ratings yet

- Inventory Voucher TypesDocument64 pagesInventory Voucher TypesUday Pali100% (1)

- Solution For Chapter 12 Accounting For Partnership (13 E)Document19 pagesSolution For Chapter 12 Accounting For Partnership (13 E)RaaNo ratings yet

- HL Pay & Save-I Account 112022 2Document2 pagesHL Pay & Save-I Account 112022 2naidaNo ratings yet

- PT JAYATAMA Account Receivable and Payable ListsDocument14 pagesPT JAYATAMA Account Receivable and Payable ListssepriyadiNo ratings yet