You might also like

- Chapter 4 MacroeconomicDocument9 pagesChapter 4 MacroeconomicPham Phu Cuong B2108182No ratings yet

- lecture4Document69 pageslecture4Edward Gabada JnrNo ratings yet

- Week 3Document44 pagesWeek 3Maqsood AhmadNo ratings yet

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- Unit 12Document7 pagesUnit 12hvcatdluluNo ratings yet

- Chapter 2 Overview of The Financial SystemDocument72 pagesChapter 2 Overview of The Financial SystemKokab Manzoor100% (1)

- Session 3Document13 pagesSession 3Mohamed BadawyNo ratings yet

- MONEYDocument11 pagesMONEYzainabNo ratings yet

- Unit-3 Commercial Banking & Retail BanksDocument97 pagesUnit-3 Commercial Banking & Retail BanksAbhikaam SharmaNo ratings yet

- 3.1 Money & BankingDocument28 pages3.1 Money & BankingappletransactionsNo ratings yet

- Chapter 4 UpdatedDocument80 pagesChapter 4 Updatedrajan20202000No ratings yet

- Banking Interview QuestionsDocument5 pagesBanking Interview Questionsresearchr.aadi02No ratings yet

- Banking in Financial System. ProjectDocument40 pagesBanking in Financial System. Projectvickyrawat1983No ratings yet

- The Role of Commercial BanksDocument29 pagesThe Role of Commercial BanksGeorge Cristinel RotaruNo ratings yet

- Money Measurement-SabaDocument18 pagesMoney Measurement-Sabas shaikhNo ratings yet

- Money and BankingDocument26 pagesMoney and BankingutkarshNo ratings yet

- Week 4Document42 pagesWeek 4Maqsood AhmadNo ratings yet

- English For Banking and FinanceDocument28 pagesEnglish For Banking and FinancefathiyarizkiNo ratings yet

- Banking, Money Supply and Monetary PolicyDocument13 pagesBanking, Money Supply and Monetary PolicySiti Nurul Alia RazaliNo ratings yet

- Chapter 1 & 2Document5 pagesChapter 1 & 2rog67558No ratings yet

- Topic 9 - Money Banking (Week8)Document40 pagesTopic 9 - Money Banking (Week8)Wei SongNo ratings yet

- Functions of MoneyDocument7 pagesFunctions of MoneyShayan YasirNo ratings yet

- Postgraduate Diploma in Islamic Finance Practices OverviewDocument83 pagesPostgraduate Diploma in Islamic Finance Practices OverviewShadman ShakibNo ratings yet

- Deposit Sources of FundsDocument6 pagesDeposit Sources of FundsSakib Chowdhury0% (1)

- Basic Banking ConceptsDocument17 pagesBasic Banking ConceptsVyasraj Singamodi100% (1)

- Basic Banking ConceptsDocument17 pagesBasic Banking ConceptsVishnuvardhan VishnuNo ratings yet

- Money & Banking: Money Meaning, Functions, Supply of Money Banking Meaning, Functions of Commercial BankDocument24 pagesMoney & Banking: Money Meaning, Functions, Supply of Money Banking Meaning, Functions of Commercial BankKunal SubaNo ratings yet

- CH 1Document37 pagesCH 1xyzNo ratings yet

- Financial System Chapter SummaryDocument23 pagesFinancial System Chapter SummaryShahid IqbalNo ratings yet

- Lesson 1: Concept and Functions of MoneyDocument31 pagesLesson 1: Concept and Functions of MoneyFind DeviceNo ratings yet

- Money and BankingDocument16 pagesMoney and BankingSiddhi JainNo ratings yet

- Banking Unit 6Document32 pagesBanking Unit 6ALAN WALKER PIANONo ratings yet

- Commercial Banks EcoDocument15 pagesCommercial Banks EcojinNo ratings yet

- What Is MoneyDocument33 pagesWhat Is Moneyد.عيد عشريNo ratings yet

- Sample NotesDocument20 pagesSample NotesKenpin EteNo ratings yet

- Financial Market, Financial InstitutionsDocument17 pagesFinancial Market, Financial InstitutionsMuhammad RadeelNo ratings yet

- Banking Services: Includes All The Operations Provided by The Banks Including To TheDocument7 pagesBanking Services: Includes All The Operations Provided by The Banks Including To TheChandrika DasNo ratings yet

- Banking Terminology: Bank - Basic FunctionsDocument8 pagesBanking Terminology: Bank - Basic Functionsshivam choudharyNo ratings yet

- POB Lesson 2 Notes (Form 4)Document27 pagesPOB Lesson 2 Notes (Form 4)Ryanna ChambersNo ratings yet

- Lecture TwoDocument28 pagesLecture TwoSajed RahmanNo ratings yet

- Financial Markets: Ana Flor V. CerboDocument25 pagesFinancial Markets: Ana Flor V. CerboLuna AndraNo ratings yet

- Macro Economics: Institution of Money & Modern EconomicsDocument36 pagesMacro Economics: Institution of Money & Modern EconomicsApeksha ShaniNo ratings yet

- Chapter 6 - Debt Securities MarketDocument15 pagesChapter 6 - Debt Securities MarketWill De Ocampo100% (1)

- Introduction To CreditDocument34 pagesIntroduction To CreditElle RaineNo ratings yet

- Evolution of MoneyDocument9 pagesEvolution of MoneySenthil Kumar GanesanNo ratings yet

- 0 - Retail Banking Doc2Document8 pages0 - Retail Banking Doc2Niyati BagweNo ratings yet

- 1 - Money, Banking, and The Financial SectorDocument138 pages1 - Money, Banking, and The Financial SectorMacNo ratings yet

- Banking Products and ServicesDocument13 pagesBanking Products and ServicesDharmeshParikhNo ratings yet

- Chapter 24 The Role and Function of Financial InstitutionsDocument3 pagesChapter 24 The Role and Function of Financial InstitutionsVỹ San KohNo ratings yet

- Lecture # 20 Branch Banking in PakistanDocument55 pagesLecture # 20 Branch Banking in PakistanImran YousafNo ratings yet

- Methods of PaymentsDocument73 pagesMethods of PaymentsIqbal ChyNo ratings yet

- Unit - Vii Commercial BanksDocument14 pagesUnit - Vii Commercial Bankssheetal rajputNo ratings yet

- Monetary EconomicsDocument12 pagesMonetary Economicsrealmadridramos1902No ratings yet

- MoneyDocument18 pagesMoneyAkshit KansalNo ratings yet

- Chapter 1-2Document40 pagesChapter 1-2jakeNo ratings yet

- 06 - Financial InstitutionsDocument14 pages06 - Financial InstitutionsJaripNo ratings yet

- Financial Institutions and ServicesDocument27 pagesFinancial Institutions and ServicesJayesh RathodNo ratings yet

- Are Repos Really LoansDocument8 pagesAre Repos Really LoansMarius AngaraNo ratings yet

- Turtle SoupDocument1 pageTurtle Soupmuhafani129No ratings yet

- ICAI 291109 - Case Studies On Buyback of SharesDocument15 pagesICAI 291109 - Case Studies On Buyback of SharesRoshan Kumar0% (1)

- Convertible Preferred Market Value and Equity Value CalculationDocument22 pagesConvertible Preferred Market Value and Equity Value CalculationAnn SerratoNo ratings yet

- FMDocument9 pagesFMashrafNo ratings yet

- Financial Management 2-UumDocument48 pagesFinancial Management 2-UumjameshsurunaNo ratings yet

- Learn about mutual fund fact sheetsDocument7 pagesLearn about mutual fund fact sheetsOwner JustACodeNo ratings yet

- Thesis On Ghana Stock ExchangeDocument4 pagesThesis On Ghana Stock Exchangeggzgpeikd100% (2)

- Ray Dalio: I Have Some Bitcoin'Document5 pagesRay Dalio: I Have Some Bitcoin'Bogdan L MorosanNo ratings yet

- Unit 1 - Indian Financial SystemDocument73 pagesUnit 1 - Indian Financial SystemHasrat AliNo ratings yet

- Daily Open-SR TechniqueDocument3 pagesDaily Open-SR Techniquetawhid anamNo ratings yet

- 2022 CFA Level 2 Curriculum Changes Summary (300hours)Document1 page2022 CFA Level 2 Curriculum Changes Summary (300hours)mawais263No ratings yet

- Lista Abreviações Oficial Completa 01.06.2022Document22 pagesLista Abreviações Oficial Completa 01.06.2022Walber SoaresNo ratings yet

- Citi TTS Seminar BASEL III Intraday LiquidityDocument13 pagesCiti TTS Seminar BASEL III Intraday LiquidityCezara EminescuNo ratings yet

- BibliographyDocument4 pagesBibliographytylerelliott1No ratings yet

- Verdhana - MSCI Indonesia February 2024 Index Rebalancing Preview, Part TwoDocument2 pagesVerdhana - MSCI Indonesia February 2024 Index Rebalancing Preview, Part TwoAdri KhosasihNo ratings yet

- CREDO PresentationDocument23 pagesCREDO PresentationPampalini01No ratings yet

- Important Questions in Securities Laws For Cs Executive Group 2Document83 pagesImportant Questions in Securities Laws For Cs Executive Group 2debanka100% (2)

- NBFC Sector ReportDocument8 pagesNBFC Sector Reportpawankaul82No ratings yet

- CH 6Document16 pagesCH 6devrajkinjalNo ratings yet

- Tutorial 3 - Risk Return (Part 2) PDFDocument2 pagesTutorial 3 - Risk Return (Part 2) PDFChamNo ratings yet

- FMG Rates - June - Upload PageDocument2 pagesFMG Rates - June - Upload Pageasif_rasheedNo ratings yet

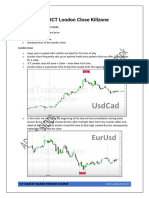

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Stock Trak ReportDocument5 pagesStock Trak Reportnhausaue100% (6)

- Way2wealth Derivatives 10jan18Document2 pagesWay2wealth Derivatives 10jan18kasNo ratings yet

- Comparable Companies TemplateDocument23 pagesComparable Companies Templatesandeep chaurasiaNo ratings yet

- BSAD 183 Fall 2018 SyllabusDocument4 pagesBSAD 183 Fall 2018 SyllabusConstantinos ConstantinouNo ratings yet

- Portfolio Investment ManagementDocument242 pagesPortfolio Investment ManagementFishah Sadri100% (4)

- Quarterly Brief: Valuation of Early-Stage CompaniesDocument17 pagesQuarterly Brief: Valuation of Early-Stage CompaniesViktorNo ratings yet

- ACF 103 Revision Qns Solns 20141Document12 pagesACF 103 Revision Qns Solns 20141danikadolorNo ratings yet