You might also like

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Final AccountsDocument15 pagesFinal AccountsVARUNKUMAR KNo ratings yet

- Financial Accounting I - Understanding the Key Financial StatementsDocument24 pagesFinancial Accounting I - Understanding the Key Financial StatementsAmmarNo ratings yet

- Understanding Financial StatementsDocument9 pagesUnderstanding Financial StatementsAbsa TraderNo ratings yet

- Final Accounts: Prof. Sweety .O. SharmaDocument10 pagesFinal Accounts: Prof. Sweety .O. SharmaAayushiNo ratings yet

- Preparing Financial Reports 4Document20 pagesPreparing Financial Reports 4alibisharadenNo ratings yet

- Preparation of Final AccountDocument32 pagesPreparation of Final AccountCHARLES FURTADONo ratings yet

- Unit 4Document85 pagesUnit 4Ankush Singh100% (1)

- Module 1 Intro To Financial Management 1Document22 pagesModule 1 Intro To Financial Management 1Jenalyn OrtegaNo ratings yet

- Unit 3 Trading ConcernDocument13 pagesUnit 3 Trading ConcernBell BottleNo ratings yet

- DP1 FM FaDocument32 pagesDP1 FM FaananditaNo ratings yet

- Components of Financial Statements#2Document5 pagesComponents of Financial Statements#2Ockouri BarnesNo ratings yet

- Accounts and TaxDocument17 pagesAccounts and Taxprasham makwanaNo ratings yet

- Financial Statements Explained: Balance Sheets, Income Statements, Cash Flows & Ratios (39Document12 pagesFinancial Statements Explained: Balance Sheets, Income Statements, Cash Flows & Ratios (39Shrutika MoreNo ratings yet

- Statement of Comprehensive IncomeDocument30 pagesStatement of Comprehensive Incomemaligaya evelyn100% (1)

- Small and Medium Enterprises Development Agency of NigeriaDocument20 pagesSmall and Medium Enterprises Development Agency of NigeriaEduardo CanelaNo ratings yet

- Final Accounts: Manufacturing, Trading and P&L A/cDocument51 pagesFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- 9 Financial Statement - Part ADocument33 pages9 Financial Statement - Part AMariam AhmedNo ratings yet

- 5.3 Income StatementDocument4 pages5.3 Income StatementHiNo ratings yet

- Tally .1Document81 pagesTally .1tbijleNo ratings yet

- Income StatementDocument7 pagesIncome Statementumarrizwan208No ratings yet

- 8 Financial StatementDocument11 pages8 Financial StatementLin Latt Wai AlexaNo ratings yet

- Accounting CycleDocument21 pagesAccounting Cyclemuhammad.16032.acNo ratings yet

- Major Accounts and the Accounting CycleDocument23 pagesMajor Accounts and the Accounting CycleVicky Ann SoriaNo ratings yet

- Financial StatementsDocument11 pagesFinancial StatementsFabiolaNo ratings yet

- Eem Unit2 AccountingDocument11 pagesEem Unit2 AccountingstudentNo ratings yet

- Tally Vol-1 - April #SKCreative2018Document34 pagesTally Vol-1 - April #SKCreative2018SK CreativeNo ratings yet

- Lecture 6 Bus. MNGMNTDocument69 pagesLecture 6 Bus. MNGMNTAizhan BaimukhamedovaNo ratings yet

- Lesson-8 Income StatementsDocument5 pagesLesson-8 Income Statementsanmolgarg129No ratings yet

- Financial Aspects in RetailDocument31 pagesFinancial Aspects in RetailPink100% (4)

- 15BCC0097 Departmental AccountsDocument9 pages15BCC0097 Departmental AccountsArun KCNo ratings yet

- Annual Report and Accounts ContentsDocument5 pagesAnnual Report and Accounts ContentsTwinkle SuriNo ratings yet

- Profit & Loss Account Balance Sheet Assets & Liabilities Fee Invoicing Annual Accounts/Auditing Tax Matters Insurance MattersDocument12 pagesProfit & Loss Account Balance Sheet Assets & Liabilities Fee Invoicing Annual Accounts/Auditing Tax Matters Insurance MattersANSLEM ALBERTNo ratings yet

- Adjustments: Steps For Recording Adjusting EntriesDocument2 pagesAdjustments: Steps For Recording Adjusting EntriesYahnsea AlfaroNo ratings yet

- PSBA Finance 1 Chapter 5 Financial StatementsDocument45 pagesPSBA Finance 1 Chapter 5 Financial StatementsEunice NunezNo ratings yet

- Statement of Comprehensive IncomeDocument25 pagesStatement of Comprehensive IncomeAngel Nichole ValenciaNo ratings yet

- Accounting and Auditing TrainingDocument31 pagesAccounting and Auditing Trainingdawn pickett100% (1)

- Income and Expenditure NotesDocument2 pagesIncome and Expenditure NotesRashmi Anand JhaNo ratings yet

- Day 3 FRA 2023Document47 pagesDay 3 FRA 2023Soumendu MandalNo ratings yet

- Accounting MechanicsDocument21 pagesAccounting MechanicsPUTTU GURU PRASAD SENGUNTHA MUDALIAR100% (1)

- Lecture 5 Chapter 2 10th January 2016Document74 pagesLecture 5 Chapter 2 10th January 2016Miraz AzadNo ratings yet

- Final AccountsDocument16 pagesFinal AccountsGurkirat SinghNo ratings yet

- S3-Managing Financial Health and PerformanceDocument36 pagesS3-Managing Financial Health and PerformanceShaheer BaigNo ratings yet

- Accounting Basics Cheat SheetDocument5 pagesAccounting Basics Cheat SheetxzxhiujinhNo ratings yet

- Financial Statement: José Manuel Rodríguez PérezDocument9 pagesFinancial Statement: José Manuel Rodríguez PérezJOSE RODRIGUEZ PEREZNo ratings yet

- Jaiib 4rd JuneDocument45 pagesJaiib 4rd JuneDeepesh SrivastavaNo ratings yet

- Chapter 4: Income Statement and Related InformationDocument15 pagesChapter 4: Income Statement and Related InformationSharif HassanNo ratings yet

- Accounting For Retailing: ©2020 John Wiley & Sons Australia LTDDocument42 pagesAccounting For Retailing: ©2020 John Wiley & Sons Australia LTDKristel Andrea100% (1)

- Module D - Final Accounts of Banks & Companies - PresentationDocument102 pagesModule D - Final Accounts of Banks & Companies - PresentationASHISH GUPTANo ratings yet

- Profit and Loss AccountDocument2 pagesProfit and Loss AccountameliarosminiNo ratings yet

- Term 2 Week 3Document42 pagesTerm 2 Week 3bhavik GuptaNo ratings yet

- Unit - 4 Final AccountDocument39 pagesUnit - 4 Final AccountHusain BohraNo ratings yet

- Basics of Book KeepingDocument62 pagesBasics of Book KeepingRodric MarbaniangNo ratings yet

- Financial Statement Theory Notes PDFDocument6 pagesFinancial Statement Theory Notes PDFAejaz MohamedNo ratings yet

- ABM5 NOTES (1st QUARTER)Document16 pagesABM5 NOTES (1st QUARTER)Adrianne Mae Almalvez Rodrigo100% (1)

- ACTBAS2 Special Journals TypesDocument8 pagesACTBAS2 Special Journals TypesEuniceNo ratings yet

- Lecture 3 DoubleentrysystemDocument47 pagesLecture 3 Doubleentrysystem叶祖儿No ratings yet

- Accounting Survival Guide: An Introduction to Accounting for BeginnersFrom EverandAccounting Survival Guide: An Introduction to Accounting for BeginnersNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Chapter 7 - Forecasting Financial StatementsDocument23 pagesChapter 7 - Forecasting Financial Statementsamanthi gunarathna95No ratings yet

- Dividend Discount ModelDocument48 pagesDividend Discount ModelRajes DubeyNo ratings yet

- Acct 033Document9 pagesAcct 033erraNo ratings yet

- Poverty in The PhilippinesDocument23 pagesPoverty in The PhilippinesDejabGuinMajaNo ratings yet

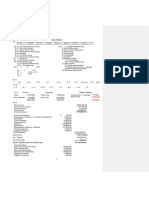

- Oct 2022 Profit and Loss Report for NiagawanDocument1 pageOct 2022 Profit and Loss Report for NiagawanNM SOLUTIONNo ratings yet

- BUS. MATH Q2 - Week3Document4 pagesBUS. MATH Q2 - Week3DARLENE MARTINNo ratings yet

- Mega Marathon Direct Tax. YtDocument257 pagesMega Marathon Direct Tax. Ytsubroshakar gamerNo ratings yet

- Accounts Case LetDocument7 pagesAccounts Case Letriya lakhotiaNo ratings yet

- CPA Review Taxation ExamDocument16 pagesCPA Review Taxation ExamAmeroden AbdullahNo ratings yet

- FINAL ACTIVITY 11-12 - (Sto. Nino)Document6 pagesFINAL ACTIVITY 11-12 - (Sto. Nino)Wena Mae LavideNo ratings yet

- Offshore Banking - Definition, Advantages & RisksDocument1 pageOffshore Banking - Definition, Advantages & RisksCrEaTiVe MiNdNo ratings yet

- PTX - AssignmentDocument15 pagesPTX - AssignmentNUR ALEEYA MAISARAH BINTI MOHD NASIR (AS)No ratings yet

- 12-ACCA-FA2-Chp 12Document26 pages12-ACCA-FA2-Chp 12SMS PrintingNo ratings yet

- C7 Gramado Đáp Án 1Document2 pagesC7 Gramado Đáp Án 1An TrịnhNo ratings yet

- Math Assignment Print SheetDocument4 pagesMath Assignment Print Sheetluca.castelvetere04No ratings yet

- Financial FeasibilityDocument53 pagesFinancial FeasibilityShyra MaximoNo ratings yet

- Partnership and Corporation Accounting Chapter 1 SolManDocument11 pagesPartnership and Corporation Accounting Chapter 1 SolManDavid BarletaNo ratings yet

- Vishal Thakkar ComputationDocument4 pagesVishal Thakkar ComputationHemant SurgicalNo ratings yet

- Business Ethics Third QTR Module Week1Document6 pagesBusiness Ethics Third QTR Module Week1Jeny FlorentinoNo ratings yet

- Chapter 12Document17 pagesChapter 12Jemaicah AmatiagaNo ratings yet

- Financial Statement Analysis: by Uditha JayasingheDocument19 pagesFinancial Statement Analysis: by Uditha JayasinghesanjuladasanNo ratings yet

- Review Questions On Financial Planning and ForecastingDocument5 pagesReview Questions On Financial Planning and ForecastingGadafi FuadNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearAbhinaba SahaNo ratings yet

- Financial Management: An OverviewDocument90 pagesFinancial Management: An OverviewGebreNo ratings yet

- Quiz 1 NotesDocument5 pagesQuiz 1 NotesShaina Monique RangasanNo ratings yet

- Sample Information Technology Business Plan TemplateDocument23 pagesSample Information Technology Business Plan TemplatehashmiajmalNo ratings yet

- Sales Budget and Financial ProjectionsDocument12 pagesSales Budget and Financial ProjectionsAbejero Trisha Nicole A.No ratings yet

- History of Ethiopian TaxationDocument4 pagesHistory of Ethiopian Taxationsara woldeyohannes100% (1)

- CFP Sample Paper Tax PlanningDocument8 pagesCFP Sample Paper Tax Planningchaitanya_koli2611No ratings yet

- Kazi Md. Mehdi Hasan2Document4 pagesKazi Md. Mehdi Hasan2Md. Obayed UllahNo ratings yet