You might also like

- A222 - Topic 4 MacsDocument29 pagesA222 - Topic 4 MacsfiqNo ratings yet

- 3Q - OM NotesDocument12 pages3Q - OM NotesCORRAL, PAUL GABRIELLE T.No ratings yet

- Introductiontomanagement 121126084622 Phpapp02Document32 pagesIntroductiontomanagement 121126084622 Phpapp02Bardhe ÇettaNo ratings yet

- HIV&HepatitisDocument46 pagesHIV&HepatitisRaja RuzannaNo ratings yet

- Math quiz on spatial figures and algebraic expressionsDocument17 pagesMath quiz on spatial figures and algebraic expressionsLetCatalyst100% (1)

- Organization - ManagementDocument11 pagesOrganization - ManagementMike Reyes (XxMKExX)No ratings yet

- Controlling ReportDocument33 pagesControlling ReportVennNo ratings yet

- Quezon City University 673 Quirino Highway Novaliches, Quezon CityDocument55 pagesQuezon City University 673 Quirino Highway Novaliches, Quezon CityKianne ChanNo ratings yet

- 1.1. Variables & ExpressionsDocument26 pages1.1. Variables & ExpressionsKzea JaeNo ratings yet

- Science Process Skills: Observe Classify Measure Infer Predict Credits Extensions About The AuthorDocument21 pagesScience Process Skills: Observe Classify Measure Infer Predict Credits Extensions About The AuthorSharmaine TuazonNo ratings yet

- Types of MapsDocument13 pagesTypes of MapsDianne Lea DamianNo ratings yet

- Algebraic Rules for Number PatternsDocument18 pagesAlgebraic Rules for Number PatternsAlex GarciaNo ratings yet

- The Beadwork LessonDocument34 pagesThe Beadwork LessonJanetNo ratings yet

- Algebraic Expressions For ClassDocument25 pagesAlgebraic Expressions For ClassRonald Abrasaldo SatoNo ratings yet

- Lessons Learned From State-Level Climate Policies To Accelerate US Climate ActionDocument9 pagesLessons Learned From State-Level Climate Policies To Accelerate US Climate ActionThe Wilson CenterNo ratings yet

- Long Division WorksheetDocument12 pagesLong Division WorksheetHoi Yuet ChauNo ratings yet

- Digital Citizenship ProjectDocument45 pagesDigital Citizenship ProjectChloe .DooleyNo ratings yet

- Chap. III Budgeting-200422Document53 pagesChap. III Budgeting-200422Gedion EndalkachewNo ratings yet

- Budget & Budgetary ControlDocument39 pagesBudget & Budgetary ControlEshael FathimaNo ratings yet

- Budgeting: Presented By: Ankit Kamal Akhilesh Rai Aakash Mishra BrijeshDocument16 pagesBudgeting: Presented By: Ankit Kamal Akhilesh Rai Aakash Mishra Brijeshbibe143kraniNo ratings yet

- Budget: Submitted By:-JappanjyotDocument16 pagesBudget: Submitted By:-JappanjyotJappanJyot Kalra100% (1)

- Budget Front OfficeDocument28 pagesBudget Front OfficeTarun GarhwalNo ratings yet

- Budget & Budgetary Control - Sem-IDocument37 pagesBudget & Budgetary Control - Sem-Ishital_vyas19870% (1)

- Budgetry ControlDocument61 pagesBudgetry ControlPranav ShandilNo ratings yet

- Meaning of Budget 1Document21 pagesMeaning of Budget 1atulchurchaNo ratings yet

- Budget by ArmaanDocument37 pagesBudget by Armaansyed bilalNo ratings yet

- Budgeting: Sowmiya.D Siva Sankar .N. V Siva Kumar Shalini Senthil Kumar Sathya NarayananDocument32 pagesBudgeting: Sowmiya.D Siva Sankar .N. V Siva Kumar Shalini Senthil Kumar Sathya NarayananSiva ShankarNo ratings yet

- MCPC 614 Budgeting GuideDocument25 pagesMCPC 614 Budgeting GuideRight Karl-Maccoy HattohNo ratings yet

- Budgeting f2Document104 pagesBudgeting f2Munyaradzi Onismas ChinyukwiNo ratings yet

- MAS.2906 - Short-Term BudgetingDocument9 pagesMAS.2906 - Short-Term BudgetingEyes SawNo ratings yet

- Budgetory Control: Presention On AccountingDocument34 pagesBudgetory Control: Presention On AccountingADITI BISWASNo ratings yet

- MS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingDocument7 pagesMS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingMonica GarciaNo ratings yet

- PPT: - Budgeting & Cost ControlDocument17 pagesPPT: - Budgeting & Cost Controlaimri_cochin100% (19)

- Financial Planning and Budgets ChapterDocument3 pagesFinancial Planning and Budgets ChapterMixx MineNo ratings yet

- BudgetsDocument10 pagesBudgetsRindai TinarwoNo ratings yet

- BSM PG College Roorkee Budgetary Control AssignmentDocument39 pagesBSM PG College Roorkee Budgetary Control AssignmentNeeraj Singh RainaNo ratings yet

- Budget and Budgetary Control-1Document44 pagesBudget and Budgetary Control-1Priya saxenaNo ratings yet

- BudgetingDocument41 pagesBudgetingkhanafshaNo ratings yet

- BSM PG College Roorkee: Assignment On AuditingDocument39 pagesBSM PG College Roorkee: Assignment On AuditingNeeraj Singh RainaNo ratings yet

- Budgetary Control Process and ImportanceDocument14 pagesBudgetary Control Process and ImportanceMansi DeokarNo ratings yet

- 2020 PDFDocument39 pages2020 PDFNeeraj Singh RainaNo ratings yet

- Esg Budget Management Final VersionDocument66 pagesEsg Budget Management Final Versionrita tamohNo ratings yet

- Perfomance BudjectingDocument72 pagesPerfomance BudjectingAnithaNo ratings yet

- Budgets and Budgetary ControlDocument42 pagesBudgets and Budgetary ControlBishnu S. MukherjeeNo ratings yet

- Budget PDFDocument74 pagesBudget PDFVaibhav GuptaNo ratings yet

- BUDGETING: KEY TO COST CONTROLDocument7 pagesBUDGETING: KEY TO COST CONTROLUdaypal Singh Rawat0% (2)

- Budgets & Budgetary Control GuideDocument39 pagesBudgets & Budgetary Control GuideNeeraj Singh RainaNo ratings yet

- Unit 13 - BudgetsDocument20 pagesUnit 13 - BudgetsAdeirehs Eyemarket BrissettNo ratings yet

- Master BudgetDocument5 pagesMaster BudgetNicole VinaraoNo ratings yet

- Chapter 14 Budget GuideDocument45 pagesChapter 14 Budget GuideJessa MartinezNo ratings yet

- BUDGETINGDocument11 pagesBUDGETINGCeceil PajaronNo ratings yet

- BUDGETARY CONTROL AND STANDARD COSTINGDocument15 pagesBUDGETARY CONTROL AND STANDARD COSTINGPratyay DasNo ratings yet

- Financial Planning and Budgets: Presented By: Rose Ann C. Paramio, Cpa, MbaDocument44 pagesFinancial Planning and Budgets: Presented By: Rose Ann C. Paramio, Cpa, MbaAki StephyNo ratings yet

- 6 - Budgetary ControlDocument18 pages6 - Budgetary ControlRakeysh RakyeshNo ratings yet

- 4 Budget and Budgetary Control SolutionsDocument74 pages4 Budget and Budgetary Control SolutionsRahul SinghNo ratings yet

- Section C. Budgetary System & Variance - TuttorsDocument61 pagesSection C. Budgetary System & Variance - TuttorsNirmal Shrestha100% (1)

- Unit 2: Business BudgetsDocument28 pagesUnit 2: Business BudgetsSHARATH JNo ratings yet

- Chapter 12 Budgeting GuideDocument59 pagesChapter 12 Budgeting GuideCristineNo ratings yet

- Budget: On The Basis of Time: According To Time, Budgets May Be Classified AsDocument11 pagesBudget: On The Basis of Time: According To Time, Budgets May Be Classified Asuday prakashNo ratings yet

- Topic 3 - Budgeting and Budgetary ControlDocument42 pagesTopic 3 - Budgeting and Budgetary ControlSYAZANA HUDA MOHD AZLINo ratings yet

- Ipsas 23: Revenue From Non Exchange TransactionsDocument11 pagesIpsas 23: Revenue From Non Exchange TransactionsHace AdisNo ratings yet

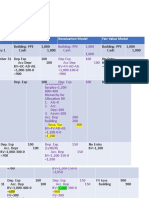

- Date Cost Model Revaluation Model Fair Value ModelDocument4 pagesDate Cost Model Revaluation Model Fair Value ModelHace AdisNo ratings yet

- Impairment of Non-Cash AssetsDocument25 pagesImpairment of Non-Cash AssetsHace AdisNo ratings yet

- Ipsas 16: Investment PropertyDocument25 pagesIpsas 16: Investment PropertyHace AdisNo ratings yet

- IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERSDocument46 pagesIFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERSHace AdisNo ratings yet

- Article Review FinalDocument5 pagesArticle Review FinalHace AdisNo ratings yet

- CHAPTER Four NewDocument16 pagesCHAPTER Four NewHace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- Finance AttachementDocument21 pagesFinance AttachementHace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument14 pagesFM II - Chapter 03, Financial Planning & ForecastingHace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- Financial Hand Out 22-2Document13 pagesFinancial Hand Out 22-2Hace AdisNo ratings yet

- BMSR - Annual Report - 2012Document66 pagesBMSR - Annual Report - 2012lakukamu8No ratings yet

- Budgeting AnswersDocument16 pagesBudgeting AnswersMuhammad Hassan UddinNo ratings yet

- Current Issues in Marketing (Teaching Plan)Document5 pagesCurrent Issues in Marketing (Teaching Plan)Eric KongNo ratings yet

- Netflix's Marketing MixDocument4 pagesNetflix's Marketing MixZaid ZubairiNo ratings yet

- EUGENIA ANDRIN NATIONAL HIGH SCHOOL MIDTERM EXAMDocument4 pagesEUGENIA ANDRIN NATIONAL HIGH SCHOOL MIDTERM EXAMAian CortezNo ratings yet

- MGT402CostAccountingSOLVEDMCQSMoreThan500 PDFDocument60 pagesMGT402CostAccountingSOLVEDMCQSMoreThan500 PDFUsman KhalidNo ratings yet

- Methods of Valuation of GoodwillDocument8 pagesMethods of Valuation of Goodwilljoysuperstar5No ratings yet

- PT Harum Energy Tbk 2021 Financial ReportDocument123 pagesPT Harum Energy Tbk 2021 Financial ReportYayu Rahayu100% (1)

- SBN 473Document27 pagesSBN 473Admin DivisionNo ratings yet

- Compilation atDocument20 pagesCompilation atAshley Levy San PedroNo ratings yet

- Comprehensive Accounting Cycle Review Problem-1Document11 pagesComprehensive Accounting Cycle Review Problem-1api-296886708100% (1)

- SuccessFactors OverviewDocument11 pagesSuccessFactors OverviewAbsar SyedNo ratings yet

- Choco BallsDocument40 pagesChoco BallsHina Baig100% (1)

- Chapter 8 - Order Management and Customer Service Flashcards - QuizletDocument4 pagesChapter 8 - Order Management and Customer Service Flashcards - QuizletXinli ShaNo ratings yet

- OOH MediaDocument28 pagesOOH MediaRony AbrahamNo ratings yet

- G 3000 Trading Statement of IncomeDocument6 pagesG 3000 Trading Statement of IncomeFrancine Angelika Conda TañedoNo ratings yet

- Bachelor of Science in Accountancy Advanced Financial Accounting and Reporting Quiz Number 1: Home Office and Branch AccountingDocument5 pagesBachelor of Science in Accountancy Advanced Financial Accounting and Reporting Quiz Number 1: Home Office and Branch AccountingJoyce Mamoko0% (1)

- Managerial Short TermismDocument30 pagesManagerial Short TermismSheharyar HamidNo ratings yet

- Second Quiz in MASDocument5 pagesSecond Quiz in MASPraise BuenaflorNo ratings yet

- MCQ MarketingDocument13 pagesMCQ MarketinglindakuttyNo ratings yet

- Analysis of The Effect of Marketing Mix On Purchasing Decisions On The Trans Park Cibubur ApartmentDocument8 pagesAnalysis of The Effect of Marketing Mix On Purchasing Decisions On The Trans Park Cibubur ApartmentInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Operations ManagementDocument277 pagesOperations ManagementdanigeletaNo ratings yet

- Final Exam Project - Amazon - Kholoud MohsenDocument19 pagesFinal Exam Project - Amazon - Kholoud MohsenChristine EskanderNo ratings yet

- Financial ReportingDocument34 pagesFinancial ReportingEunice Adjei0% (1)

- Make - Buy - Special - Order - Tutorial Sem 1 2021Document7 pagesMake - Buy - Special - Order - Tutorial Sem 1 2021Daneille BakerNo ratings yet

- MSCI ACWI Risk Weighted Index FactsheetDocument2 pagesMSCI ACWI Risk Weighted Index FactsheetRoberto PerezNo ratings yet

- Market Research On Samsung Mobile Phone PDFDocument103 pagesMarket Research On Samsung Mobile Phone PDFPriyaNo ratings yet

- The Cool, Trendy Fastrack WatchDocument29 pagesThe Cool, Trendy Fastrack WatchdeepakssinghNo ratings yet

- Digital Journey MapDocument11 pagesDigital Journey MapTahnee TsenNo ratings yet

- Chapter 1 ExerciseDocument4 pagesChapter 1 ExerciseCoffee JellyNo ratings yet