You might also like

- The Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)From EverandThe Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)Rating: 4 out of 5 stars4/5 (2)

- Sir M Visvesvaraya Institute of Management StudiesDocument32 pagesSir M Visvesvaraya Institute of Management StudiesMonil VisariyaNo ratings yet

- ABO - Week10 Non-Financial PerformanceDocument33 pagesABO - Week10 Non-Financial Performancejinman bongNo ratings yet

- Ch12 - Balanced ScorecardDocument45 pagesCh12 - Balanced Scorecard1091 Akshay kumarNo ratings yet

- Chap 020Document37 pagesChap 020Farah ThabitNo ratings yet

- BFT 509 Accounting for Business Performance Measurement SystemDocument22 pagesBFT 509 Accounting for Business Performance Measurement SystemtcsNo ratings yet

- Strategic Balanced Management ScorecardDocument34 pagesStrategic Balanced Management ScorecardKumar ManojNo ratings yet

- Lecture 9 BSCDocument43 pagesLecture 9 BSCVasunNo ratings yet

- Models of Improving Operations: Chapter EightDocument35 pagesModels of Improving Operations: Chapter EightAbdiNo ratings yet

- Balanced ScorecardDocument45 pagesBalanced ScorecardKshitij TyagiNo ratings yet

- Balanced Scorecard GuideDocument19 pagesBalanced Scorecard GuidejhafjfNo ratings yet

- Performance Measurement using BSC in Nepalese BanksDocument9 pagesPerformance Measurement using BSC in Nepalese BanksNaveed Mughal AcmaNo ratings yet

- Balanced Scorecard: Strategic ManagementDocument34 pagesBalanced Scorecard: Strategic Managementmitaa jannahNo ratings yet

- BSC and Pms Abhay 205Document42 pagesBSC and Pms Abhay 205Misganaw GishenNo ratings yet

- Balanced ScorecardDocument13 pagesBalanced ScorecardRamalingam ChandrasekharanNo ratings yet

- Balanced Scorecard 2Document45 pagesBalanced Scorecard 2Balaji Sekar100% (1)

- Module 3 PerfMetricsDocument82 pagesModule 3 PerfMetricsBalaji SekarNo ratings yet

- F5-15 Further Aspects of Performance AnalysisDocument20 pagesF5-15 Further Aspects of Performance AnalysisZakariya PkNo ratings yet

- ACC51112 Balanced ScorecardDocument6 pagesACC51112 Balanced ScorecardjasNo ratings yet

- Balance Score Card Full Color RevisiDocument34 pagesBalance Score Card Full Color RevisiDana MadalinaNo ratings yet

- Management Accounting Value Creation at Brandix LingerieDocument30 pagesManagement Accounting Value Creation at Brandix LingeriechamithNo ratings yet

- SOPDocument44 pagesSOPDian SugiartoNo ratings yet

- Power Point BSCDocument13 pagesPower Point BSCapi-3732654100% (1)

- Managing Corporate Performance with Balanced ScorecardDocument83 pagesManaging Corporate Performance with Balanced ScorecardT Ferdinand S Lumbantobing100% (1)

- Workshop Tips & Trik "Lolos" UJI KompetensiDocument44 pagesWorkshop Tips & Trik "Lolos" UJI KompetensiGatot HarmonoNo ratings yet

- Techniques Under Development in Managerial AccountingDocument27 pagesTechniques Under Development in Managerial AccountingMostafa MahmoudNo ratings yet

- Balanced ScorecardDocument72 pagesBalanced ScorecardBalaji Sekar100% (1)

- C1 IntroDocument13 pagesC1 IntroNgọc Phương HoàngNo ratings yet

- Balance ScorecardDocument55 pagesBalance ScorecardAbdulAhadNo ratings yet

- Balance Scorecard of TcsDocument17 pagesBalance Scorecard of TcsKrishna Chaitanya100% (2)

- Balanced Scorecard Measures Drive PerformanceDocument15 pagesBalanced Scorecard Measures Drive PerformanceSampat MishraNo ratings yet

- Balanced ScorecardDocument32 pagesBalanced Scorecardfaney singh100% (3)

- The Balanced Scorecard For MISDocument24 pagesThe Balanced Scorecard For MISNannu KardamNo ratings yet

- Performance Management, Evaluation, and Data AnalysisDocument18 pagesPerformance Management, Evaluation, and Data AnalysiscandraNo ratings yet

- PM Performamce NoteDocument14 pagesPM Performamce NoteAhmed TallanNo ratings yet

- Combination of Measures and Myopia - Ch11Document25 pagesCombination of Measures and Myopia - Ch11Lok Fung KanNo ratings yet

- ANL201 Study Unit 1 (Ver 20200108)Document42 pagesANL201 Study Unit 1 (Ver 20200108)Lincoln thunNo ratings yet

- The 4 Perspectives of The Balanced ScorecardDocument6 pagesThe 4 Perspectives of The Balanced Scorecardnivedita patilNo ratings yet

- Strategic Performance Measurement Balanced ScorecardDocument33 pagesStrategic Performance Measurement Balanced ScorecardJanes VuNo ratings yet

- The Balanced Scorecard: Traditional Methods of PerformanceDocument20 pagesThe Balanced Scorecard: Traditional Methods of PerformanceNawshad PervezNo ratings yet

- Construction Performance Management BasicsDocument62 pagesConstruction Performance Management Basicshaile mulunehNo ratings yet

- Balance Score Card: Roshith CP 2017MBARG151Document23 pagesBalance Score Card: Roshith CP 2017MBARG151roshith cpNo ratings yet

- Balanced Scorecard: Your Company NameDocument32 pagesBalanced Scorecard: Your Company NameSheika SuhailNo ratings yet

- Business Strategy Assignment On: Enrol. No.: 09BS0001416Document10 pagesBusiness Strategy Assignment On: Enrol. No.: 09BS0001416Vasudha SinghNo ratings yet

- Balance ScorecardDocument25 pagesBalance ScorecardJia BarrientosNo ratings yet

- Balanced Scorecard: Business Strategy I 10. Management Tools in Strategy 1/15Document15 pagesBalanced Scorecard: Business Strategy I 10. Management Tools in Strategy 1/15Mona AgarwallaNo ratings yet

- Evolution of Management Accounting Part 1: Scope and EvolutionDocument23 pagesEvolution of Management Accounting Part 1: Scope and EvolutionDabbie JoyNo ratings yet

- IT-Driven Business Process ChangeDocument36 pagesIT-Driven Business Process ChangeNirmit OzaNo ratings yet

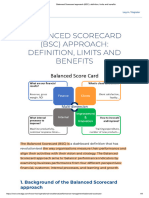

- Balanced Scorecard Approach (BSC) - Definition, Limits and BenefitsDocument9 pagesBalanced Scorecard Approach (BSC) - Definition, Limits and Benefitsritika.jain197No ratings yet

- Balance Scorecard For Finance DepttDocument10 pagesBalance Scorecard For Finance DepttVeenu SharmaNo ratings yet

- Balanced Score CardDocument6 pagesBalanced Score CarddcunhabrianNo ratings yet

- Balance Score CardDocument61 pagesBalance Score CardmadhurbvmNo ratings yet

- Ebook Balanced ScorecardDocument12 pagesEbook Balanced ScorecardReza SeptianNo ratings yet

- Balanced Scorecard ExplainedDocument16 pagesBalanced Scorecard ExplainedChann ChannNo ratings yet

- The Balanced Scorecard ApproachDocument27 pagesThe Balanced Scorecard Approachilsen100% (1)

- BSC PresentationDocument58 pagesBSC PresentationmzulfikarmuslimNo ratings yet

- Balanced Scorecard and Project ManagerDocument27 pagesBalanced Scorecard and Project ManagerRajat Mehta100% (1)

- Module 4 Balanced ScorecardDocument35 pagesModule 4 Balanced ScorecardWendryNo ratings yet

- Putting The Balanced ScorecardDocument12 pagesPutting The Balanced ScorecardArnabNo ratings yet

- Balanced ScorecardDocument13 pagesBalanced ScorecardRajiv NatarajNo ratings yet

- LAW ON BUSINESS ORGANIZATIONS: PARTNERSHIPDocument53 pagesLAW ON BUSINESS ORGANIZATIONS: PARTNERSHIPJanelle Joyce Maranan DipasupilNo ratings yet

- PRC List of DGR CoursesDocument1 pagePRC List of DGR Coursesnaveen thomasNo ratings yet

- Warranty Against Hidden DefectDocument5 pagesWarranty Against Hidden DefectYannah HidalgoNo ratings yet

- Address: Organisation DetailsDocument2 pagesAddress: Organisation DetailsFree PressNo ratings yet

- Shreya Acc MCQDocument34 pagesShreya Acc MCQSHREYA S 200526No ratings yet

- Executive Summary FritzDocument13 pagesExecutive Summary FritzethelNo ratings yet

- Harbeck Responds To Letter From Cong. GarrettDocument28 pagesHarbeck Responds To Letter From Cong. GarrettIlene KentNo ratings yet

- Unit II - CFDocument26 pagesUnit II - CFuser 02No ratings yet

- PL AccessDocument1 pagePL AccessBrayan Calcina BellotNo ratings yet

- Marketing Management Notes Unit 1Document34 pagesMarketing Management Notes Unit 1Saumya SinghNo ratings yet

- Risk Assessment Checklist: Insert Company Logo HereDocument17 pagesRisk Assessment Checklist: Insert Company Logo HereRaffique HazimNo ratings yet

- Appendix 66 - RPCI - UpdatedDocument1 pageAppendix 66 - RPCI - UpdatedJimley CanillaNo ratings yet

- Acct Statement - XX9642 - 10082022Document87 pagesAcct Statement - XX9642 - 10082022sunkenapelli adityaNo ratings yet

- Advantages and Disadvantages of E-CommerceDocument7 pagesAdvantages and Disadvantages of E-CommercekipovoNo ratings yet

- CEO List 2022 1Document26 pagesCEO List 2022 1pawan nishalNo ratings yet

- Supply Chain HubsDocument19 pagesSupply Chain HubsKavitha Reddy GurrralaNo ratings yet

- 48Document2 pages48Vladimir KrylosovNo ratings yet

- Problems 3) Inadequate Expertise (Lack of Knowledge and Skills)Document3 pagesProblems 3) Inadequate Expertise (Lack of Knowledge and Skills)ROS SHAHNo ratings yet

- SAP IRPA Estimation PDFDocument1 pageSAP IRPA Estimation PDFJMNo ratings yet

- MidtermsDocument8 pagesMidtermsRhea BadanaNo ratings yet

- ACCA P5 GTG Question Bank - 2011Document180 pagesACCA P5 GTG Question Bank - 2011raqifiluz86% (22)

- Parle Group 2 Market ResearchDocument9 pagesParle Group 2 Market ResearchVikrant KarhadkarNo ratings yet

- The New B2B Marketing Playbook: Executive SummaryDocument11 pagesThe New B2B Marketing Playbook: Executive Summaryaggold616No ratings yet

- Risk Assessment Correct AnswersDocument27 pagesRisk Assessment Correct AnswersКристинаNo ratings yet

- Project Final - Corp. Law II 2022-23Document11 pagesProject Final - Corp. Law II 2022-23Lalbee SNo ratings yet

- Capital Today FINAL PPMDocument77 pagesCapital Today FINAL PPMAshish AgrawalNo ratings yet

- SHALINI CV PDFDocument2 pagesSHALINI CV PDFSanjay JindalNo ratings yet

- IntroductiontoAccounting STDocument328 pagesIntroductiontoAccounting STAbsara Khan100% (1)

- Business Phrasal VerbsDocument3 pagesBusiness Phrasal Verbsdarlene bryant-popelierNo ratings yet

- ABDT2043 FUNDAMENTALS OF MARKETING TUTORIAL 1 WEEK 1Document4 pagesABDT2043 FUNDAMENTALS OF MARKETING TUTORIAL 1 WEEK 1Calvin TanNo ratings yet