You might also like

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- Understanding Goods and Services TaxDocument23 pagesUnderstanding Goods and Services TaxTEst User 44452No ratings yet

- GST PPT Tkil FinalDocument53 pagesGST PPT Tkil FinalVikas SharmaNo ratings yet

- GST in India: Prepared By:-Shubham SharmaDocument57 pagesGST in India: Prepared By:-Shubham Sharmamurali140No ratings yet

- Goods and Service Tax (GST)Document19 pagesGoods and Service Tax (GST)Saurabh Kumar SharmaNo ratings yet

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocument30 pagesGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- Goods and Service Tax (GST) : Biggest Indirect Tax Reform in IndiaDocument26 pagesGoods and Service Tax (GST) : Biggest Indirect Tax Reform in Indiafal_engNo ratings yet

- GST Annual Return and AuditDocument10 pagesGST Annual Return and AuditRachit ChhedaNo ratings yet

- 51 GST Flyer - Chapter 47 - TDS On GSTDocument5 pages51 GST Flyer - Chapter 47 - TDS On GSTRanjanNo ratings yet

- PPT-on-GST Annual-ReturnDocument33 pagesPPT-on-GST Annual-Returnshrutha p jainNo ratings yet

- Task 8Document23 pagesTask 8Anooja SajeevNo ratings yet

- Benefits of GSTDocument3 pagesBenefits of GSTVasundhara SinghNo ratings yet

- GST Pracital Class 2Document7 pagesGST Pracital Class 2Nayan JhaNo ratings yet

- GST PPT TaxguruDocument30 pagesGST PPT TaxgurupraveerNo ratings yet

- Bank of India Fund BasedDocument33 pagesBank of India Fund Basedhariram v choudharyNo ratings yet

- GST Impact On Distribution NetworkDocument17 pagesGST Impact On Distribution NetworkrahulNo ratings yet

- Unit1 GSTDocument26 pagesUnit1 GSTAryan SethiNo ratings yet

- Debate Against GSTDocument3 pagesDebate Against GSTKshitij Gaur100% (3)

- GST mcq-5Document14 pagesGST mcq-5Avik DasNo ratings yet

- Anil's Commerce +3 3Rd Yr Unit - 3Document26 pagesAnil's Commerce +3 3Rd Yr Unit - 3Justin ChanduNo ratings yet

- GST Compendium September 2022Document48 pagesGST Compendium September 2022sbsreddyNo ratings yet

- DT RevisionDocument133 pagesDT RevisionharshallahotNo ratings yet

- GST GuideDocument46 pagesGST GuideVikasNo ratings yet

- GST Notes-CA Inter-May 23 1 Lyst8910 PDFDocument172 pagesGST Notes-CA Inter-May 23 1 Lyst8910 PDFMaheshkumar PerlaNo ratings yet

- GST PDFDocument81 pagesGST PDFPankaj JainNo ratings yet

- GST Study MaterialDocument30 pagesGST Study Materialkowc kousalyaNo ratings yet

- GST Impact On The Supply ChainDocument8 pagesGST Impact On The Supply ChainAamiTataiNo ratings yet

- E CircularDocument3 pagesE Circularkethan kumarNo ratings yet

- Supply GSTDocument16 pagesSupply GSTMehak Kaushikk100% (1)

- GSTDocument9 pagesGSTCelina AlexNo ratings yet

- Seattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitDocument15 pagesSeattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitGeekWireNo ratings yet

- Impact of GST On Warehousing and Supply ChainDocument39 pagesImpact of GST On Warehousing and Supply ChainSundaravaradhan Iyengar100% (6)

- GST Vs VATDocument22 pagesGST Vs VATalmNo ratings yet

- Vision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaDocument24 pagesVision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaAnam FatimaNo ratings yet

- E-Book On GST by CA. (DR.) G. S. Grewal - 2020Document58 pagesE-Book On GST by CA. (DR.) G. S. Grewal - 2020Aarav DhingraNo ratings yet

- Chargeble GSTDocument87 pagesChargeble GSTgopaljha84No ratings yet

- Income Tax & GST: 2 Mark Questions With Answers - (Calicut University)Document2 pagesIncome Tax & GST: 2 Mark Questions With Answers - (Calicut University)Ashwini GanigerNo ratings yet

- Invoice: Page 1 of 3Document3 pagesInvoice: Page 1 of 3CA Shrikant VaranasiNo ratings yet

- Central ExciseDocument53 pagesCentral ExciseSuyash JainNo ratings yet

- GST - A Game Changer: 2. Review of LiteratureDocument3 pagesGST - A Game Changer: 2. Review of LiteratureMoumita Mishra100% (1)

- GST User ManuelDocument195 pagesGST User Manuelsakthi raoNo ratings yet

- GST BookDocument100 pagesGST BookNaman ChopraNo ratings yet

- PLA Refunds Post GSTDocument35 pagesPLA Refunds Post GSTManish Sachdeva67% (9)

- Goods & Services Act FinalDocument78 pagesGoods & Services Act FinalParvesh AghiNo ratings yet

- Audit Under Fiscal Laws GST AuditDocument4 pagesAudit Under Fiscal Laws GST AuditRanjit BhogesaraNo ratings yet

- Inter CA DT JKSC Mumbai-Prof - Aagam Dalal (May 23 Nov 23)Document176 pagesInter CA DT JKSC Mumbai-Prof - Aagam Dalal (May 23 Nov 23)pradeep ozaNo ratings yet

- Financial Model For 1 Year MBA - Is It Worth Going For 1 Year MBADocument7 pagesFinancial Model For 1 Year MBA - Is It Worth Going For 1 Year MBAAnurag SingalNo ratings yet

- Chapter 5 Composition Scheme Nov 2020Document41 pagesChapter 5 Composition Scheme Nov 2020Alka GuptaNo ratings yet

- Transmission in IndiaDocument36 pagesTransmission in IndiaMuhammad AdilNo ratings yet

- GST OverviewDocument15 pagesGST OverviewHimanshu ChandnaNo ratings yet

- Mathematics Class 10: Goods and Service Tax (GS T)Document10 pagesMathematics Class 10: Goods and Service Tax (GS T)Mohd Yousha AnsariNo ratings yet

- 40 Final Accounts FormatDocument3 pages40 Final Accounts FormatAditya GowdaNo ratings yet

- GST ChallanDocument2 pagesGST ChallanAkshay GangradeNo ratings yet

- Dr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawDocument9 pagesDr. Shakuntala Misra National Rehabilitation University: Lucknow Faculty of LawVimal SinghNo ratings yet

- IGSTDocument5 pagesIGSTAnonymous I5SUhZwNo ratings yet

- GST in India - Objectives, Concerns and ChallengesDocument44 pagesGST in India - Objectives, Concerns and Challengesakhilca87% (15)

- Overview GSTDocument56 pagesOverview GSTrahulNo ratings yet

- GST BasicsDocument56 pagesGST BasicsrahulNo ratings yet

- Overview of GST - PPT For GACDocument57 pagesOverview of GST - PPT For GACRonak DesaiNo ratings yet

- Regions StatementDocument4 pagesRegions StatementTemecco BufordNo ratings yet

- Boe 7 ZM Ua WYg 8 PTRNDocument9 pagesBoe 7 ZM Ua WYg 8 PTRNprakash pardeshiNo ratings yet

- Product Variants - CA Biz Elite/CA Biz - Premium /CA Biz-Advantage /CA Biz-Standard/ CA - SELDocument4 pagesProduct Variants - CA Biz Elite/CA Biz - Premium /CA Biz-Advantage /CA Biz-Standard/ CA - SELVikram JhaNo ratings yet

- Income Tax - ElaineDocument11 pagesIncome Tax - ElaineSamsung AccountNo ratings yet

- Eonnext - 3rd of Jun - 25th of Jun 2023Document5 pagesEonnext - 3rd of Jun - 25th of Jun 2023qzvg5csbmnNo ratings yet

- Bustax Very Easy Quiz1Document9 pagesBustax Very Easy Quiz1GianJoshuaDayritNo ratings yet

- Coj 2018-08-06 550402465Document2 pagesCoj 2018-08-06 550402465Benny BerniceNo ratings yet

- Form 1707 PDFDocument2 pagesForm 1707 PDFNetweightNo ratings yet

- Income Taxation of Proprietary Educational InstitutionsDocument2 pagesIncome Taxation of Proprietary Educational InstitutionsRegina Grace GadoNo ratings yet

- VRIDDHIDocument18 pagesVRIDDHIshashwatsaketNo ratings yet

- ROI CALCULATION - MBA MKT 1 - Shivam JadhavDocument4 pagesROI CALCULATION - MBA MKT 1 - Shivam JadhavShivam JadhavNo ratings yet

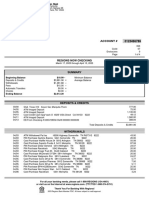

- Account StatementDocument12 pagesAccount StatementpunugauriNo ratings yet

- Í Jn5Sè Ryanârepolloâbesi Rya R Ç2F' 2lî Ryan Repollo BesidDocument3 pagesÍ Jn5Sè Ryanârepolloâbesi Rya R Ç2F' 2lî Ryan Repollo Besidraymund12345No ratings yet

- Monthly Statement: This Month's SummaryDocument3 pagesMonthly Statement: This Month's SummarySibiviswa RajendranNo ratings yet

- Accounting Level II Assignment 3Document2 pagesAccounting Level II Assignment 3EdomNo ratings yet

- Accounting Voucher DisplayDocument1 pageAccounting Voucher DisplayYoGesh PaWarNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)AvinaSh GirsawaleNo ratings yet

- Work AllotmentDocument2 pagesWork AllotmentasarthiNo ratings yet

- Associate Payment Slip - HarmonyDocument1 pageAssociate Payment Slip - Harmonykhanjodetejas491No ratings yet

- Tax Order of PaymentDocument3 pagesTax Order of PaymentLea NartatezNo ratings yet

- Taxation Homework 1 PDFDocument4 pagesTaxation Homework 1 PDFKNVS Siva KumarNo ratings yet

- Bba G V Unit-Ii GST-309 E-NotesDocument20 pagesBba G V Unit-Ii GST-309 E-NotesDeepanshu baghanNo ratings yet

- Resume Ravi Kumar L 15yrs F&ADocument3 pagesResume Ravi Kumar L 15yrs F&AYamini SharmaNo ratings yet

- Efektivitas E-Samsat, Pajak Progresif Dan Kualitas Pelayanan Terhadap Kepatuhan Wajib Pajak Kendaraan BermotorDocument12 pagesEfektivitas E-Samsat, Pajak Progresif Dan Kualitas Pelayanan Terhadap Kepatuhan Wajib Pajak Kendaraan BermotorWira Eka WulandariNo ratings yet

- Annex A Timta 2022Document8 pagesAnnex A Timta 2022Nestly MendezNo ratings yet

- Net Operating Losses (Nols) For Individuals, Estates, and TrustsDocument12 pagesNet Operating Losses (Nols) For Individuals, Estates, and TrustsAdi PutraNo ratings yet

- SW 2Document2 pagesSW 2Miss IstiNo ratings yet

- ANUBIS Ticket PrintDocument1 pageANUBIS Ticket Printkapil chavanNo ratings yet

- Tax Notes Chapter 4Document3 pagesTax Notes Chapter 4Sam ReyesNo ratings yet

- Compliance ManualDocument52 pagesCompliance ManualNupur GajjarNo ratings yet