You might also like

- Cost Volume Profit AnalysisDocument63 pagesCost Volume Profit AnalysisJunaid KhalidNo ratings yet

- Chapter 7Document49 pagesChapter 7farahNo ratings yet

- Lect # 10a CVPDocument44 pagesLect # 10a CVPAimen KhanNo ratings yet

- Lecture CVPDocument58 pagesLecture CVPKashif RaheemNo ratings yet

- Chap 005 Cost BehaviorDocument66 pagesChap 005 Cost Behaviorromi naibahoNo ratings yet

- Cost Behavior: Analysis and UseDocument66 pagesCost Behavior: Analysis and UseJayson ReyesNo ratings yet

- Be601 Lecture7 (Module6 CVP) 03nov21 ClassDocument36 pagesBe601 Lecture7 (Module6 CVP) 03nov21 ClassMohammad Musa AbidNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Presentation Chapter 6 - CompletedDocument49 pagesPresentation Chapter 6 - CompletedStephanie Ayu PraditaNo ratings yet

- Lecture 3: 27 September 2017: CIA2009: Management AccountingDocument74 pagesLecture 3: 27 September 2017: CIA2009: Management AccountingPublisherNo ratings yet

- COST ESTIMATION A Class Lecture by Rashid Hussain 1657763473Document55 pagesCOST ESTIMATION A Class Lecture by Rashid Hussain 1657763473HiteshSandhalNo ratings yet

- Session-7: Cost Analysis For Decision MakingDocument81 pagesSession-7: Cost Analysis For Decision MakingAnkitShettyNo ratings yet

- Microsoft PowerPoint - Chap005 (Compatibility Mode) 3Document1 pageMicrosoft PowerPoint - Chap005 (Compatibility Mode) 3Noor HossainNo ratings yet

- 1b - Cost Concepts and Terminology - 14sept06Document31 pages1b - Cost Concepts and Terminology - 14sept06Zaid AnsariNo ratings yet

- Fundamental: Managerial Accounting ConceptsDocument17 pagesFundamental: Managerial Accounting ConceptsRosh OtojanovNo ratings yet

- Cost Volume ProvitDocument57 pagesCost Volume ProvitannisaNo ratings yet

- Cost Behavior - Analysis and Use-1Document83 pagesCost Behavior - Analysis and Use-1Sabbir ZisNo ratings yet

- Accounting and Financial Management: Cost Volume Profit AnalysisDocument50 pagesAccounting and Financial Management: Cost Volume Profit AnalysisParas DhakaNo ratings yet

- Chapter 6 - Presentation - Virtual Classroom - MDocument34 pagesChapter 6 - Presentation - Virtual Classroom - Mrebeccahf7No ratings yet

- Assignment # 2 Submitted To: Sir Tahir Mehmmood Submitted By: Class - Section: BBA (3) - BDocument6 pagesAssignment # 2 Submitted To: Sir Tahir Mehmmood Submitted By: Class - Section: BBA (3) - BAhmadshabir ShabirNo ratings yet

- IPPTChap 006Document48 pagesIPPTChap 006Khaled BarakatNo ratings yet

- Managerial Accounting Managerial AccountingDocument30 pagesManagerial Accounting Managerial Accountingpvsk17072005No ratings yet

- Chap 011Document75 pagesChap 011Farah ThabitNo ratings yet

- Marginal CostingDocument33 pagesMarginal CostingYaminiDevpuraSomaniNo ratings yet

- 02-Cost-Terms-Concepts-and-Behavior - Managerial AccountingDocument58 pages02-Cost-Terms-Concepts-and-Behavior - Managerial Accountingsabrina jane falconNo ratings yet

- ACC202 SU6 Jan2020Document31 pagesACC202 SU6 Jan2020hashtagjxNo ratings yet

- Introduction To Cost ManagementDocument31 pagesIntroduction To Cost ManagementVINCENT GAYRAMONNo ratings yet

- END3972 Week2 v2Document27 pagesEND3972 Week2 v2Enes TürksalNo ratings yet

- Cost-Volume-Profit AnalysisDocument56 pagesCost-Volume-Profit AnalysisAgatNo ratings yet

- Chapter Two-1Document50 pagesChapter Two-1Nagiib Haibe Ibrahim Awale 6107No ratings yet

- Cost Behavior-Analysis and UseDocument74 pagesCost Behavior-Analysis and UseGraciously ElleNo ratings yet

- Week 3-Cost BehaviorDocument19 pagesWeek 3-Cost BehaviorRichard Oliver CortezNo ratings yet

- Cost BehaviorDocument29 pagesCost BehaviorLucy UnNo ratings yet

- Chapter 2S - Cost Behavior (Supplementary of Chapter 2)Document53 pagesChapter 2S - Cost Behavior (Supplementary of Chapter 2)Stavria KalliNo ratings yet

- MALec Batch 2Document105 pagesMALec Batch 2duong duongNo ratings yet

- CVP AnalysisDocument21 pagesCVP AnalysisDaksh AnejaNo ratings yet

- Cost Behavior PowerpointDocument50 pagesCost Behavior PowerpointPrecious SanchezNo ratings yet

- Slide Chapter 2Document65 pagesSlide Chapter 2daoviethung29No ratings yet

- Cost BehaviorDocument20 pagesCost BehaviorJonathan JibuNo ratings yet

- Lecture Aid Cost BehaviorDocument5 pagesLecture Aid Cost BehaviorKatleen AvisoNo ratings yet

- Cost Behavior: Analysis and Use: Mcgraw-Hill /irwinDocument72 pagesCost Behavior: Analysis and Use: Mcgraw-Hill /irwinDavid CarlNo ratings yet

- Chapter 5 Cost BehaviourDocument50 pagesChapter 5 Cost Behaviourmarizemeyer2No ratings yet

- Chapter 5 ReviewDocument9 pagesChapter 5 Reviewណយ សុវណ្ណNo ratings yet

- Chapter 3 - Cost BehaviourDocument30 pagesChapter 3 - Cost BehaviourMaha IqrarNo ratings yet

- Cost Behavior: Analysis and Use: Chapter FourDocument66 pagesCost Behavior: Analysis and Use: Chapter FourMahfuzNo ratings yet

- Cost Classification Based On Cost BehaviorDocument38 pagesCost Classification Based On Cost Behaviorshriya2413No ratings yet

- Microsoft PowerPoint - Chap005 (Compatibility Mode) 2Document1 pageMicrosoft PowerPoint - Chap005 (Compatibility Mode) 2Noor HossainNo ratings yet

- MAS Hilton Chap06Document33 pagesMAS Hilton Chap06YahiMicuaVillandaNo ratings yet

- Chapter 3.1Document52 pagesChapter 3.1EISEN BELWIGANNo ratings yet

- An Introduction To Cost Terms and PurposesDocument33 pagesAn Introduction To Cost Terms and PurposesCarrie ChanNo ratings yet

- Chapter 3 Cost Behavior Analysis and UseDocument45 pagesChapter 3 Cost Behavior Analysis and UseMarriel Fate Cullano100% (1)

- Lesson 4 HND in Business Unit 5 Management AccountingDocument32 pagesLesson 4 HND in Business Unit 5 Management AccountingShan Wikoon LLB LLM100% (3)

- Act 202. Chap002Document18 pagesAct 202. Chap002Mahmudulhasan PallabNo ratings yet

- CVP AnalysisDocument21 pagesCVP Analysisrangoli maheshwariNo ratings yet

- Acct 202 Ch5Document39 pagesAcct 202 Ch5Hải Anh LươngNo ratings yet

- Profitability Analysis FrameworkpdfDocument10 pagesProfitability Analysis FrameworkpdfObalowu Bolaji YusufNo ratings yet

- How Costs Vary With Output in The Short Run and in The Long RunDocument69 pagesHow Costs Vary With Output in The Short Run and in The Long RunKavisha RatraNo ratings yet

- 5 CVP Sep 2023Document38 pages5 CVP Sep 2023acare.carrotNo ratings yet

- Cost Behavior: Analysis and UseDocument31 pagesCost Behavior: Analysis and UsekumarNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- AEM 6210 Selecting Supplier 29-8-2023Document24 pagesAEM 6210 Selecting Supplier 29-8-2023Mahbubur MasnunNo ratings yet

- Merchandisers - . - Manufacturers - .Document14 pagesMerchandisers - . - Manufacturers - .Mahbubur MasnunNo ratings yet

- 2 ElectrostaticsDocument8 pages2 ElectrostaticsMahbubur MasnunNo ratings yet

- 2nd Paper Chapter 9 Atomic Model and Nuclear PhysicsDocument10 pages2nd Paper Chapter 9 Atomic Model and Nuclear PhysicsMahbubur MasnunNo ratings yet

- PlanningDocument10 pagesPlanningMahbubur MasnunNo ratings yet

- Shaw 1992Document14 pagesShaw 1992Mahbubur MasnunNo ratings yet

- The Contribution Margin Format of The Income Statement Emphasizes Cost BehaviorDocument3 pagesThe Contribution Margin Format of The Income Statement Emphasizes Cost BehaviorMahbubur MasnunNo ratings yet

- Lin 2019Document8 pagesLin 2019Mahbubur MasnunNo ratings yet

- Layout-1Document16 pagesLayout-1Mahbubur MasnunNo ratings yet

- L3 - Statistical Quality ControlDocument22 pagesL3 - Statistical Quality ControlMahbubur MasnunNo ratings yet

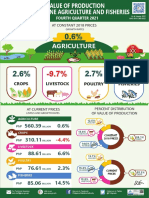

- Infographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Document1 pageInfographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Cart LaneNo ratings yet

- Dasacon Sdn. BHD.: Operation During The Movement Control OrderDocument1 pageDasacon Sdn. BHD.: Operation During The Movement Control OrderAiman ZhafriNo ratings yet

- Dependency Theory and The Latin American ExperienceDocument2 pagesDependency Theory and The Latin American ExperienceKate Angellou Jawood100% (1)

- Autocorrelation-Applied TestsDocument16 pagesAutocorrelation-Applied TestsAnsigar ChuwaNo ratings yet

- Rs. 113.7 Rs.38739.92 Rs.38821.43: Account Statement ForDocument3 pagesRs. 113.7 Rs.38739.92 Rs.38821.43: Account Statement Forirfan shamaNo ratings yet

- Ldce - Fasp - 06 PDFDocument8 pagesLdce - Fasp - 06 PDFDinesh Talele100% (4)

- Cement Industry Analysis Model 2Document5 pagesCement Industry Analysis Model 2shadyNo ratings yet

- Homework 2 DoneDocument4 pagesHomework 2 Donemythien94No ratings yet

- List Karyawan Wap, Dss & TristarDocument1 pageList Karyawan Wap, Dss & TristarLinda MargaritaNo ratings yet

- Floor HardenerDocument2 pagesFloor Hardenerhks1209No ratings yet

- Macroeconomics 9Th Edition Abel Solutions Manual Full Chapter PDFDocument36 pagesMacroeconomics 9Th Edition Abel Solutions Manual Full Chapter PDFjames.coop639100% (12)

- Barro 2000 - Inequality and Growth in A Panel of CountriesDocument28 pagesBarro 2000 - Inequality and Growth in A Panel of Countriesbb_tt_AANo ratings yet

- BanKO Partner Outlet LocatorDocument344 pagesBanKO Partner Outlet LocatorBPI Globe BanKONo ratings yet

- Roller-Ironers en Rel02Document9 pagesRoller-Ironers en Rel02kato davidNo ratings yet

- الطاقة المتجددة كخيار استراتيجي لتحقيق التنمية المستدامةDocument14 pagesالطاقة المتجددة كخيار استراتيجي لتحقيق التنمية المستدامةُElhadj arabaNo ratings yet

- Master Fee Schedule (Policy-Fees) 2022 Draft Plus MemoDocument109 pagesMaster Fee Schedule (Policy-Fees) 2022 Draft Plus MemoNBC MontanaNo ratings yet

- Transcription - Charl Cilliers (06.09.18)Document86 pagesTranscription - Charl Cilliers (06.09.18)Leila DouganNo ratings yet

- Customer Service Case StudiesDocument4 pagesCustomer Service Case Studiessameer maddubaigari80% (5)

- HRDocument2 pagesHRkiranaNo ratings yet

- Kawooya RoscoDocument2 pagesKawooya RoscoMwesigwa SamuelNo ratings yet

- EHV Application FormatDocument2 pagesEHV Application FormatsunilgvoraNo ratings yet

- Memorandum of Understanding-SubvendorsDocument3 pagesMemorandum of Understanding-SubvendorsfazilskNo ratings yet

- 09 - Chapter 6. - 7 PDFDocument23 pages09 - Chapter 6. - 7 PDFMotiram paudelNo ratings yet

- Vietnam May 23Document8 pagesVietnam May 23ImpExp TradeNo ratings yet

- Rms Form 48013716 Notice of DisposalDocument1 pageRms Form 48013716 Notice of DisposalJessica Ruiz CocaNo ratings yet

- Economics B ComDocument9 pagesEconomics B ComIkram Ul Haq0% (1)

- Practice Problems Econ 101eDocument4 pagesPractice Problems Econ 101eVince Ginno DaywanNo ratings yet

- UAE Digest Jun 06Document68 pagesUAE Digest Jun 06Fa Hian100% (2)

- Acct Statement - XX6440 - 28032023Document16 pagesAcct Statement - XX6440 - 28032023Maran PrabakaranNo ratings yet

- Excel Problem Set 2 FIN 5203 SP21 PDFDocument3 pagesExcel Problem Set 2 FIN 5203 SP21 PDFAhmed MahmoudNo ratings yet