You might also like

- 4th Gr. CMLDocument54 pages4th Gr. CMLsanjeet_kaur_100% (1)

- 3rd Grade CML Answer KeyDocument29 pages3rd Grade CML Answer Keysanjeet_kaur_10No ratings yet

- HCCC Overview and SpecificationDocument68 pagesHCCC Overview and SpecificationMohammad Umer InamNo ratings yet

- Building A Brand Is Like Building A HouseDocument123 pagesBuilding A Brand Is Like Building A HouseTapan Kumar Mallick100% (1)

- SPOUSES RAINIER JOSE M. YULO AND JULIET L. YULO vs. BANK OF THE PHILIPPINE ISLANDSDocument2 pagesSPOUSES RAINIER JOSE M. YULO AND JULIET L. YULO vs. BANK OF THE PHILIPPINE ISLANDSRizza Angela Mangalleno100% (1)

- Ibs Genting Highlands 1 30/06/19Document5 pagesIbs Genting Highlands 1 30/06/19ZhiChaoLeongNo ratings yet

- Smollan Group - Brief CredentialsDocument23 pagesSmollan Group - Brief Credentialsashish_agrawal80204809No ratings yet

- Module 1 - Time Value of Money Handout For LMS 2020Document8 pagesModule 1 - Time Value of Money Handout For LMS 2020sandeshNo ratings yet

- Financial Management FM 1: Introduction & Time Value of MoneyDocument20 pagesFinancial Management FM 1: Introduction & Time Value of MoneyharryworldNo ratings yet

- The Time Value of MoneyDocument25 pagesThe Time Value of MoneyShveta HastirNo ratings yet

- Time Value of MoneyDocument7 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- Time Value of MoneyDocument24 pagesTime Value of MoneySXCEcon PostGrad 2021-23No ratings yet

- Time Value of MoneyDocument76 pagesTime Value of Moneyrhea agnesNo ratings yet

- Time Value of MoneyDocument37 pagesTime Value of MoneyDarrell PhilipNo ratings yet

- The Time Value of Money: Topic 3Document35 pagesThe Time Value of Money: Topic 3lazycat1703No ratings yet

- Time Value of MoneyDocument10 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- Unit 2Document13 pagesUnit 2anas khanNo ratings yet

- The Time Value of MoneyDocument29 pagesThe Time Value of Moneymasandvishal50% (2)

- Basic QuantDocument12 pagesBasic Quantchickenmurgi365No ratings yet

- Time Value of MoneyDocument78 pagesTime Value of Moneyneha_baid_167% (3)

- Module 1Document53 pagesModule 1SSNo ratings yet

- Lec 4 Economic ConsiderationDocument52 pagesLec 4 Economic ConsiderationSampa DasNo ratings yet

- Unit-II ADocument26 pagesUnit-II APaytm KaroNo ratings yet

- 8 The Time Value of MoneyDocument19 pages8 The Time Value of MoneyRaj KumarNo ratings yet

- Capital Budgeting 02Document28 pagesCapital Budgeting 02VageeshaRajapakseNo ratings yet

- Study Material For Corporate FinanceDocument62 pagesStudy Material For Corporate FinanceAnant JainNo ratings yet

- Time Value of MoneyDocument36 pagesTime Value of Moneybisma9681No ratings yet

- 4th QTR Week 4-5 - Time Value Money (Part 1)Document47 pages4th QTR Week 4-5 - Time Value Money (Part 1)Nichole Joy XielSera TanNo ratings yet

- 302time Value of MoneyDocument69 pages302time Value of MoneypujaadiNo ratings yet

- Time Value of MoneyDocument38 pagesTime Value of MoneyLaiba KhanNo ratings yet

- Corporate Finance - V - STDocument13 pagesCorporate Finance - V - STSubhana NasimNo ratings yet

- Time Value of MoneyDocument54 pagesTime Value of Moneyayomi6515No ratings yet

- Topic 2 FINANCIAL MANAGEMENT - VALUATION CONCEPTS, LIRA UNIVERSITYDocument17 pagesTopic 2 FINANCIAL MANAGEMENT - VALUATION CONCEPTS, LIRA UNIVERSITYPule JackobNo ratings yet

- Lecture 3rd Time Value of MoneyDocument26 pagesLecture 3rd Time Value of MoneyBahrawar saidNo ratings yet

- PFP Unit 1 Time Value of MoneyDocument40 pagesPFP Unit 1 Time Value of MoneyAnkit KumarNo ratings yet

- TMVTBDocument17 pagesTMVTBShantam RajanNo ratings yet

- Time Value of Money, Risk and Return and Financial AnalysisDocument15 pagesTime Value of Money, Risk and Return and Financial AnalysisBETHMI MITHARA JAYAWARDENANo ratings yet

- Basic of Corporate FinanceDocument44 pagesBasic of Corporate FinanceekanshjiNo ratings yet

- Bus FinDocument119 pagesBus FinIsha GarciaNo ratings yet

- 2time Value of MoneyDocument64 pages2time Value of MoneySagar KhairnarNo ratings yet

- Finance Written ReportDocument8 pagesFinance Written ReportKOUJI N. MARQUEZNo ratings yet

- FINMAN1 Module5Document10 pagesFINMAN1 Module5Jayron NonguiNo ratings yet

- Time Value of MoneyDocument60 pagesTime Value of MoneyAtta MohammadNo ratings yet

- Chapter - 6 - Time Value of MoneyDocument27 pagesChapter - 6 - Time Value of MoneyMahe990No ratings yet

- Time Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaDocument84 pagesTime Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaWaqas Siddique SammaNo ratings yet

- Mathematics For FinanceDocument12 pagesMathematics For FinanceAbhishek PrabhakarNo ratings yet

- Capital Budgeting TheoryDocument8 pagesCapital Budgeting TheorySweta AgarwalNo ratings yet

- The Time Value of MoneyDocument28 pagesThe Time Value of MoneyRajat ShrinetNo ratings yet

- FIN 242 Chapter 10 (Mathematic of Finance)Document24 pagesFIN 242 Chapter 10 (Mathematic of Finance)MUHAMMAD FAUZAN ABU BAKARNo ratings yet

- Concept of Value and Return Question and AnswerDocument4 pagesConcept of Value and Return Question and Answervinesh1515No ratings yet

- Bus Fin Mod 6Document33 pagesBus Fin Mod 6taebearNo ratings yet

- Time Value of MoneyDocument15 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- Capital Budgeting TutorialDocument26 pagesCapital Budgeting Tutorialf20221182No ratings yet

- CUZ CORP FIN Time Value For Money-1Document16 pagesCUZ CORP FIN Time Value For Money-1KIMBERLY MUKAMBANo ratings yet

- FMCF - Unit 1Document22 pagesFMCF - Unit 1Deepak VermaNo ratings yet

- Chapter Two: How To Calculate Present ValuesDocument31 pagesChapter Two: How To Calculate Present ValuesYusuf HusseinNo ratings yet

- Time Value of MoneyDocument60 pagesTime Value of MoneyJash ChhedaNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- Capital Budgeting - I: Gourav Vallabh Xlri JamshedpurDocument64 pagesCapital Budgeting - I: Gourav Vallabh Xlri JamshedpurSimran JainNo ratings yet

- FM Notes by Dipan SirDocument178 pagesFM Notes by Dipan SirchimbanguraNo ratings yet

- 01 TVMDocument47 pages01 TVMSaranya GedelaNo ratings yet

- Chapter 04 (Final Energy Financial Management)Document19 pagesChapter 04 (Final Energy Financial Management)rathneshkumarNo ratings yet

- Rate of Return InflationDocument12 pagesRate of Return InflationShreya SinglaNo ratings yet

- Financial Management: by K Lubza NiharDocument21 pagesFinancial Management: by K Lubza NiharAashutosh MishraNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- Session 8 - Equity Valuation, Risk and ReturnDocument11 pagesSession 8 - Equity Valuation, Risk and Returnsanjeet_kaur_10No ratings yet

- Session 15 - Estimation of Cash FlowsDocument4 pagesSession 15 - Estimation of Cash Flowssanjeet_kaur_10No ratings yet

- Session 1 - IntroductionDocument24 pagesSession 1 - Introductionsanjeet_kaur_10No ratings yet

- Adventures in BookbindingDocument145 pagesAdventures in Bookbindingsanjeet_kaur_10No ratings yet

- CBSE Class 4 Punjabi WorksheetDocument4 pagesCBSE Class 4 Punjabi Worksheetsanjeet_kaur_10No ratings yet

- Ginger Cook Basics The Dirty Dozen Insanely Easy Acrylic Painting TipsDocument1 pageGinger Cook Basics The Dirty Dozen Insanely Easy Acrylic Painting Tipssanjeet_kaur_10No ratings yet

- Chocolate Cake Food Network Ina GartenDocument2 pagesChocolate Cake Food Network Ina Gartensanjeet_kaur_10No ratings yet

- CML Grade 4 SampleDocument2 pagesCML Grade 4 Samplesanjeet_kaur_10No ratings yet

- Companies Amendment Act 2021 GazetteDocument9 pagesCompanies Amendment Act 2021 GazetteNajeebullah KardaarNo ratings yet

- Sustainability Analysis On NVDADocument24 pagesSustainability Analysis On NVDABalaji PadmanabanNo ratings yet

- Plate For Mounting Robotarm UR3 Item and Bosch ProfilesDocument1 pagePlate For Mounting Robotarm UR3 Item and Bosch ProfilesVickocorp SlpNo ratings yet

- Hybrid Container Clients Mobiliser Apps: SAP Back EndDocument1 pageHybrid Container Clients Mobiliser Apps: SAP Back EndPadma KotamsettiNo ratings yet

- Philippine Mining Act of 1995Document19 pagesPhilippine Mining Act of 1995Chamamhile Lanzespi67% (3)

- Corpotare Status:: N/A N/A N/ADocument3 pagesCorpotare Status:: N/A N/A N/AAdnan MasoodNo ratings yet

- MGMT UNDocument357 pagesMGMT UNEXPOGREENNo ratings yet

- THE CONCEPT OF KAIZEN-How Hybe Corporation Implements The Principle of Continuous Improvement - KERENOBARADocument16 pagesTHE CONCEPT OF KAIZEN-How Hybe Corporation Implements The Principle of Continuous Improvement - KERENOBARAKeren ObaraNo ratings yet

- Consumer BehaviorDocument6 pagesConsumer Behaviorshivam goyalNo ratings yet

- Wallstreetjournaleurope 20170609 The Wall Street Journal EuropeDocument36 pagesWallstreetjournaleurope 20170609 The Wall Street Journal EuropestefanoNo ratings yet

- ABA 2021 Midwinter FMLA Report of 2020 CasesDocument211 pagesABA 2021 Midwinter FMLA Report of 2020 Caseseric_meyer8174No ratings yet

- Scope of Retailing in ChhattishgarhDocument3 pagesScope of Retailing in Chhattishgarhnavneet sNo ratings yet

- CESSDA Strategy 2018 2022Document18 pagesCESSDA Strategy 2018 2022Muhammad PebriyansyahNo ratings yet

- Code of ConductDocument5 pagesCode of ConductTerryNo ratings yet

- Mortgage Leads GuideDocument16 pagesMortgage Leads GuideAli 69No ratings yet

- Wal-Mart Changes Tactics To Meet International TastesDocument9 pagesWal-Mart Changes Tactics To Meet International TastesjimmybansalNo ratings yet

- Shareholder's EquityDocument6 pagesShareholder's EquityRock LeeNo ratings yet

- Agn006 CDocument12 pagesAgn006 CKolakaluri MadhuNo ratings yet

- UNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBDocument71 pagesUNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBswethaNo ratings yet

- LOI (PT. Tarfiha-)Document2 pagesLOI (PT. Tarfiha-)PriyoNo ratings yet

- Marketing Management 13Th Edition Kotler Test Bank Full Chapter PDFDocument49 pagesMarketing Management 13Th Edition Kotler Test Bank Full Chapter PDFmalabarhumane088100% (13)

- 2 Theories of SellingDocument31 pages2 Theories of SellingPiyush Gulati100% (1)

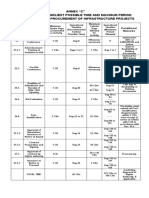

- Timelines InfrastructureDocument1 pageTimelines InfrastructureGie Bernal CamachoNo ratings yet

- Karnena Tejeshwar Rao - H3456D17 - DeveloperDocument6 pagesKarnena Tejeshwar Rao - H3456D17 - Developerranjithramesh555No ratings yet

- Consolidation of Differentiation StrategyDocument57 pagesConsolidation of Differentiation StrategyKe Lun ChuaNo ratings yet