You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- IFP September 2013Document11 pagesIFP September 2013Shakil KhanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- IFP June 2013Document20 pagesIFP June 2013Shakil KhanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- IFP Feb and Mar 2013Document17 pagesIFP Feb and Mar 2013Shakil KhanNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- IFP - July and August 2013Document17 pagesIFP - July and August 2013Shakil KhanNo ratings yet

- IFP May 2013Document12 pagesIFP May 2013Shakil KhanNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- IFP Apr 2013Document12 pagesIFP Apr 2013Shakil KhanNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- IFP Jan 2013Document14 pagesIFP Jan 2013Shakil KhanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- IFP - Aug and Sep 2012Document13 pagesIFP - Aug and Sep 2012Shakil KhanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- IFP - Nov 2012Document9 pagesIFP - Nov 2012Shakil KhanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- IFP - Oct 2012Document8 pagesIFP - Oct 2012Shakil KhanNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- IFP - May 2012Document8 pagesIFP - May 2012Shakil KhanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- IFP - Aug and Sep 2012Document13 pagesIFP - Aug and Sep 2012Shakil KhanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- IFP - Jan 2012Document10 pagesIFP - Jan 2012Shakil KhanNo ratings yet

- IFP - July 2012Document14 pagesIFP - July 2012Shakil KhanNo ratings yet

- IFP - December 2012Document13 pagesIFP - December 2012Shakil KhanNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- IFP - Feb 2012Document9 pagesIFP - Feb 2012Shakil KhanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- IFP - June 2012Document14 pagesIFP - June 2012Shakil KhanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- IFP - Aug 2012Document13 pagesIFP - Aug 2012Shakil KhanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- IFP - April 2012Document9 pagesIFP - April 2012Shakil KhanNo ratings yet

- Tadabbur-042 Surah ShuraDocument61 pagesTadabbur-042 Surah ShuraMonty AlfiantoNo ratings yet

- A Dictionary of Kashmiri Proverbs & SayingsDocument280 pagesA Dictionary of Kashmiri Proverbs & Sayingsatulya k50% (2)

- Rise of Islam & Caliphates in Central Islamic LandsDocument31 pagesRise of Islam & Caliphates in Central Islamic LandsHarsh SharmaNo ratings yet

- Mindanao Halal Food Corporation to Boost Halal IndustryDocument3 pagesMindanao Halal Food Corporation to Boost Halal IndustryJossie EjercitoNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- New Age-Fr Mitch PacwaDocument15 pagesNew Age-Fr Mitch PacwaFrancis LoboNo ratings yet

- Planning To Influence The Inflential Women of Society Aug 2023Document13 pagesPlanning To Influence The Inflential Women of Society Aug 2023faisalsdq1No ratings yet

- Eulogy of Sayyidi Ali Cisse by Shaikh Ahmad ShabanDocument17 pagesEulogy of Sayyidi Ali Cisse by Shaikh Ahmad Shabanabubakr fingerNo ratings yet

- Rangkuman Penilaian Positive PersonDocument10 pagesRangkuman Penilaian Positive PersonAndi PangeranNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Lec#2 TaklifiDocument20 pagesLec#2 TaklifiSaba BatoolNo ratings yet

- Lesson NotesDocument188 pagesLesson NotesSadettin KoçNo ratings yet

- 1 - Introduction To HalalDocument57 pages1 - Introduction To HalalNur ShazieyahNo ratings yet

- Children With DisabilityDocument89 pagesChildren With DisabilityMariakatrinuuhNo ratings yet

- Book BindingDocument19 pagesBook BindingZalozba Ignis67% (3)

- Time and Works of NarasimhaDocument6 pagesTime and Works of NarasimhaArun Kumar UpadhyayNo ratings yet

- The Qur'an and Modern Science by Dr. Maurice BucailleDocument22 pagesThe Qur'an and Modern Science by Dr. Maurice BucailleJamshaidzubairee50% (2)

- Civil Muslim Marriage ContractDocument3 pagesCivil Muslim Marriage ContractVicky RajaNo ratings yet

- Bahasa Indonesia Klas XIIDocument13 pagesBahasa Indonesia Klas XIIHIDAYATNo ratings yet

- Holy Quran in Roman Urdu - 20 ParahDocument22 pagesHoly Quran in Roman Urdu - 20 ParahKhanSummy100% (1)

- Tafsir Bi Al-DirayahDocument1 pageTafsir Bi Al-DirayahRasyad KamalNo ratings yet

- Jurnal PrakaryaDocument28 pagesJurnal PrakaryaAndra Mahar FadillahNo ratings yet

- A Commentary On Theistic Arguments - Jawadi AmuliDocument271 pagesA Commentary On Theistic Arguments - Jawadi AmuliSahrianNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

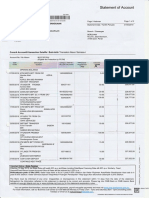

- Cimbislamic: Statement of AccountDocument1 pageCimbislamic: Statement of AccountAuristene Dos Anjos CostaNo ratings yet

- Banking Helping Desk For Jalalpur Jattan BranchesDocument23 pagesBanking Helping Desk For Jalalpur Jattan BranchesMoghees RazaNo ratings yet

- Jurnal Penelitian Hukum De Jure Vol 20 No 2Document16 pagesJurnal Penelitian Hukum De Jure Vol 20 No 2Bagas Syahfudiantoro IINo ratings yet

- Apa Referencing: A Brief Guide: All APA Examples SearchDocument10 pagesApa Referencing: A Brief Guide: All APA Examples SearchFaie SollehNo ratings yet

- Baclochistan Board of Intermediate and Secondary Education Past Papers 9th Science 5 YearsDocument61 pagesBaclochistan Board of Intermediate and Secondary Education Past Papers 9th Science 5 Yearsasan booksNo ratings yet

- Quaid's Vision of Peaceful Foreign Policy for PakistanDocument4 pagesQuaid's Vision of Peaceful Foreign Policy for PakistanHamzaNo ratings yet

- History of TrigoDocument2 pagesHistory of TrigoArrianne ZeannaNo ratings yet

- ৭ টি জীবনীDocument24 pages৭ টি জীবনীdroughplayerNo ratings yet

- Quote BookDocument91 pagesQuote BookKirsten RossNo ratings yet