You might also like

- Demand Forecasting Indian Textile IndustryDocument23 pagesDemand Forecasting Indian Textile IndustryAbhishek Moses RichardNo ratings yet

- Alphamed Formulations PVT LTDDocument51 pagesAlphamed Formulations PVT LTDBhargav BezawadaNo ratings yet

- Export Procedure in JCT LTD - Textile IndustryDocument52 pagesExport Procedure in JCT LTD - Textile IndustrydikshaluNo ratings yet

- Baseline Survey Technical Textiles Sector 20042022Document652 pagesBaseline Survey Technical Textiles Sector 20042022Space MuskNo ratings yet

- Final Textile IndustryDocument121 pagesFinal Textile IndustryJas KaurNo ratings yet

- Demonetisation in India: A Study of Its' Impact On Various Key SectorsDocument8 pagesDemonetisation in India: A Study of Its' Impact On Various Key SectorsHimanshuNo ratings yet

- Mirza International Pvt. Ltd.Document93 pagesMirza International Pvt. Ltd.Arjun PatelNo ratings yet

- Introduction To Packaging IndustryDocument85 pagesIntroduction To Packaging Industryshellybal50% (2)

- A Project Report On ExideDocument90 pagesA Project Report On ExidePiyush Bhardwaj100% (3)

- Indian Automobile IndustryDocument10 pagesIndian Automobile IndustryneemolnNo ratings yet

- EuroChem - Europe - Final PDFDocument36 pagesEuroChem - Europe - Final PDFYuvrajNo ratings yet

- CSR Indian OilDocument9 pagesCSR Indian OilDeepak NayakNo ratings yet

- Ralco PROJECT REPORTDocument67 pagesRalco PROJECT REPORTSahil Nayyar100% (2)

- Data Analysis and InterpretationDocument7 pagesData Analysis and InterpretationATS PROJECT DEPARTMENTNo ratings yet

- Procurement, Processing & Distribution of Basmati Rice Special Reference Jagat Agro IndustriesDocument86 pagesProcurement, Processing & Distribution of Basmati Rice Special Reference Jagat Agro IndustriesKhushboo Khanna100% (1)

- List of Operational SEZs in IndiaDocument128 pagesList of Operational SEZs in IndiaParesh LilaNo ratings yet

- Pranav Kaistha ReportDocument18 pagesPranav Kaistha ReportRahul JunejaNo ratings yet

- Customer Satisfaction Varun MotorsDocument66 pagesCustomer Satisfaction Varun Motorsbhanu prasadNo ratings yet

- Textile Industry in India Project ReportDocument16 pagesTextile Industry in India Project ReportmitNo ratings yet

- Indian Textile Industry Chapter 1Document6 pagesIndian Textile Industry Chapter 1himanshuNo ratings yet

- Survey of Steel Industries in India To Study The Potential For Waste Heat Recovery Boilers For Electric Arc FurnaceDocument42 pagesSurvey of Steel Industries in India To Study The Potential For Waste Heat Recovery Boilers For Electric Arc FurnaceChinmay JoshiNo ratings yet

- Challenges in Individual Investment During PandemicDocument22 pagesChallenges in Individual Investment During Pandemicroshini rajendranNo ratings yet

- EPGDM - Project Report GuidelinesDocument7 pagesEPGDM - Project Report GuidelinesManish GuptaNo ratings yet

- A Project Report OnDocument7 pagesA Project Report OnbanalavjuNo ratings yet

- EXIMDocument18 pagesEXIMPushpak RoyNo ratings yet

- Growth Trends in Cotton Textile Industry in India and Tamil NaduDocument6 pagesGrowth Trends in Cotton Textile Industry in India and Tamil NaduJohn HaynesNo ratings yet

- Marketing Strategies of Top FMCG Retail Stores in IndiaDocument76 pagesMarketing Strategies of Top FMCG Retail Stores in IndiaSimar ZuluNo ratings yet

- Medical Tourism: Medical Tourism and The Growth of Health Care Sector in IndiaDocument7 pagesMedical Tourism: Medical Tourism and The Growth of Health Care Sector in IndiaAbhinav RanaNo ratings yet

- Logistics & Supply Chain Management Interim Project ReportDocument29 pagesLogistics & Supply Chain Management Interim Project ReportSuduNo ratings yet

- Final ThesisDocument225 pagesFinal ThesisAnonymous VdwBhb4frFNo ratings yet

- Investment Strategy For Indian Markets Post-CovidDocument21 pagesInvestment Strategy For Indian Markets Post-CovidJcoveNo ratings yet

- Textile IndustryDocument80 pagesTextile Industryankitmehta23No ratings yet

- A Study of Organized Retail Sector S Growth and Its Future Prospects in IndiaDocument9 pagesA Study of Organized Retail Sector S Growth and Its Future Prospects in IndiaBarunNo ratings yet

- Indian Textile Industry Evaluation and Future OpportunitiesDocument45 pagesIndian Textile Industry Evaluation and Future OpportunitiesVikram RattaNo ratings yet

- Black BookDocument12 pagesBlack BookAbhijit NambiarNo ratings yet

- An Organization Study at TULSYAN NEC LTD: Objectives of The StudyDocument81 pagesAn Organization Study at TULSYAN NEC LTD: Objectives of The StudyShowmiya MahaNo ratings yet

- Salem Steel PlantDocument69 pagesSalem Steel PlantKavuthu Mathi100% (2)

- ShodhgangaDocument52 pagesShodhgangaChrz J100% (1)

- List of Licensed Commercial Banks in NepalDocument2 pagesList of Licensed Commercial Banks in Nepalnocadmin100% (1)

- DSM Textile IndustryDocument30 pagesDSM Textile IndustryeshuNo ratings yet

- Profile of Bajaj Pulsar Bike CustomersDocument70 pagesProfile of Bajaj Pulsar Bike CustomersvinothNo ratings yet

- Strategic Management Mid ProjectDocument25 pagesStrategic Management Mid ProjectDea HandayaniNo ratings yet

- Consumer's Perception Towards FOUR WHEELER INDUSTRYDocument91 pagesConsumer's Perception Towards FOUR WHEELER INDUSTRYShubhamprataps0% (1)

- Project Report On Digiworld at MumbaiDocument77 pagesProject Report On Digiworld at Mumbaisantosh888888No ratings yet

- Womens Health Challenges in Unorganized ConstructionDocument94 pagesWomens Health Challenges in Unorganized ConstructionShashank KUmar Rai Bhadur100% (1)

- Industrial Research Project: Version 1.0, 9 July, 2021 School of Business UPES, DehradunDocument5 pagesIndustrial Research Project: Version 1.0, 9 July, 2021 School of Business UPES, Dehradunraja rockyNo ratings yet

- Indian Pharma Industry OverviewDocument9 pagesIndian Pharma Industry OverviewrakeshNo ratings yet

- Project Guidelines From Mumbai UniversityDocument3 pagesProject Guidelines From Mumbai UniversityRavi VaithyNo ratings yet

- Amul Industr-BBA-MBA Project ReportDocument61 pagesAmul Industr-BBA-MBA Project ReportpRiNcE DuDhAtRaNo ratings yet

- Indian Oil (PBM)Document37 pagesIndian Oil (PBM)AsraNo ratings yet

- Final Report Based On 60 Days Market Work As A Nilons' Army Soldier in Mumbai MarketDocument54 pagesFinal Report Based On 60 Days Market Work As A Nilons' Army Soldier in Mumbai MarketKabir SinghNo ratings yet

- Summer InternshipDocument60 pagesSummer InternshipAyush AroraNo ratings yet

- Project Report ON A Comprehensive Study of Indian Banking SystemDocument55 pagesProject Report ON A Comprehensive Study of Indian Banking Systemkaushal2442No ratings yet

- Tata Vs HyundaiDocument49 pagesTata Vs HyundaiAnkit SethNo ratings yet

- Jai Beverages Company ProfileDocument4 pagesJai Beverages Company ProfileSherry SherNo ratings yet

- Aayush Leather IndustryDocument50 pagesAayush Leather IndustryRahul JaiswalNo ratings yet

- Portrait of an Industrial City: 'Clanging Belfast' 1750-1914From EverandPortrait of an Industrial City: 'Clanging Belfast' 1750-1914No ratings yet

- Indian Textile IndustryDocument17 pagesIndian Textile IndustryVin BankaNo ratings yet

- Project On Vardhman - ManishDocument46 pagesProject On Vardhman - ManishManish JhaNo ratings yet

- Cotton Textiles in IndiaDocument3 pagesCotton Textiles in IndiaNitin ShettyNo ratings yet

- Climate defined as weather averaged over 30 yearsDocument4 pagesClimate defined as weather averaged over 30 yearsSakhamuri Ram'sNo ratings yet

- Capital Budgeting VishakaDocument105 pagesCapital Budgeting VishakaSakhamuri Ram'sNo ratings yet

- "Funds Flow Statement": Eswar College of EngineeringDocument8 pages"Funds Flow Statement": Eswar College of EngineeringSakhamuri Ram'sNo ratings yet

- MBA Program VIIT: Performance Appraisal ProcessDocument86 pagesMBA Program VIIT: Performance Appraisal ProcessSakhamuri Ram'sNo ratings yet

- SpencersDocument12 pagesSpencersSakhamuri Ram'sNo ratings yet

- Funds Flow StatementDocument101 pagesFunds Flow StatementSakhamuri Ram'sNo ratings yet

- Funds Flow Statement Tirumala MilkDocument101 pagesFunds Flow Statement Tirumala MilkSakhamuri Ram's100% (3)

- Capital Budgeting CclaDocument50 pagesCapital Budgeting CclaSakhamuri Ram'sNo ratings yet

- Ratio Analysis 1012Document74 pagesRatio Analysis 1012Sakhamuri Ram'sNo ratings yet

- Financial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Document11 pagesFinancial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Sakhamuri Ram'sNo ratings yet

- Narasimhulu CR COLLEGE Funds Flow 021Document94 pagesNarasimhulu CR COLLEGE Funds Flow 021Sakhamuri Ram'sNo ratings yet

- Financial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Document11 pagesFinancial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Sakhamuri Ram'sNo ratings yet

- List of The Tables: SL NO NO Title of The Table Page NoDocument9 pagesList of The Tables: SL NO NO Title of The Table Page NoSakhamuri Ram'sNo ratings yet

- Capital Budgeting Krishna MurthyDocument54 pagesCapital Budgeting Krishna MurthySakhamuri Ram'sNo ratings yet

- Financial Statement Analysis of Tirumala MilkDocument6 pagesFinancial Statement Analysis of Tirumala MilkSakhamuri Ram'sNo ratings yet

- Financial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Document11 pagesFinancial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Sakhamuri Ram'sNo ratings yet

- Capital Budgeting KarimullaDocument51 pagesCapital Budgeting KarimullaSakhamuri Ram'sNo ratings yet

- Dairy IndustryDocument16 pagesDairy IndustrySakhamuri Ram'sNo ratings yet

- Industry Indan Cotton Textile ProfileDocument30 pagesIndustry Indan Cotton Textile ProfileSakhamuri Ram'sNo ratings yet

- Performance AppraisalDocument85 pagesPerformance AppraisalSakhamuri Ram'sNo ratings yet

- Master of Business Administration: A Study On Ratio Analysis With Reference To Jocil LimitedDocument97 pagesMaster of Business Administration: A Study On Ratio Analysis With Reference To Jocil LimitedSakhamuri Ram'sNo ratings yet

- Amaravathi 16 PointsdDocument16 pagesAmaravathi 16 PointsdSakhamuri Ram'sNo ratings yet

- CottonDocument17 pagesCottonSakhamuri Ram's100% (1)

- Cotton IndustryDocument18 pagesCotton IndustrySakhamuri Ram'sNo ratings yet

- Sreemsbi ResumeDocument4 pagesSreemsbi ResumeSakhamuri Ram'sNo ratings yet

- Sagar Cement PointsDocument16 pagesSagar Cement PointsSakhamuri Ram'sNo ratings yet

- VivekDocument24 pagesVivekSakhamuri Ram'sNo ratings yet

- Employee performance report by monthDocument2 pagesEmployee performance report by monthSakhamuri Ram'sNo ratings yet

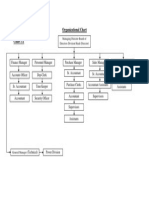

- Organizational Chart 3.1 - Management StructureDocument1 pageOrganizational Chart 3.1 - Management StructureSakhamuri Ram'sNo ratings yet