You might also like

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDocument52 pagesSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- Christine Sousa BagsDocument8 pagesChristine Sousa BagsKaila Clarisse Cortez100% (5)

- Simple Compound Complex and Compound Complex SentencesDocument7 pagesSimple Compound Complex and Compound Complex SentencesRanti HarviNo ratings yet

- (Bloom's Modern Critical Views) (2000)Document267 pages(Bloom's Modern Critical Views) (2000)andreea1613232100% (1)

- Crime and Punishment Vocabulary 93092Document2 pagesCrime and Punishment Vocabulary 93092Rebeca Alfonso Alabarta50% (4)

- Acctg Problem 7Document4 pagesAcctg Problem 7Salvie Perez Utana57% (14)

- Ily Abella Surveyors - WorksheetDocument2 pagesIly Abella Surveyors - WorksheetNeilan Jay FloresNo ratings yet

- Starmada House RulesDocument2 pagesStarmada House Ruleshvwilson62No ratings yet

- Afar Partnership LiquidationDocument42 pagesAfar Partnership LiquidationKrizia Mae Uzielle PeneroNo ratings yet

- PDF-Afar CompressDocument128 pagesPDF-Afar CompressCharisse VisteNo ratings yet

- Ae 100 Section L Navarro, LainaDocument14 pagesAe 100 Section L Navarro, LainaLaina Recel NavarroNo ratings yet

- A) Show The Effects of The Above Transactions On The Accounting Equation Using The Following FormatDocument4 pagesA) Show The Effects of The Above Transactions On The Accounting Equation Using The Following FormatMark CalimlimNo ratings yet

- PTE GURU - Will Provide You Template For Following SST, SWT, RETELL, DI and ESSAY and at The End Some Good Knowledge of Scoring SystemDocument6 pagesPTE GURU - Will Provide You Template For Following SST, SWT, RETELL, DI and ESSAY and at The End Some Good Knowledge of Scoring Systemrohit singh100% (1)

- Project ManagementDocument37 pagesProject ManagementAlfakri WaleedNo ratings yet

- Maria Hernandez & Associates: Case Study #1Document6 pagesMaria Hernandez & Associates: Case Study #1Susy CifuentesNo ratings yet

- Maria Hernandez SolutionDocument13 pagesMaria Hernandez SolutionShashank PatelNo ratings yet

- Accounts Unadjusted Trial Balance Adjustments Ajusted Trial Balance Income Statement Balance Sheet Debit Credit Debit Credit DR CR DR CR DR CRDocument4 pagesAccounts Unadjusted Trial Balance Adjustments Ajusted Trial Balance Income Statement Balance Sheet Debit Credit Debit Credit DR CR DR CR DR CRGIDEON, JR. INESNo ratings yet

- Tutorial 2 (Suggested Solution)Document2 pagesTutorial 2 (Suggested Solution)DyksterNo ratings yet

- Fund Flow Statement NumericalsDocument9 pagesFund Flow Statement Numericalsjaydeep kriplaniNo ratings yet

- Assets, Liabilities and Equity of ARA Galleries Pty LTD As at 30 June 2017Document4 pagesAssets, Liabilities and Equity of ARA Galleries Pty LTD As at 30 June 2017BáchHợpNo ratings yet

- Accounting 1 (Chapter 9)Document3 pagesAccounting 1 (Chapter 9)angel cao100% (2)

- Activities and Assesment 2Document4 pagesActivities and Assesment 2Mante, Josh Adrian Greg S.No ratings yet

- Accounting - Trial BalanceDocument1 pageAccounting - Trial Balancefranchesca.dejesus.educNo ratings yet

- Vending Machines SolutionDocument6 pagesVending Machines SolutionizquierdofacturaNo ratings yet

- Transaction Analysis Janelle'SRESTAURANTDocument2 pagesTransaction Analysis Janelle'SRESTAURANTReana ReyesNo ratings yet

- 2021 SM2 Tutorial 02 InClass SolutionDocument3 pages2021 SM2 Tutorial 02 InClass SolutionZhu ZiRuiNo ratings yet

- Chapter 4 - Partnership Liquidation Practice ExercisesDocument3 pagesChapter 4 - Partnership Liquidation Practice ExercisessanjoeNo ratings yet

- FAR Chapter 4Document5 pagesFAR Chapter 4Celine Therese BuNo ratings yet

- Quiz 1 SFM AnswerDocument4 pagesQuiz 1 SFM Answerangelicacas063No ratings yet

- 17 - Accounting For Incomplete Records (Single Entry)Document7 pages17 - Accounting For Incomplete Records (Single Entry)KAMAL POKHRELNo ratings yet

- Assignment - Basics of AccountingDocument1 pageAssignment - Basics of AccountingSamadhi KatagodaNo ratings yet

- FA2 - CFS SOlutionDocument1 pageFA2 - CFS SOlutionKc SevillaNo ratings yet

- Consolidation FP ExampleDocument4 pagesConsolidation FP ExampleYoooNo ratings yet

- Consolidation FP ExampleDocument4 pagesConsolidation FP ExampleYAUHANo ratings yet

- Accounting EquationDocument4 pagesAccounting Equationunknown PersonNo ratings yet

- WorksheetDocument1 pageWorksheetjoygie124apigoNo ratings yet

- Fabm 1Document5 pagesFabm 1Lady Aleah Naharah P. AlugNo ratings yet

- Jawaban CH 5 - TM 11Document3 pagesJawaban CH 5 - TM 11ahmad shinigamiNo ratings yet

- Rico - Assignment IaDocument18 pagesRico - Assignment IaGwen TimoteoNo ratings yet

- Accn 101 Assignment Group WorkDocument8 pagesAccn 101 Assignment Group WorkkumbiraidavidNo ratings yet

- Worksheet J. P. Peralta Computer ClinicDocument2 pagesWorksheet J. P. Peralta Computer ClinicMinjin lesner ManalansanNo ratings yet

- Profit 220,333.3 3 220,333.33Document1 pageProfit 220,333.3 3 220,333.33CookiemonsterNo ratings yet

- SBR1 Dummy With Cash FlowDocument15 pagesSBR1 Dummy With Cash Flowakansha.associate.workNo ratings yet

- Mahusay, Bsa 315, Module 1-CaseletsDocument9 pagesMahusay, Bsa 315, Module 1-CaseletsJeth MahusayNo ratings yet

- Indirect MethodDocument4 pagesIndirect MethodjustinreyNo ratings yet

- Exercise 8-7 Page 319Document3 pagesExercise 8-7 Page 319Dianne Jane LirayNo ratings yet

- Assignment TwoDocument10 pagesAssignment TwoTeke TarekegnNo ratings yet

- J. P. Peralta Computer Clinic Worksheet For The Month Ended December 31, 2020Document2 pagesJ. P. Peralta Computer Clinic Worksheet For The Month Ended December 31, 2020Minjin lesner ManalansanNo ratings yet

- Account Name Trial Balance Income Statement Capital Statement Balance SheetDocument2 pagesAccount Name Trial Balance Income Statement Capital Statement Balance SheetMeryl BinoNo ratings yet

- Actbfar Exercise #2Document8 pagesActbfar Exercise #2Janela Venice SantosNo ratings yet

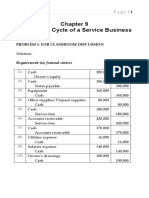

- Chapter 9 Problem 1 SolutionDocument8 pagesChapter 9 Problem 1 SolutionAustin Coles83% (6)

- Hotel Abc Hotel Abc Balance Sheet Cash Flow Statement As Per 31 December 2020 As of 31 December 2020Document2 pagesHotel Abc Hotel Abc Balance Sheet Cash Flow Statement As Per 31 December 2020 As of 31 December 2020Yoga SaputraNo ratings yet

- Perpetual Answer KeyDocument11 pagesPerpetual Answer KeyRichelle Janine Dela CruzNo ratings yet

- Chapter 2 - Partnership Operations PROBLEM 6 and 8 With Worksheet 6.)Document12 pagesChapter 2 - Partnership Operations PROBLEM 6 and 8 With Worksheet 6.)sanjoeNo ratings yet

- CHAPTER 6 - Joint VentureDocument10 pagesCHAPTER 6 - Joint VentureminmenmNo ratings yet

- Dzaky Farhansyah - V1620034 - E5-19 - P5-8A - P5-7ADocument15 pagesDzaky Farhansyah - V1620034 - E5-19 - P5-8A - P5-7ADzaky FarhansyahNo ratings yet

- Revenue History ChartDocument2 pagesRevenue History ChartjsweigartNo ratings yet

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 34Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 34Malar SrirengarajahNo ratings yet

- Consolidation FP ExampleDocument4 pagesConsolidation FP ExampleSuryaRaoNo ratings yet

- Zabala Auto Supply Worksheet JANUARY 31, 2021 Unadjusted Trial Balance DebitDocument24 pagesZabala Auto Supply Worksheet JANUARY 31, 2021 Unadjusted Trial Balance DebitIphegenia DipoNo ratings yet

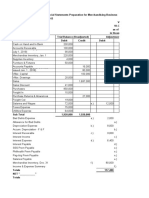

- DB6 - Worksheet & FS Prep For Merchandising BusinessDocument4 pagesDB6 - Worksheet & FS Prep For Merchandising BusinessArrianeNo ratings yet

- Test Bank 3 - Ia 3Document25 pagesTest Bank 3 - Ia 3jessaNo ratings yet

- Unit NDocument1 pageUnit NjharithpalaciosNo ratings yet

- 5.1 Kunci Jawaban Minggu 5 Lap Konsol 15 - 19 Feb 2016Document6 pages5.1 Kunci Jawaban Minggu 5 Lap Konsol 15 - 19 Feb 2016agustadivNo ratings yet

- FADM Assignment SolvedDocument12 pagesFADM Assignment SolvedAnujain JainNo ratings yet

- Restrictive Covenants - AfsaDocument10 pagesRestrictive Covenants - AfsaFrank A. Cusumano, Jr.No ratings yet

- Depreciated Replacement CostDocument7 pagesDepreciated Replacement CostOdetteDormanNo ratings yet

- Dda 2020Document32 pagesDda 2020GetGuidanceNo ratings yet

- Depreciation, Depletion and Amortization (Sas 9)Document3 pagesDepreciation, Depletion and Amortization (Sas 9)SadeeqNo ratings yet

- MAKAUT CIVIL Syllabus SEM 8Document9 pagesMAKAUT CIVIL Syllabus SEM 8u9830120786No ratings yet

- 14CFR, ICAO, EASA, PCAR, ATA Parts (Summary)Document11 pages14CFR, ICAO, EASA, PCAR, ATA Parts (Summary)therosefatherNo ratings yet

- Business Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketDocument13 pagesBusiness Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketJtm GarciaNo ratings yet

- HelpDocument5 pagesHelpMd Tushar Abdullah 024 ANo ratings yet

- Blood Angels Ref SheetsDocument4 pagesBlood Angels Ref SheetsAndrew ThomasNo ratings yet

- Travisa India ETA v5Document4 pagesTravisa India ETA v5Chamith KarunadharaNo ratings yet

- Financial Report: The Coca Cola Company: Ews/2021-10-27 - Coca - Cola - Reports - Continued - Momentum - and - Strong - 1040 PDFDocument3 pagesFinancial Report: The Coca Cola Company: Ews/2021-10-27 - Coca - Cola - Reports - Continued - Momentum - and - Strong - 1040 PDFDominic MuliNo ratings yet

- WFP AF Project Proposal The Gambia REV 04sept20 CleanDocument184 pagesWFP AF Project Proposal The Gambia REV 04sept20 CleanMahima DixitNo ratings yet

- An Introduction: by Rajiv SrivastavaDocument17 pagesAn Introduction: by Rajiv SrivastavaM M PanditNo ratings yet

- Facts:: Topic: Serious Misconduct and Wilfull DisobedienceDocument3 pagesFacts:: Topic: Serious Misconduct and Wilfull DisobedienceRochelle Othin Odsinada MarquesesNo ratings yet

- GOUP GO of 8 May 2013 For EM SchoolsDocument8 pagesGOUP GO of 8 May 2013 For EM SchoolsDevendra DamleNo ratings yet

- Variable Costing Case Part A SolutionDocument3 pagesVariable Costing Case Part A SolutionG, BNo ratings yet

- Thesis RecruitmentDocument62 pagesThesis Recruitmentmkarora122No ratings yet

- Christian Biography ResourcesDocument7 pagesChristian Biography ResourcesAzhar QureshiNo ratings yet

- Chapter 1 Introduction To Quranic Studies PDFDocument19 pagesChapter 1 Introduction To Quranic Studies PDFtaha zafar100% (3)

- Internship Report Mca Audit Report InternshipDocument33 pagesInternship Report Mca Audit Report InternshipJohnNo ratings yet

- Trifles Summary and Analysis of Part IDocument11 pagesTrifles Summary and Analysis of Part IJohn SmytheNo ratings yet

- ThesisDocument44 pagesThesisjagritiNo ratings yet

- Dam Water SensorDocument63 pagesDam Water SensorMuhammad RizalNo ratings yet

- 2 Quiz of mgt111 of bc090400798: Question # 1 of 20 Total Marks: 1Document14 pages2 Quiz of mgt111 of bc090400798: Question # 1 of 20 Total Marks: 1Muhammad ZeeshanNo ratings yet