You might also like

- Bain - Luxury Worldwide Market 2013Document46 pagesBain - Luxury Worldwide Market 2013pigcognitoNo ratings yet

- Bain - Luxury Goods Worldwide Market Study 2020 - Luxury and CoronavirusDocument30 pagesBain - Luxury Goods Worldwide Market Study 2020 - Luxury and CoronavirusIan TanNo ratings yet

- Bain Digest Luxury Goods Worldwide Market Study Fall Winter 2018Document36 pagesBain Digest Luxury Goods Worldwide Market Study Fall Winter 2018thestaybrownNo ratings yet

- Altagamma Research 2012Document46 pagesAltagamma Research 2012Nathaniel ShepardNo ratings yet

- Bain Luxury Study 9th Edition Oct 2010Document41 pagesBain Luxury Study 9th Edition Oct 2010Daniel Rusu100% (1)

- BAIN 2011 Luxury Market StudyDocument35 pagesBAIN 2011 Luxury Market StudyMichelleMNFNo ratings yet

- DigE DesignThinking WorkbookDocument3 pagesDigE DesignThinking WorkbookwaleedNo ratings yet

- Bain & Co.Document3 pagesBain & Co.rashmi shrivastavaNo ratings yet

- Charla12AGO2022 TelcoTRENDS Mckinsey 2023-2026CEDocument29 pagesCharla12AGO2022 TelcoTRENDS Mckinsey 2023-2026CEalejandro claroNo ratings yet

- 04 - Convert Symbols To Editable ShapesDocument6 pages04 - Convert Symbols To Editable ShapesSANJITNo ratings yet

- Ernst & Young Islamic Funds & Investments Report 2011Document50 pagesErnst & Young Islamic Funds & Investments Report 2011The_Banker100% (1)

- Delivering Productivity and Good Jobs: Why Industrial Strategy Must Focus On Fuman CapitalDocument14 pagesDelivering Productivity and Good Jobs: Why Industrial Strategy Must Focus On Fuman CapitalTera Allas100% (1)

- Mckinsey Report - COVID-19-Facts-and-Insights-March-25 PDFDocument57 pagesMckinsey Report - COVID-19-Facts-and-Insights-March-25 PDFUmang K100% (2)

- BCG ConsumatoreDocument37 pagesBCG ConsumatoreAdriano ManiscalcoNo ratings yet

- Oliver Wyman 2019 - The Brazilian Investment Landscape A New Era For Brazilian InvestorsDocument22 pagesOliver Wyman 2019 - The Brazilian Investment Landscape A New Era For Brazilian InvestorsThomaz FragaNo ratings yet

- Wenban MonitorDocument21 pagesWenban Monitoralex.nogueira396No ratings yet

- VP Strategy Marketing Operations in Austin TX Raleigh Durham NC Resume Joseph CarsanaroDocument2 pagesVP Strategy Marketing Operations in Austin TX Raleigh Durham NC Resume Joseph CarsanaroJosephCarsanaroNo ratings yet

- Organizational Velocity - Improving Speed, Efficiency & Effectiveness of Business SampleDocument24 pagesOrganizational Velocity - Improving Speed, Efficiency & Effectiveness of Business SampleSTRATICXNo ratings yet

- BCG COVID-19 Webinar For Malaysia - 8 Apr - vFINALDocument44 pagesBCG COVID-19 Webinar For Malaysia - 8 Apr - vFINALAlexander WinifredNo ratings yet

- Professor Low - PieSky Ventures (READ BY MAY 3)Document4 pagesProfessor Low - PieSky Ventures (READ BY MAY 3)erdal karatasNo ratings yet

- SKP SPI LCE ProjectSetUp VCLDocument43 pagesSKP SPI LCE ProjectSetUp VCLHugo CaviedesNo ratings yet

- Mekko Graphics Sample ChartsDocument47 pagesMekko Graphics Sample ChartsluizacoditaNo ratings yet

- The Net Zero Transition Report Final 25 Jan EsDocument64 pagesThe Net Zero Transition Report Final 25 Jan EsvineetaashNo ratings yet

- Price Execution How To Get Pricing Power Into Your Sales ForceDocument4 pagesPrice Execution How To Get Pricing Power Into Your Sales ForceasaadNo ratings yet

- Colombia Consumer Sentiment - FulldeckDocument34 pagesColombia Consumer Sentiment - FulldeckKatherine Uribe PeñaNo ratings yet

- Slide Templates: CEO-level Presentation Skills Course: Illustrative Slide Template CollectionDocument22 pagesSlide Templates: CEO-level Presentation Skills Course: Illustrative Slide Template CollectionVenketeshNo ratings yet

- Management Consulting: Book: The Mckinsey MindDocument26 pagesManagement Consulting: Book: The Mckinsey MindHoàng Tùng AnhNo ratings yet

- MGI Service Sector Productivity ReportDocument254 pagesMGI Service Sector Productivity ReportIoproprioioNo ratings yet

- 2017-11 AID Milan Fintech, How Financial Institutions McKinsey PDFDocument21 pages2017-11 AID Milan Fintech, How Financial Institutions McKinsey PDFHieu Nguyen MinhNo ratings yet

- EMC - Handout - Week 1 - AC - 2020-2021Document52 pagesEMC - Handout - Week 1 - AC - 2020-2021set_hitNo ratings yet

- Enduring LessonsDocument4 pagesEnduring LessonsPradeep RaghunathanNo ratings yet

- McKinsey Asia Marketing PracticeDocument7 pagesMcKinsey Asia Marketing PracticeAman RanaNo ratings yet

- Training: Problem Solving - The "8 X 3" Problem Solving MethodologyDocument16 pagesTraining: Problem Solving - The "8 X 3" Problem Solving Methodologysusheel kumarNo ratings yet

- Innovation MckinseyDocument23 pagesInnovation MckinseyVasco Duarte BarbosaNo ratings yet

- Indonesia e Conomy Sea 2021 ReportDocument17 pagesIndonesia e Conomy Sea 2021 ReportEep Saefulloh FatahNo ratings yet

- ZF Telco Conference v1Document30 pagesZF Telco Conference v1imatacheNo ratings yet

- Q&Me - Vietnam Retail Store (Modern Trade) Status 2019Document30 pagesQ&Me - Vietnam Retail Store (Modern Trade) Status 2019Tan LeNo ratings yet

- Instruction Manual: 1. Set Up The Schedule TableDocument3 pagesInstruction Manual: 1. Set Up The Schedule TableRadoslav RobertNo ratings yet

- Everyday Life and Activities Are Resuming in China: Confirmed New Cases Per Day (Thousands)Document10 pagesEveryday Life and Activities Are Resuming in China: Confirmed New Cases Per Day (Thousands)Pankaj MehraNo ratings yet

- Value CreationDocument36 pagesValue CreationKamalapati BeheraNo ratings yet

- Senior Manager Internal Audit in Boston MA Providence RI Resume Edward NolanDocument3 pagesSenior Manager Internal Audit in Boston MA Providence RI Resume Edward NolanEdwardNolanNo ratings yet

- Holidays List 2019Document8 pagesHolidays List 2019SR RaoNo ratings yet

- Parker's Biscuits, Inc.: Venturing Into China: Harvard Business School 9-697-056Document18 pagesParker's Biscuits, Inc.: Venturing Into China: Harvard Business School 9-697-056Shaan RoyNo ratings yet

- The Great Reskilling - CourseraDocument40 pagesThe Great Reskilling - CourseraHichem AkroutNo ratings yet

- How To Choose A Capital Structure - Navigating The Debt Equity DecisionDocument12 pagesHow To Choose A Capital Structure - Navigating The Debt Equity Decisionresat gürNo ratings yet

- Mckinsey China Consumer Report 2021Document158 pagesMckinsey China Consumer Report 2021brianNo ratings yet

- Economic FluctuationsDocument49 pagesEconomic Fluctuationsswayam anandNo ratings yet

- Keyboard Shortcuts CheatsheetDocument2 pagesKeyboard Shortcuts CheatsheetMuskanDodejaNo ratings yet

- Cu01 PDF EngDocument9 pagesCu01 PDF EngroxanaNo ratings yet

- Presentation of Financial Information Course PresentationDocument22 pagesPresentation of Financial Information Course PresentationSaviour Kandolo37No ratings yet

- BCG Pricing Playbook For CPG Companies Amid Inflationary Pressure July 2021Document11 pagesBCG Pricing Playbook For CPG Companies Amid Inflationary Pressure July 2021Saksham KumarNo ratings yet

- Strategy FrameworksDocument14 pagesStrategy FrameworksTanmay Shubham PantNo ratings yet

- Global Chemical 2030 - Roland Berger - 2011Document16 pagesGlobal Chemical 2030 - Roland Berger - 2011xav9238No ratings yet

- McKinsey CovidDocument24 pagesMcKinsey CovidAarati Krishnan100% (6)

- Greater China Smartphone Sector 130904Document52 pagesGreater China Smartphone Sector 130904BLBVORTEXNo ratings yet

- Blockbuster Script For The New DecadeDocument78 pagesBlockbuster Script For The New DecadePankaj PandeyNo ratings yet

- Product Life Cycles VinodDocument45 pagesProduct Life Cycles VinodVinod JoshiNo ratings yet

- McKinsey China Luxury Report 2019 EnglishDocument29 pagesMcKinsey China Luxury Report 2019 EnglishTung NgoNo ratings yet

- BTTM 707 Tourism ProductDocument114 pagesBTTM 707 Tourism ProductSaurabh ShahiNo ratings yet

- Bainstudy Luxurygoodsworldwidemarketstudy Spring20201120updateDocument18 pagesBainstudy Luxurygoodsworldwidemarketstudy Spring20201120updateRupsayar DasNo ratings yet

- Syndicates For LeadsDocument8 pagesSyndicates For Leadsboka987No ratings yet

- Altagamma Bain Worldwide Market Monitor - Update 2019 PDFDocument15 pagesAltagamma Bain Worldwide Market Monitor - Update 2019 PDFHaider RazaNo ratings yet

- Why Assisted' E-Commerce - LinkedInDocument5 pagesWhy Assisted' E-Commerce - LinkedInHaider RazaNo ratings yet

- CB Insights Banks in Fintech BriefingDocument60 pagesCB Insights Banks in Fintech BriefingHaider RazaNo ratings yet

- The Mechanics of AngelList Syndicates - by David E. WeeklyDocument13 pagesThe Mechanics of AngelList Syndicates - by David E. WeeklyHaider RazaNo ratings yet

- All3 Business Vs System Use Cases v1 9Document135 pagesAll3 Business Vs System Use Cases v1 9Haider RazaNo ratings yet

- Customer Journey MapDocument1 pageCustomer Journey MapHaider RazaNo ratings yet

- All3 Business Vs System Use Cases v1 9 PDFDocument15 pagesAll3 Business Vs System Use Cases v1 9 PDFHaider RazaNo ratings yet

- Eco Design Proposal v1Document6 pagesEco Design Proposal v1Haider RazaNo ratings yet

- Credits: A New Generation of BlockchainDocument21 pagesCredits: A New Generation of BlockchainHaider RazaNo ratings yet

- Singularities and The Sociological Imagination: On Nathalie Heinich's Sociology of The ArtsDocument4 pagesSingularities and The Sociological Imagination: On Nathalie Heinich's Sociology of The ArtsHaider RazaNo ratings yet

- UHD60-M-en-US ManualDocument61 pagesUHD60-M-en-US ManualTaesun KangNo ratings yet

- UHD60 M en USDocument84 pagesUHD60 M en USHaider RazaNo ratings yet

- Paimona BeedayDocument1 pagePaimona BeedayHaider RazaNo ratings yet

- How Happiness Affects ChoiceDocument15 pagesHow Happiness Affects ChoiceHaider RazaNo ratings yet

- Workcoinen White PaperDocument22 pagesWorkcoinen White PaperHaider RazaNo ratings yet

- Fast-Forwarding To A Future of On-Demand Urban Air TransportationDocument98 pagesFast-Forwarding To A Future of On-Demand Urban Air TransportationTri RamadhaniNo ratings yet

- How To Be An Innovation RockstarDocument40 pagesHow To Be An Innovation RockstarHaider Raza100% (1)

- Infographic Luxury Travel Amadeus Media SolutionsDocument1 pageInfographic Luxury Travel Amadeus Media SolutionsHaider RazaNo ratings yet

- SDO Imus City LeaP ABM Principles of Marketing 1st Quarter Week 2Document4 pagesSDO Imus City LeaP ABM Principles of Marketing 1st Quarter Week 2Aprilyn HernandezNo ratings yet

- The RSI Scalping StrategyDocument30 pagesThe RSI Scalping StrategyDavid Gordon83% (23)

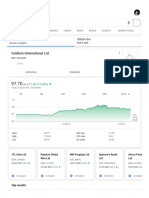

- Goldiam Share - Google SearchDocument5 pagesGoldiam Share - Google SearchDudheshwar SinghNo ratings yet

- Viral Marketing and Social Media StatisticsDocument16 pagesViral Marketing and Social Media Statisticsosama haseebNo ratings yet

- Chart Analysis: by Sunny JainDocument26 pagesChart Analysis: by Sunny JainShubh mangalNo ratings yet

- E-Book - Retail Marketing Management - Principles & Practice-Pearson (2015) - Helen Goworek PDFDocument369 pagesE-Book - Retail Marketing Management - Principles & Practice-Pearson (2015) - Helen Goworek PDFJerrielle CastroNo ratings yet

- Introduction To Sales Management: by Prof. V KrishnamohanDocument20 pagesIntroduction To Sales Management: by Prof. V KrishnamohanKrishnamohan VaddadiNo ratings yet

- Risk and ReturnDocument55 pagesRisk and ReturnShukri Omar AliNo ratings yet

- Petrobras of Brazil and The CostDocument3 pagesPetrobras of Brazil and The CostIoana PunctNo ratings yet

- A-Level Economics - The Price System and The Micro Economy (Contestable Market Theory)Document27 pagesA-Level Economics - The Price System and The Micro Economy (Contestable Market Theory)Hyacinth ChimundaNo ratings yet

- Business Economics AssignmentDocument7 pagesBusiness Economics AssignmentDEAN JASPERNo ratings yet

- Economics Higher Level Paper 3: Instructions To CandidatesDocument6 pagesEconomics Higher Level Paper 3: Instructions To CandidatesAndres Krauss100% (1)

- Effect of Foreign Institutional Investors On Corporate Board Attributes A Literature ReviewDocument7 pagesEffect of Foreign Institutional Investors On Corporate Board Attributes A Literature ReviewRiya CassendraNo ratings yet

- EFF CHP 2 - MVSIR - ChartsDocument11 pagesEFF CHP 2 - MVSIR - ChartsMayank RajputNo ratings yet

- Project Report On DERIVATIVESDocument69 pagesProject Report On DERIVATIVESRaghavendra yadav KM100% (2)

- The Rise and Fall of The Neoliberal Order America and The World in The Free Market Era Gary Gerstle Full ChapterDocument67 pagesThe Rise and Fall of The Neoliberal Order America and The World in The Free Market Era Gary Gerstle Full Chapterjamie.johnson157100% (5)

- FINA3080 Assignment 1Document2 pagesFINA3080 Assignment 1Koon Sing ChanNo ratings yet

- JAIIB PPB Sample Questions by Murugan-May 19 Exams PDFDocument549 pagesJAIIB PPB Sample Questions by Murugan-May 19 Exams PDFOruganti DivyaNo ratings yet

- Shuats Hostel - Fee Online PaymentDocument1 pageShuats Hostel - Fee Online PaymentSyed Mubashshir AlamNo ratings yet

- CBM ReviewerDocument6 pagesCBM ReviewerJersey SNo ratings yet

- Worried About The Fall in Gold Price?: Ashish Ranawade, Head of Products, Emkay Global. Annexure: Gold Price ChartDocument1 pageWorried About The Fall in Gold Price?: Ashish Ranawade, Head of Products, Emkay Global. Annexure: Gold Price ChartspeedenquiryNo ratings yet

- PPE Investments Working PaperDocument15 pagesPPE Investments Working PaperMarriel Fate CullanoNo ratings yet

- Passing Package PDFDocument10 pagesPassing Package PDFAddds Muhammmed100% (1)

- Soap Industries (FMCG)Document66 pagesSoap Industries (FMCG)Bhavin Patel55% (11)

- Portfolio AnalysisDocument40 pagesPortfolio AnalysisAryan GuptaNo ratings yet

- SWOT Analysis Textile IndustryDocument23 pagesSWOT Analysis Textile Industrydumitrescu viorelNo ratings yet

- 01 Introduction Principles of MarketingDocument15 pages01 Introduction Principles of MarketingGracely Calliope De JuanNo ratings yet

- The Multichannel Challenge at NatDocument18 pagesThe Multichannel Challenge at NatGianfranco GardellaNo ratings yet

- FinMod 2022-2023 Tutorial Exercise + Answers Week 5Document36 pagesFinMod 2022-2023 Tutorial Exercise + Answers Week 5jjpasemperNo ratings yet

- E-Books - AS 13 Accounting For InvestmentsDocument32 pagesE-Books - AS 13 Accounting For InvestmentssmartshivenduNo ratings yet

- Prisoners of Geography: Ten Maps That Explain Everything About the WorldFrom EverandPrisoners of Geography: Ten Maps That Explain Everything About the WorldRating: 4.5 out of 5 stars4.5/5 (1145)

- The Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaFrom EverandThe Shadow War: Inside Russia's and China's Secret Operations to Defeat AmericaRating: 4.5 out of 5 stars4.5/5 (12)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (227)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (8)

- Reagan at Reykjavik: Forty-Eight Hours That Ended the Cold WarFrom EverandReagan at Reykjavik: Forty-Eight Hours That Ended the Cold WarRating: 4 out of 5 stars4/5 (4)

- Age of Revolutions: Progress and Backlash from 1600 to the PresentFrom EverandAge of Revolutions: Progress and Backlash from 1600 to the PresentRating: 4.5 out of 5 stars4.5/5 (6)

- Son of Hamas: A Gripping Account of Terror, Betrayal, Political Intrigue, and Unthinkable ChoicesFrom EverandSon of Hamas: A Gripping Account of Terror, Betrayal, Political Intrigue, and Unthinkable ChoicesRating: 4.5 out of 5 stars4.5/5 (498)

- How States Think: The Rationality of Foreign PolicyFrom EverandHow States Think: The Rationality of Foreign PolicyRating: 5 out of 5 stars5/5 (7)

- The Power of Geography: Ten Maps that Reveal the Future of Our WorldFrom EverandThe Power of Geography: Ten Maps that Reveal the Future of Our WorldRating: 4.5 out of 5 stars4.5/5 (54)

- Can We Talk About Israel?: A Guide for the Curious, Confused, and ConflictedFrom EverandCan We Talk About Israel?: A Guide for the Curious, Confused, and ConflictedRating: 5 out of 5 stars5/5 (5)

- The Tragic Mind: Fear, Fate, and the Burden of PowerFrom EverandThe Tragic Mind: Fear, Fate, and the Burden of PowerRating: 4 out of 5 stars4/5 (14)

- Never Give an Inch: Fighting for the America I LoveFrom EverandNever Give an Inch: Fighting for the America I LoveRating: 4 out of 5 stars4/5 (10)

- Four Battlegrounds: Power in the Age of Artificial IntelligenceFrom EverandFour Battlegrounds: Power in the Age of Artificial IntelligenceRating: 5 out of 5 stars5/5 (5)

- The Devil's Chessboard: Allen Dulles, the CIA, and the Rise of America's Secret GovernmentFrom EverandThe Devil's Chessboard: Allen Dulles, the CIA, and the Rise of America's Secret GovernmentRating: 4.5 out of 5 stars4.5/5 (27)

- The Future of Geography: How the Competition in Space Will Change Our WorldFrom EverandThe Future of Geography: How the Competition in Space Will Change Our WorldRating: 4 out of 5 stars4/5 (5)

- International Relations: An IntroductionFrom EverandInternational Relations: An IntroductionRating: 4 out of 5 stars4/5 (2)

- Epicenter: Why the Current Rumblings in the Middle East Will Change Your FutureFrom EverandEpicenter: Why the Current Rumblings in the Middle East Will Change Your FutureRating: 4 out of 5 stars4/5 (22)

- Pitfall: The Race to Mine the World’s Most Vulnerable PlacesFrom EverandPitfall: The Race to Mine the World’s Most Vulnerable PlacesNo ratings yet

- The Economic Weapon: The Rise of Sanctions as a Tool of Modern WarFrom EverandThe Economic Weapon: The Rise of Sanctions as a Tool of Modern WarRating: 4.5 out of 5 stars4.5/5 (4)

- Overreach: The Inside Story of Putin’s War Against UkraineFrom EverandOverreach: The Inside Story of Putin’s War Against UkraineRating: 4.5 out of 5 stars4.5/5 (29)

- Crazy Like Us: The Globalization of the American PsycheFrom EverandCrazy Like Us: The Globalization of the American PsycheRating: 4.5 out of 5 stars4.5/5 (16)

- Except for Palestine: The Limits of Progressive PoliticsFrom EverandExcept for Palestine: The Limits of Progressive PoliticsRating: 4.5 out of 5 stars4.5/5 (52)

- Chip War: The Fight for the World's Most Critical TechnologyFrom EverandChip War: The Fight for the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (82)

- Freedom is a Constant Struggle: Ferguson, Palestine, and the Foundations of a MovementFrom EverandFreedom is a Constant Struggle: Ferguson, Palestine, and the Foundations of a MovementRating: 4.5 out of 5 stars4.5/5 (566)