You might also like

- Cotton Science and Processing Technology: Gene, Ginning, Garment and Green RecyclingFrom EverandCotton Science and Processing Technology: Gene, Ginning, Garment and Green RecyclingHua WangNo ratings yet

- Sustainable Innovations in Textile Chemical ProcessesFrom EverandSustainable Innovations in Textile Chemical ProcessesNo ratings yet

- Indian Textile Industry - UnlockedDocument15 pagesIndian Textile Industry - UnlockedHarish BullsNo ratings yet

- India's Textile Industry: An Overview of Major Players and ExportsDocument0 pagesIndia's Textile Industry: An Overview of Major Players and Exportsdianty_marienkafergsNo ratings yet

- Textile Industry in IndiaDocument0 pagesTextile Industry in IndiashanujssNo ratings yet

- Textile Industry in India PDFDocument13 pagesTextile Industry in India PDFarunNo ratings yet

- Textile Industry in IndiaDocument15 pagesTextile Industry in IndiaKannan Krishnamurthy50% (2)

- Bombay Dyeing: History and Products of India's Leading Textile CompanyDocument2 pagesBombay Dyeing: History and Products of India's Leading Textile CompanyVikrant Singh0% (1)

- Garment IndustryDocument37 pagesGarment IndustryPuneet TandonNo ratings yet

- Leshark Global LLP - InternshipDocument38 pagesLeshark Global LLP - InternshipSowmya LakshmiNo ratings yet

- The Garment Industry in India Has One of the Most Illustrious and Venerabl_20240311_110426_0000Document20 pagesThe Garment Industry in India Has One of the Most Illustrious and Venerabl_20240311_110426_0000Heera SriganeshNo ratings yet

- Raymond Group's Transformation into a Global ConglomerateDocument35 pagesRaymond Group's Transformation into a Global ConglomerateAmisha SinghNo ratings yet

- Raymond Group's Evolution into a Global ConglomerateDocument33 pagesRaymond Group's Evolution into a Global ConglomerateRavibalan50% (4)

- Improving Jacket Line Quality at Raymond's Silver Spark LtdDocument2 pagesImproving Jacket Line Quality at Raymond's Silver Spark LtdAashish KukretiNo ratings yet

- Arvind ReportDocument17 pagesArvind Reportaneri31791100% (1)

- Mahendra R & TDocument73 pagesMahendra R & THarshith ShettyNo ratings yet

- Arvind Mills Company ProfileDocument23 pagesArvind Mills Company ProfileBharath Chandra B KNo ratings yet

- A Project Report On A Study On Working Capital Management in Vardhaman Textile LTDDocument22 pagesA Project Report On A Study On Working Capital Management in Vardhaman Textile LTDDeepika GNo ratings yet

- Arvind Mills AnalysisDocument18 pagesArvind Mills AnalysisAnup AgarwalNo ratings yet

- Chapter - 1: Introduction of Textile IndustryDocument68 pagesChapter - 1: Introduction of Textile Industrydeep bajwaNo ratings yet

- Lalbhai Group - ArvindDocument4 pagesLalbhai Group - Arvindvinoth_17588No ratings yet

- Textile IndustryDocument8 pagesTextile IndustryAarav AggarwalNo ratings yet

- Comprehensive Study of Textile From Fiber To FashionDocument10 pagesComprehensive Study of Textile From Fiber To Fashiondeepakshi.inNo ratings yet

- Ibis Textiles Directory 2023 SampleDocument13 pagesIbis Textiles Directory 2023 Samplesujan mehtaNo ratings yet

- Indian Textile IndustryDocument21 pagesIndian Textile IndustryPrateek MehariaNo ratings yet

- Arvind Mills Restructuring PlanDocument21 pagesArvind Mills Restructuring PlanPrarrthona Pal Chowdhury50% (2)

- MAP Report For MBADocument57 pagesMAP Report For MBAMaulik TankNo ratings yet

- Final Report of AnugrahaDocument35 pagesFinal Report of AnugrahaPavithra SankolNo ratings yet

- Vardhman ReportDocument18 pagesVardhman ReportRaj Kumar100% (1)

- 1.1introduction To The StudyDocument74 pages1.1introduction To The StudysathishNo ratings yet

- AHMEDABAD UNIVERSITY (AU) H.L. INSTITUTE OF COMMERCE (HLIC) F.Y. B.Com-5. Project Assignment For Fundamental Of Accountancy Topic- Textile GroupDocument14 pagesAHMEDABAD UNIVERSITY (AU) H.L. INSTITUTE OF COMMERCE (HLIC) F.Y. B.Com-5. Project Assignment For Fundamental Of Accountancy Topic- Textile GroupNishit PatelNo ratings yet

- RN 15 Entrepreneurship DevelopmentDocument6 pagesRN 15 Entrepreneurship DevelopmentShane McmillanNo ratings yet

- JacketsDocument75 pagesJacketsraghvendra2208No ratings yet

- Neva Marketing ProjectDocument92 pagesNeva Marketing ProjectujranchamanNo ratings yet

- Introduction To Textile IndustryDocument75 pagesIntroduction To Textile IndustryPratima JainNo ratings yet

- NandyDocument10 pagesNandyNandhini PriyaNo ratings yet

- Navdeep oSWAL FinalDocument54 pagesNavdeep oSWAL FinalLovlesh RubyNo ratings yet

- Inplant Training in Kandhan KnitssDocument51 pagesInplant Training in Kandhan KnitssgunasekaranmbaNo ratings yet

- UCO Raymond Denim HoldingDocument7 pagesUCO Raymond Denim Holdingantonypio123No ratings yet

- Indian Textile and Nahar SpinningDocument25 pagesIndian Textile and Nahar SpinningrinekshjNo ratings yet

- Positioning Strategy Adopted by Raymond Ltd.Document46 pagesPositioning Strategy Adopted by Raymond Ltd.Priyanka Sharma57% (7)

- Group No 12 Fip ReportDocument10 pagesGroup No 12 Fip ReportHimanshu AgrawalNo ratings yet

- India's Textile Industry & Raymond's GrowthDocument3 pagesIndia's Textile Industry & Raymond's Growth551VIJAYA ADITYA ERRABATINo ratings yet

- Inventory Management JapanDocument4 pagesInventory Management JapanSURUCHI KUMARINo ratings yet

- Textile Industry in IndiaDocument7 pagesTextile Industry in IndiaSandeep YadavNo ratings yet

- Arvind MillsDocument9 pagesArvind MillsPradeep Kumar PandeyNo ratings yet

- Himatsingka Seide1 PDFDocument44 pagesHimatsingka Seide1 PDFVishwas Kumar100% (2)

- Textile Industry in SuratDocument70 pagesTextile Industry in SuratgoswamiakashNo ratings yet

- OM - CIA-1 (GROUP - 1) ReportDocument9 pagesOM - CIA-1 (GROUP - 1) ReportRadhika SinghalNo ratings yet

- Textile Industry: Submitted By: Unnati PatelDocument31 pagesTextile Industry: Submitted By: Unnati Patelpalak rathoreNo ratings yet

- Pavit Worldwide Private Limited Company: Industry ProfileDocument66 pagesPavit Worldwide Private Limited Company: Industry ProfilemazoahrahselNo ratings yet

- Current Facts On Indian Textile Industry: Page - 1Document54 pagesCurrent Facts On Indian Textile Industry: Page - 1bccmehtaNo ratings yet

- TextileDocument11 pagesTextileعبداللہ یاسر بلوچNo ratings yet

- Chapter-1: Involvement of State AgriculturalDocument42 pagesChapter-1: Involvement of State AgriculturalMohankumar MohankumarNo ratings yet

- TIR Vardhman, Budhni (29 Dec 2020)Document36 pagesTIR Vardhman, Budhni (29 Dec 2020)Keshav AnandNo ratings yet

- Amaravathi 16 PointsdDocument16 pagesAmaravathi 16 PointsdSakhamuri Ram'sNo ratings yet

- OS ReportDocument72 pagesOS ReportPrasanth C NairNo ratings yet

- My ProjectDocument116 pagesMy ProjectLaxmannathsidhNo ratings yet

- Textiles For Commercial, Industrial, and Domestic Arts Schools; Also Adapted to Those Engaged in Wholesale and Retail Dry Goods, Wool, Cotton, and Dressmaker's TradesFrom EverandTextiles For Commercial, Industrial, and Domestic Arts Schools; Also Adapted to Those Engaged in Wholesale and Retail Dry Goods, Wool, Cotton, and Dressmaker's TradesRating: 4 out of 5 stars4/5 (1)

- Union Budget 2011-12: HighlightsDocument14 pagesUnion Budget 2011-12: HighlightsNDTVNo ratings yet

- Entrepreneurship Concept & DefinitionDocument5 pagesEntrepreneurship Concept & DefinitionanoopguptNo ratings yet

- Book 1Document16 pagesBook 1Gaurav PoddarNo ratings yet

- HRM TerminologyDocument2 pagesHRM TerminologyGaurav PoddarNo ratings yet

- IT ReportDocument2 pagesIT ReportGaurav PoddarNo ratings yet

- 7 Eleven Store Nantun District - Google SearchDocument1 page7 Eleven Store Nantun District - Google SearchArleen MallillinNo ratings yet

- Survey of Portland Cement Consumption by of Portland Cement Consumption 1stDocument45 pagesSurvey of Portland Cement Consumption by of Portland Cement Consumption 1stHimerozNo ratings yet

- Contracts II AssignmentDocument16 pagesContracts II AssignmentIsha PuthettuNo ratings yet

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- The Following Information Is Available To Reconcile Style Co SDocument2 pagesThe Following Information Is Available To Reconcile Style Co SAmit PandeyNo ratings yet

- CRT 3rd Year NewDocument232 pagesCRT 3rd Year NewAkshat agrawalNo ratings yet

- Developing Lean and Agile Automotive Suppliers ManDocument12 pagesDeveloping Lean and Agile Automotive Suppliers ManLia Nurul MulyaniNo ratings yet

- Urban MarketplaceDocument20 pagesUrban MarketplaceMae LafortezaNo ratings yet

- PPM02 Project Portfolio Prioritization Matrix - AdvancedDocument5 pagesPPM02 Project Portfolio Prioritization Matrix - AdvancedHazqanNo ratings yet

- FMCSA Rules on Marking Commercial Motor VehiclesDocument3 pagesFMCSA Rules on Marking Commercial Motor VehiclesfreeNo ratings yet

- Marcopper Mining CorpDocument7 pagesMarcopper Mining CorpChristine Ivy Delos SantosNo ratings yet

- Real-Estate Investor's Psychology: Heuristics and Prospect FactorsDocument6 pagesReal-Estate Investor's Psychology: Heuristics and Prospect Factors03217925346No ratings yet

- Technical Appraisal: Unit 5Document16 pagesTechnical Appraisal: Unit 5DIPAKNo ratings yet

- ABS ISPS Company - Vessel Audit ChecklistDocument1 pageABS ISPS Company - Vessel Audit ChecklistredchaozNo ratings yet

- Implementing RBI and RCM to Improve Asset ReliabilityDocument56 pagesImplementing RBI and RCM to Improve Asset ReliabilityKareem RasmyNo ratings yet

- Top 20 Customer Relationship Manager Interview QuestionsDocument8 pagesTop 20 Customer Relationship Manager Interview QuestionsYifredewNo ratings yet

- Andhra Pradesh Board Fee Payment FormDocument1 pageAndhra Pradesh Board Fee Payment FormM JEEVARATHNAM NAIDUNo ratings yet

- 30 Free Leed Ap BD+C Sample QuestionsDocument23 pages30 Free Leed Ap BD+C Sample QuestionsSubhranshu PandaNo ratings yet

- Power Purchase AgreementDocument22 pagesPower Purchase Agreementdark webNo ratings yet

- Diamond Doctor Suit Against ManookianDocument41 pagesDiamond Doctor Suit Against ManookianThe Dallas Morning News100% (1)

- Jollisavers Meals TV Ad DeconstructedDocument4 pagesJollisavers Meals TV Ad DeconstructedMa. Rhona Faye MedesNo ratings yet

- TQM in Graduate Teacher EducationDocument38 pagesTQM in Graduate Teacher Educationjuditha b. PaunillanNo ratings yet

- Zain Ufone Best 1 Strategic Management ProjectDocument50 pagesZain Ufone Best 1 Strategic Management Projectzain_lion2009372280% (10)

- Kajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in WorldDocument10 pagesKajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in Worldapi-556903190No ratings yet

- Chapter 1 KTQTDocument38 pagesChapter 1 KTQTHà LiênNo ratings yet

- Software Developement Life CycleDocument21 pagesSoftware Developement Life CycleJAI THAPANo ratings yet

- Solved MAT 2002 Paper With SolutionsDocument59 pagesSolved MAT 2002 Paper With SolutionsAnshuman NarangNo ratings yet

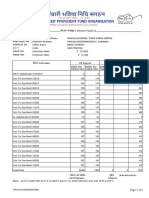

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Final Ruckus ProposalDocument29 pagesFinal Ruckus Proposalapi-609740598No ratings yet