You might also like

- The Beginners Bible Coloring Book by JPR504Document37 pagesThe Beginners Bible Coloring Book by JPR504Ernesto Carmona Parra100% (1)

- Senior Assassins 2015 Official Rulebook: Welcome To The Game, AssassinsDocument5 pagesSenior Assassins 2015 Official Rulebook: Welcome To The Game, Assassinsapi-280221810No ratings yet

- Ruhi Agrawal Assignment (Banking)Document32 pagesRuhi Agrawal Assignment (Banking)Shraddha GawadeNo ratings yet

- CRR & SLR and Computation - PPTX BVB 204Document20 pagesCRR & SLR and Computation - PPTX BVB 204679shrishti SinghNo ratings yet

- Role of CRR and SLRDocument9 pagesRole of CRR and SLRVineeta Malan50% (2)

- Indian Economy Part-II in EnglishDocument116 pagesIndian Economy Part-II in EnglishWTF NewsNo ratings yet

- Monetary Management REPORTDocument12 pagesMonetary Management REPORTRajat MishraNo ratings yet

- Monetary Policy - Eco ProjectDocument8 pagesMonetary Policy - Eco Projectnandanaa06No ratings yet

- Monetary PolicyDocument18 pagesMonetary PolicyTanmay JainNo ratings yet

- Statutory Liquidity RatioDocument2 pagesStatutory Liquidity RatioRamNo ratings yet

- Financial Sector Reforms in India Since 1991Document11 pagesFinancial Sector Reforms in India Since 1991AMAN KUMAR SINGHNo ratings yet

- ACFrOgAIPqeduC6xn4YwZGZULnMkaBXsvoe10JiZ-5Gnt4qvbUJXSXRHFCv6h5nRQP2TLyrabhEZf-59scu6F351RDSAZxite5CfZhqyGduD7KdgdhzTwKMK4QoI9hB6T8PAPD3ipWT0lTuM-y5husUPIYygwxVMlMXT-K2USA==Document12 pagesACFrOgAIPqeduC6xn4YwZGZULnMkaBXsvoe10JiZ-5Gnt4qvbUJXSXRHFCv6h5nRQP2TLyrabhEZf-59scu6F351RDSAZxite5CfZhqyGduD7KdgdhzTwKMK4QoI9hB6T8PAPD3ipWT0lTuM-y5husUPIYygwxVMlMXT-K2USA==Manleen KaurNo ratings yet

- Value and Formula: Statutory Liquidity Ratio Is The Amount of Liquid Assets Such As Precious Metals (Gold) or OtherDocument4 pagesValue and Formula: Statutory Liquidity Ratio Is The Amount of Liquid Assets Such As Precious Metals (Gold) or OthernandiniNo ratings yet

- Genral Terms of EconomiczDocument3 pagesGenral Terms of Economiczreds32001No ratings yet

- Monetary Policy: Reserve Bank of IndiaDocument5 pagesMonetary Policy: Reserve Bank of IndiaRicky RoyNo ratings yet

- Banking, Financial Services and Insurance: Unnati Sector PresentationDocument48 pagesBanking, Financial Services and Insurance: Unnati Sector PresentationPradeep VarshneyNo ratings yet

- 2631IIBF Vision January 2013Document8 pages2631IIBF Vision January 2013Sukanta DasNo ratings yet

- Monetary PolicyDocument3 pagesMonetary PolicymbapritiNo ratings yet

- Banking SectorDocument2 pagesBanking SectorAtharva SisodiyaNo ratings yet

- RBI's Unprecedented StepsDocument7 pagesRBI's Unprecedented StepsRakshita AsatiNo ratings yet

- Quantitative ToolsDocument14 pagesQuantitative Tools9439223514pNo ratings yet

- Indian financial reforms focused on banking sectorDocument10 pagesIndian financial reforms focused on banking sectornagendra yanamalaNo ratings yet

- Monetary PolicyDocument18 pagesMonetary PolicySarada NagNo ratings yet

- FIM Done PDFDocument244 pagesFIM Done PDFsNo ratings yet

- RBI Monetary Policy Explained in 40 CharactersDocument18 pagesRBI Monetary Policy Explained in 40 CharactersAshish ShuklaNo ratings yet

- Banking Sector Reforms in IndiaDocument8 pagesBanking Sector Reforms in IndiaJashan Singh GillNo ratings yet

- Assignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryDocument9 pagesAssignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryRohit VermaNo ratings yet

- RBI's LTRO and TLTRO ExplainedDocument2 pagesRBI's LTRO and TLTRO ExplainedSanjana KrishnakumarNo ratings yet

- Why Interest Rates ChangeDocument4 pagesWhy Interest Rates Changekirang gandhiNo ratings yet

- CA - 01-10 May 2022Document36 pagesCA - 01-10 May 2022Tushar SahaNo ratings yet

- 5 MayDocument113 pages5 MayShubhendu VermaNo ratings yet

- How Is CRR Used As A Tool of Credit ControlDocument14 pagesHow Is CRR Used As A Tool of Credit ControlHimangini SinghNo ratings yet

- Cash Reserve Ratio: Economics Project by Ayush Dadawala and Suradnya PatilDocument14 pagesCash Reserve Ratio: Economics Project by Ayush Dadawala and Suradnya PatilSuradnya PatilNo ratings yet

- Banking AwarenessDocument6 pagesBanking AwarenessYashJainNo ratings yet

- (A) Quantitative Instruments or General ToolsDocument5 pages(A) Quantitative Instruments or General ToolsSiddh Shah ⎝⎝⏠⏝⏠⎠⎠No ratings yet

- Financial IndicatorsDocument20 pagesFinancial Indicatorsmajid_khan_4No ratings yet

- U I S M: Pdate On Ndian Ecuritisation ArketDocument9 pagesU I S M: Pdate On Ndian Ecuritisation ArketAbhishek SinghNo ratings yet

- Monetary Policy of India - WikipediaDocument4 pagesMonetary Policy of India - Wikipediaambikesh008No ratings yet

- Monetary PolicyDocument23 pagesMonetary PolicyPooja JainNo ratings yet

- 1939IIBF Vision April 2012Document8 pages1939IIBF Vision April 2012Shambhu KumarNo ratings yet

- Presentation On NPA Problem: by Anshika AditiDocument18 pagesPresentation On NPA Problem: by Anshika AditiAnshika SharmaNo ratings yet

- Weekly Economic Round Up 39Document14 pagesWeekly Economic Round Up 39Mana PlanetNo ratings yet

- Assignment FinancialSectorReforms1991Document4 pagesAssignment FinancialSectorReforms1991Swathi SriNo ratings yet

- 4163IIBF Vision March 2015Document8 pages4163IIBF Vision March 2015Madhumita PandeyNo ratings yet

- RBI's Monetary Policy Objectives and ToolsDocument6 pagesRBI's Monetary Policy Objectives and ToolspundirsandeepNo ratings yet

- Use Unclaimed DepositsDocument5 pagesUse Unclaimed DepositsalkjghNo ratings yet

- Monetary Policy PresentationDocument22 pagesMonetary Policy Presentationanon_792919970No ratings yet

- Notes On Monetary & Credit Policy of RBIDocument5 pagesNotes On Monetary & Credit Policy of RBIjophythomasNo ratings yet

- Quantitative instruments used to control inflationDocument4 pagesQuantitative instruments used to control inflationanvesha khillarNo ratings yet

- RBI Credit Authorization SchemeDocument6 pagesRBI Credit Authorization SchemeOngwang KonyakNo ratings yet

- Monthly Digest November 2023 Eng 29Document24 pagesMonthly Digest November 2023 Eng 29shivam feb414No ratings yet

- FINANCE CURRENT MARCH WEEK 4 Lyst6283Document23 pagesFINANCE CURRENT MARCH WEEK 4 Lyst6283hero66No ratings yet

- 6 Banking and Financial ServicesDocument5 pages6 Banking and Financial ServicesSatish MehtaNo ratings yet

- Treasury ManagementDocument40 pagesTreasury ManagementNiraj DesaiNo ratings yet

- Monetary Policy of IndiaDocument34 pagesMonetary Policy of IndiaJhankar MishraNo ratings yet

- Sample Phase I Ga NotesDocument8 pagesSample Phase I Ga NotesSAI CHARAN VNo ratings yet

- What Is Monetary PolicyDocument5 pagesWhat Is Monetary PolicyBhagat DeepakNo ratings yet

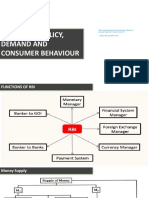

- Monetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreDocument23 pagesMonetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreBhavya NarangNo ratings yet

- Debt Market Yearbook 2020Document11 pagesDebt Market Yearbook 2020JayNo ratings yet

- Indian Monetary Policy Analysis (2010-2017)Document38 pagesIndian Monetary Policy Analysis (2010-2017)Parang Mehta95% (21)

- Impact of Credit Policy On The Indian Capital Markets: PortfoliotalkDocument5 pagesImpact of Credit Policy On The Indian Capital Markets: PortfoliotalkWELLS_BETSNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Marketing ManagementDocument28 pagesMarketing Managementaditya kothekarNo ratings yet

- Regulatory policy and monetary measures to tackle recessionDocument29 pagesRegulatory policy and monetary measures to tackle recessionaditya kothekarNo ratings yet

- Name of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Human Resource ManagementDocument24 pagesName of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Human Resource Managementaditya kothekarNo ratings yet

- Name of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Corporate Social ResponsibilityDocument26 pagesName of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Corporate Social Responsibilityaditya kothekarNo ratings yet

- Chapter - 1Document8 pagesChapter - 1aditya kothekarNo ratings yet

- Project Report HandbookDocument17 pagesProject Report Handbookaditya kothekarNo ratings yet

- Marketing ManagementDocument28 pagesMarketing Managementaditya kothekarNo ratings yet

- EM (Entrepreneurship Management)Document29 pagesEM (Entrepreneurship Management)aditya kothekarNo ratings yet

- Regulatory policy and monetary measures to tackle recessionDocument29 pagesRegulatory policy and monetary measures to tackle recessionaditya kothekarNo ratings yet

- Project Report HandbookDocument17 pagesProject Report Handbookaditya kothekarNo ratings yet

- Hall TicketDocument2 pagesHall Ticketaditya kothekarNo ratings yet

- Renault Duster review: capable SUV suits needs for mountain roadsDocument44 pagesRenault Duster review: capable SUV suits needs for mountain roadsaditya kothekarNo ratings yet

- Name of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Corporate Social ResponsibilityDocument26 pagesName of The College: Armiet Roll No: Armiet/mms 19/gt48 NAME OF THE STUDENT: Tejaswini Gajendra Gurav ACADEMIC YEAR: 2019-2020 SUBJECT: Corporate Social Responsibilityaditya kothekarNo ratings yet

- MARKETING MANAGEMENT, 15qDocument19 pagesMARKETING MANAGEMENT, 15qaditya kothekarNo ratings yet

- Reposition Its BrandDocument2 pagesReposition Its Brandaditya kothekarNo ratings yet

- Johnson & JohnsonDocument2 pagesJohnson & JohnsonRiddhi ShahNo ratings yet

- Organizational Environmental TheoryDocument14 pagesOrganizational Environmental Theoryaditya kothekarNo ratings yet

- ICICI BankDocument2 pagesICICI Bankaditya kothekarNo ratings yet

- TraceDocument3 pagesTraceaditya kothekarNo ratings yet

- Sem 2 Improvement TTDocument1 pageSem 2 Improvement TTaditya kothekarNo ratings yet

- Report of CSRDocument3 pagesReport of CSRRiddhi ShahNo ratings yet

- Nike Case StudyDocument5 pagesNike Case Studyaditya kothekarNo ratings yet

- Diffrance Between Oral & Written CommunicationDocument3 pagesDiffrance Between Oral & Written Communicationaditya kothekarNo ratings yet

- History of The CompanyDocument3 pagesHistory of The Companyaditya kothekarNo ratings yet

- Presentation1 150221070554 Conversion Gate01Document75 pagesPresentation1 150221070554 Conversion Gate01yellymarlianapatuNo ratings yet

- Nationalism in India - PadhleNotes PDFDocument10 pagesNationalism in India - PadhleNotes PDFTejpal SinghNo ratings yet

- Tackling Addiction: From Belfast To Lisbon: An In-Depth InsightDocument32 pagesTackling Addiction: From Belfast To Lisbon: An In-Depth InsightSonia EstevesNo ratings yet

- Qustion Bank LAB.docxDocument3 pagesQustion Bank LAB.docxshubhampoddar11.11No ratings yet

- Fiitjee All India Test Series: Concept Recapitulation Test - Iv JEE (Advanced) - 2019Document13 pagesFiitjee All India Test Series: Concept Recapitulation Test - Iv JEE (Advanced) - 2019Raj KumarNo ratings yet

- 1988 Ojhri Camp Disaster in PakistanDocument3 pages1988 Ojhri Camp Disaster in PakistanranasohailiqbalNo ratings yet

- DEED OF SALE OF MOTOR VEHICLE - TemplateDocument1 pageDEED OF SALE OF MOTOR VEHICLE - TemplateLiz BorromeoNo ratings yet

- Manantan v. CADocument1 pageManantan v. CARywNo ratings yet

- 07 Part of Speech ActivitiesDocument6 pages07 Part of Speech ActivitiesLorraine UnigoNo ratings yet

- 1 Aka 57Document4 pages1 Aka 57Richard FadhilahNo ratings yet

- Alf 2Document9 pagesAlf 2NamitaNo ratings yet

- Admin Case DigestDocument8 pagesAdmin Case DigestlenvfNo ratings yet

- ENSC1001 Unit Outline 2014Document12 pagesENSC1001 Unit Outline 2014TheColonel999No ratings yet

- SIOP Lesson PlanDocument6 pagesSIOP Lesson PlanSmithRichardL1988100% (3)

- Proposal On The Goals For ChangeDocument5 pagesProposal On The Goals For ChangeMelody MhedzyNo ratings yet

- Carte Tehnica Panou Solar Cu Celule Monocristaline SunPower 345 WDocument4 pagesCarte Tehnica Panou Solar Cu Celule Monocristaline SunPower 345 WphatdoggNo ratings yet

- English Language Communication Skills Lab Manual: Name Roll No. Branch SectionDocument39 pagesEnglish Language Communication Skills Lab Manual: Name Roll No. Branch SectionSurendrakumar ThotaNo ratings yet

- Đề Thi và Đáp ÁnDocument19 pagesĐề Thi và Đáp ÁnTruong Quoc TaiNo ratings yet

- People V Pugay DigestDocument2 pagesPeople V Pugay DigestSecret SecretNo ratings yet

- Math 7-4th QuarterDocument3 pagesMath 7-4th QuarterMarie Saren100% (2)

- US vs. HernandezDocument7 pagesUS vs. HernandezJnhNo ratings yet

- Macroeconomics 1st Edition Ebook or PaperbackDocument1 pageMacroeconomics 1st Edition Ebook or PaperbackSurya DarmaNo ratings yet

- Patient Medication ProfileDocument4 pagesPatient Medication ProfileLaura HernandezNo ratings yet

- Mounting Accessories 2017V03 - EN PDFDocument33 pagesMounting Accessories 2017V03 - EN PDFegalNo ratings yet

- Derrida Large DeviationsDocument13 pagesDerrida Large Deviationsanurag sahayNo ratings yet

- 2608 Mathematics Paper With Solution MorningDocument9 pages2608 Mathematics Paper With Solution MorningTheManASHNo ratings yet

- Csir Ugc Net - Life Sciences - Free Sample TheoryDocument12 pagesCsir Ugc Net - Life Sciences - Free Sample TheorySyamala Natarajan100% (1)

- Indosat AR10 ENGDocument564 pagesIndosat AR10 ENGHerry Abu DanishNo ratings yet